The payment industry has a habit of moving slowly before taking a sudden leap, and we are currently in the middle of one. For years, managing transactions felt like directing traffic with a blindfold. Merchants relied on rigid rules to push transactions from point A to point B. If a transaction failed, it was simply added to a pile of lost revenue. That approach is now a liability. The sheer complexity of global commerce has fundamentally broken the old models of payment optimization. Issuers are deploying highly aggressive fraud algorithms, while cross-border latency remains completely unpredictable. Solving payment failures now requires more than just fallback routing. It demands a system that can think, adapt, and predict in milliseconds.

Beyond the If-Then Trap

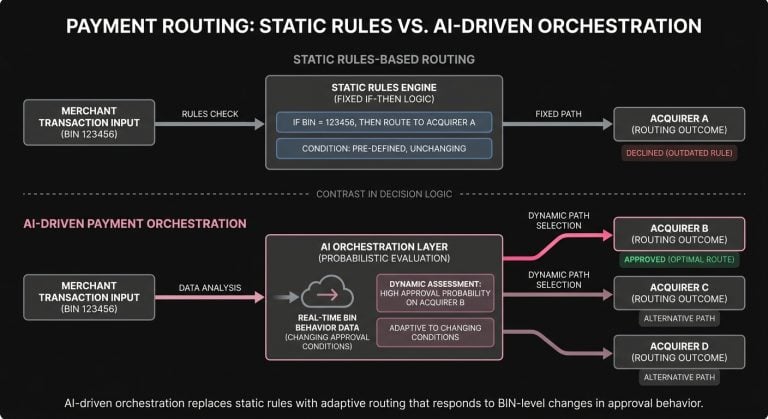

For the better part of the last decade, payment orchestration was governed by static rules engines. Payment operations teams would sit down and map out sprawling decision trees based on whatever data they could get their hands on. It usually looked something like this: if the transaction is from the UK and the card is a Visa, route it to Acquirer X. If that acquirer goes down, route it to Acquirer Y.

This logic made perfect sense at the time, providing a baseline of control and a safety net for major outages. However, the limitations of static routing are now painfully obvious. Static rules are binary. They lack context, miss subtle shifts in network behavior, and cannot adapt to the unique risk appetites of thousands of different issuing banks.

When you rely on static rules, you are essentially making guesses based on historical averages, but the payment ecosystem does not operate on averages. An acquiring bank might have exceptional approval rates for a specific BIN range at 10:00 AM, but subtly throttle those same bins at 2:00 PM because an internal risk threshold was reached. A static rule engine will blindly keep sending volume into the teeth of that throttling, resulting in a cascade of declined transactions.

Artificial intelligence fundamentally changes this architecture. Instead of routing a transaction based on a predetermined path, AI orchestration treats every single payment as a unique event with its own probability matrix. Before the transaction ever leaves the merchant’s environment, machine learning models analyze dozens of micro-signals. These include device telemetry, transaction velocity, time of day, network tokenization status, and historical issuer behavior to determine the optimal path for that exact moment.

The Reality of Payment Authorization

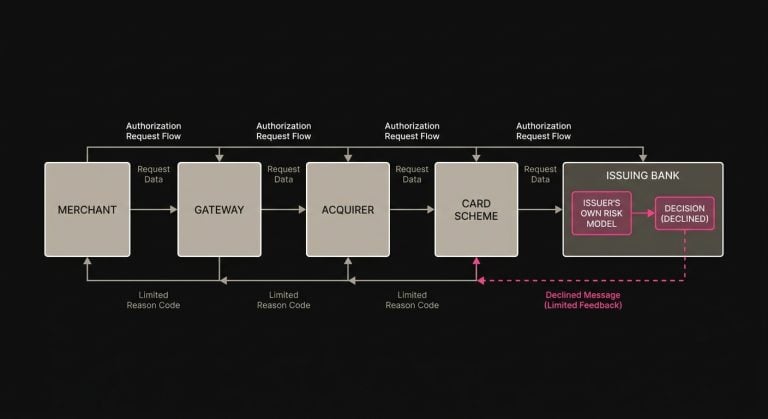

To appreciate why algorithmic orchestration is becoming the standard, you have to look closely at what actually happens during payment authorization. It is a minor miracle that a transaction ever gets approved in the first place, considering that within the span of a few hundred milliseconds, a payload of sensitive data must traverse the merchant, the gateway, the acquirer, the card scheme, and finally land at the issuing bank.

At the end of this journey sits the issuer’s own risk model. This model acts as the ultimate, entirely opaque gatekeeper. Issuers do not publish their risk parameters or broadcast their downtime. They simply ingest the authorization request and return a response.

When a declined message makes its way back down the chain, it rarely comes with a helpful explanation. Instead, you are often left staring at a vague two-digit code that offers zero actionable insight. The entire dynamic is asymmetrical because the issuer holds all the cards, leaving the merchant to guess what went wrong.

AI levels this playing field by aggregating and analyzing massive volumes of behavioral data across the entire payment processing flow. An AI-driven orchestration layer does not just look at a single merchant’s transactions, as it also evaluates network-wide patterns. If an issuer suddenly starts soft declining transactions from a specific acquirer, the AI detects the anomaly in real time. It can then instantly divert subsequent transactions through an alternative acquiring route that has a higher probability of success with that specific issuer, entirely bypassing the bottleneck.

Making Sense of the Nonsense: The Issuer Response

If you spend enough time looking at transaction logs, you will quickly develop a mild disdain for legacy decline codes. The most notorious of these is Do Not Honor, which is the payment equivalent of it’s not you, it’s me. It provides absolutely no technical context. The code simply means the issuer refused the transaction and will not explain why.

In the past, a Do Not Honor code was effectively a dead end. Merchants would either accept the loss or blindly hit the retry button, hoping the issuer would miraculously change its mind a few seconds later.

We now understand that an issuer response is highly contextual. A transaction declined under Code 05 could mean the user triggered a velocity filter, or the purchase looked slightly out of character for the cardholder’s typical spending habits. Alternatively, it could just mean the issuer’s risk model was experiencing a momentary blip.

AI models strip away the ambiguity of these generic codes by looking at the surrounding metadata. By analyzing the time of day, the specific BIN, the transaction amount, and the routing path, machine learning algorithms can infer the likely cause of the decline with a high degree of accuracy.

For example, if a model observes a spike in Code 05 declines for high-ticket transactions originating from a specific region, but low-ticket transactions on the same BIN are passing through smoothly, the AI can deduce that a localized risk filter has been triggered. Armed with this insight, the orchestration layer can dynamically adjust the presentation of the transaction. This might involve prompting the user for an additional layer of authentication like 3D Secure, which shifts the liability and often forces the issuer to approve the charge.

The Art and Science of the Retry

Understanding why a transaction failed is only half the battle, while the other half is figuring out what to do about it. The concept of retrying payments is not new, but the methodology has undergone a massive transformation.

Brute-force retrying is the practice of repeatedly submitting a failed transaction in rapid succession, and it is deeply frowned upon by the card networks. It looks exactly like a BIN attack. Issuers will actively penalize merchants who engage in this behavior by permanently blacklisting their transactions, making it a highly destructive way to manage checkout issues.

This brings us to the necessity of the intelligent retry. An intelligent retry requires patience, timing, and a deep understanding of network dynamics. Rather than immediately hammering the gateway, an AI model will hold the declined transaction and calculate the precise moment when a subsequent attempt is most likely to succeed.

Platforms like SmartRetry step into the fold to address this challenge. Instead of indiscriminately hitting the network, this technology focuses on intelligent retries by analyzing temporal data, issuer patterns, and specific decline logic. The approach recovers revenue and improves transaction approval rates without triggering risk flags, turning a previously blunt-force operation into a highly surgical one.

The variables involved in a successful retry are staggering. Sometimes, the most effective strategy is to wait 24 hours to clear a daily velocity limit, while other times, the solution is to switch the acquiring channel entirely. In certain cases, simply stripping out non-essential data fields from the authorization payload can reduce the perceived risk score on the issuer’s side. The AI orchestrator evaluates all of these permutations in the background, executing the retry only when the probability of success reaches a predefined threshold.

Solving the Recurring Revenue Puzzle

Nowhere is the impact of intelligent orchestration more evident than in the subscription economy. When dealing with one-off e-commerce purchases, the user is actively engaged in the checkout flow. If a card is declined, they can simply pull out a different card or switch to an alternative payment method like Apple Pay or a buy now, pay later service.

Subscription payment issues are an entirely different animal. These transactions happen asynchronously, usually in the middle of the night, without the cardholder present. If a recurring billing attempt fails, you cannot rely on the user to fix it in real time.

Historically, subscription businesses managed this through rudimentary dunning campaigns. A card would decline, and the system would automatically send an email to the customer while retrying the card on days three, five, and seven. This created a generic schedule applied indiscriminately to the entire customer base.

The problem with this approach is that it completely ignores the reality of consumer finance. People do not get paid on days three, five, and seven of a failed billing cycle. Instead, they receive their paychecks on the first and fifteenth of the month, or every other Friday. They might have insufficient funds for a few days before their account is replenished.

AI orchestration attacks involuntary churn by treating every single subscriber as an individual financial entity. By analyzing the historical clearing patterns of specific BIN ranges, the AI can predict when a cardholder is most likely to have available funds. If a subscription renewal fails due to insufficient funds on a Tuesday, the model might hold the retry until Friday morning at 8:00 AM, aligning perfectly with standard payroll deposits.

This level of predictive timing drastically reduces the need to retry failed payments excessively. It preserves the relationship with the customer by minimizing the number of aggressive dunning emails they receive, and it significantly extends the lifetime value of the subscriber base by catching revenue before it slips into hard churn.

The Trade-offs of Algorithmic Routing

Of course, no system is perfect, and any professional discussing AI in payments must acknowledge the operational realities and trade-offs. Transitioning from a static rules engine to a dynamic, machine-learning-driven orchestrator introduces a new set of complexities.

The first major consideration is latency. Payment processing is a game of milliseconds, meaning every time you introduce a new layer of decision-making into the transaction flow, you consume a portion of your latency budget. If an AI model takes 300 milliseconds to calculate the optimal routing path, and the transaction subsequently takes another 800 milliseconds to traverse the network, you are creeping dangerously close to the point where the consumer might abandon the checkout, or the gateway might time out. High-performance orchestration engines mitigate this by pre-computing routing tables based on predictive models, but latency remains a critical metric that must be actively monitored.

The second trade-off is the loss of absolute determinism. With a static rules engine, you always know exactly why a transaction went to Acquirer A instead of Acquirer B. If something goes wrong, you can look at the code and pinpoint the exact line of logic that caused the issue.

Machine learning models, by their very nature, introduce an element of opacity on the merchant side. These models route transactions based on complex, multi-dimensional probabilistic scoring. If you ask the system why it suddenly diverted 10% of your European traffic through a secondary gateway, the answer might be buried in a subtle correlation between a specific device fingerprint and an emerging issuer timeout pattern. This requires payment operations teams to shift their mindset. You are no longer managing the exact path of the transaction, but rather the parameters and the desired outcomes of the model.

Finally, there is the cost of false declines. When an AI model is aggressively tuned to reduce payment declines and maximize approval rates, it may occasionally route a genuinely fraudulent transaction through a highly permissive channel, resulting in a chargeback. Balancing the risk of chargebacks against the reward of higher authorization rates requires continuous tuning. Orchestration is no longer a set-and-forget proposition. The models drift over time as consumer behavior changes and issuers update their systems, necessitating ongoing oversight from experienced payment professionals.

Network Tokens and the Data Advantage

One of the quietest but most impactful ways AI is reshaping orchestration is through the management of network tokens. Over the last few years, the major card schemes have heavily incentivized the use of network tokens over raw primary account numbers, or PANs. Network tokens offer enhanced security, and crucially, they are often favored by issuer risk models, frequently resulting in a natural bump to the transaction approval rate.

However, the tokenization landscape is incredibly fragmented because not all issuers handle network tokens equally. Some legacy banking systems still process raw PANs more reliably than tokens. Furthermore, tokens can fall out of sync if a cardholder receives a new physical card. This updates their PAN, while the token provisioned to the merchant remains tethered to the old data, leading to inevitable checkout issues.

Intelligent orchestration layers solve this fragmentation dynamically. When a transaction is initiated, the AI evaluates the historical performance of network tokens versus raw PANs for that specific issuer and BIN range. If the model knows that a particular regional bank struggles with tokenized payloads, it can seamlessly swap the token out and transmit the raw encrypted PAN instead, optimizing the payload for exactly what the receiving bank wants to see.

This dynamic payload manipulation extends beyond just tokenization. Different acquirers and issuers have different formatting preferences for fields like billing addresses, device data, and 3D Secure indicators. An advanced orchestration engine acts as a real-time translator, reshaping the data payload on the fly to match the idiosyncratic requirements of the destination endpoint. It is the digital equivalent of speaking the local dialect, and it is a massive driver of incremental approval lift.

Stepping into the New Standard

The overarching theme in payments today is clear: the era of passive processing is over. For a long time, merchants viewed the payment stack as a utility. It was seen as a necessary cost center where success was defined simply by keeping the lights on and the gateway connected.

That perspective has completely shifted because margins in e-commerce and digital services are tighter than ever, and customer acquisition costs continue to climb. In this environment, you cannot afford to leave money on the table simply because a rigid routing rule failed, or an issuer returned a generic decline code that nobody bothered to investigate.

The integration of artificial intelligence into payment orchestration has elevated the discipline from a purely operational function to a strategic revenue driver. By embracing probabilistic routing, deep data analysis, and highly targeted recovery strategies, organizations are reclaiming control over their transaction flows so they are no longer at the mercy of opaque issuer risk models or single points of failure within the acquiring network.

Navigating this new ecosystem requires technical sophistication and a willingness to abandon outdated assumptions about how money moves. But for the teams that get it right, the reward is substantial. By transforming the checkout from a static gateway into an intelligent, learning system, businesses can turn payment friction into a competitive advantage, securing the revenue they have earned and delivering the seamless experience their customers expect.