How to Avoid Payment Declines at the 2026 FIFA World Cup

The 2026 FIFA World Cup is set to break records as it spans three massive countries. Millions of fans will cross borders, moving billions of dollars through digital channels in just a few weeks. Behind the roar of the crowds and the surge in spending, merchants are preparing for an unprecedented wave of checkout issues. When a fan travels from London to Monterrey or Tokyo to Toronto, their spending patterns change overnight. Issuers notice these shifts immediately, and suddenly, a perfectly valid purchase results in a transaction declined message. Understanding why these payment declines happen and how to navigate the complex web of cross-border payment declines is what separates prepared merchants from those leaving significant revenue on the table.

The Cross-Border Stress Test of the Decade

Hosting a global tournament across the United States, Canada, and Mexico creates a unique architectural challenge for payment systems. While the region is economically integrated, its banking infrastructure remains distinctly local. For merchants selling tickets, merchandise, travel packages, and hospitality experiences, this tri-national setup introduces significant complexity.

During typical operating periods, merchants rely on predictable baseline data. They know what a normal Tuesday looks like, so their risk engines are tuned to flag anomalies. The World Cup, however, is a massive, month-long anomaly where an influx of foreign cards interacts with domestic payment gateways at extraordinary volumes.

Consider a merchant in Miami processing a high-value VIP hospitality package for a customer using a card issued by a regional bank in Germany. The merchant sees a highly desirable sale, but the German issuer’s legacy risk system sees a compromised card being drained halfway across the world. If the merchant’s system simply routes this transaction blindly without optimizing the data payload, the chances of encountering payment issues skyrocket. Managing this requires a shift from passive processing to active orchestration.

Why Issuers Panic When Fans Travel

To understand how to avoid a card declined scenario, it helps to view the transaction through the eyes of the issuing bank. Issuers are ultimately responsible for the funds, making loss prevention their primary mandate. Their authorization systems rely heavily on historical spending patterns, geographical consistency, and velocity checks.

When an international tournament kicks off, those historical patterns are essentially thrown out the window. A fan might buy a plane ticket, book a hotel in a new country, and immediately begin purchasing local transit passes, stadium food, and expensive merchandise. Spending velocity increases rapidly while the geographical location shifts abruptly.

Many modern issuers have adapted to these behaviors using machine learning models that correlate travel purchases with subsequent foreign spending. However, a significant portion of global cards are still governed by older, more rigid rules engines. When these systems see an uncharacteristic spike in cross-border volume, their default defensive posture is to decline the transaction. Banks prefer the risk of annoying a customer over absorbing a fraudulent charge.

The Anatomy of an Out-of-Pattern Authorization

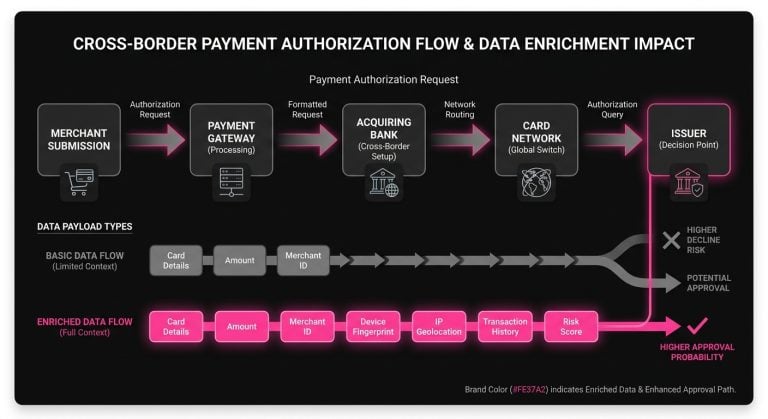

When a customer hits the checkout button, the payment authorization request embarks on a complex journey. It travels from the merchant to the payment gateway, through the acquiring bank, across the card network, and finally reaches the issuer. This entire processing flow happens in mere milliseconds.

During this brief window, the issuer evaluates dozens of data points. They look at the Merchant Category Code, transaction amount, currency, and the specific card’s history. They also check for security indicators like the Card Verification Value or Address Verification Service.

If a merchant submits a bare-bones authorization request for a cross-border transaction, they are starving the issuer of the context needed to approve it. Conversely, merchants who enrich the authorization payload with enhanced data give the issuer a much stronger foundation for trust. This extra data can include device fingerprinting, matching shipping and billing addresses, or 3D Secure authentication. Building this trust is the core mechanism for reducing payment declines during high-volatility events.

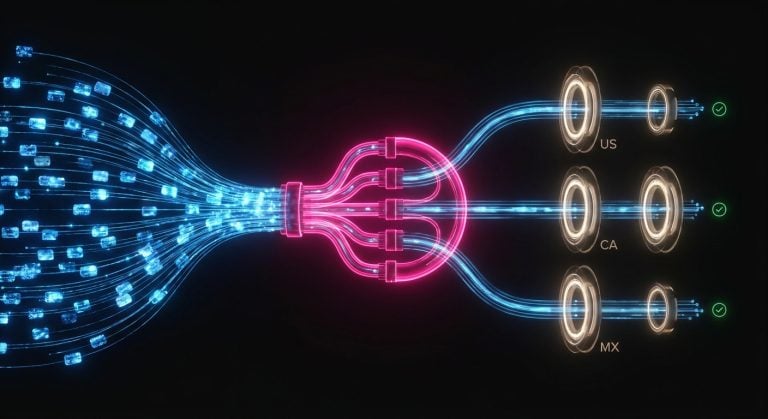

Local Acquiring vs. Cross-Border Routing

One of the most effective strategies to improve transaction approval rates is routing payments through a local acquirer. Issuers generally trust domestic transactions far more than cross-border ones.

If a merchant is selling team jerseys out of a fulfillment center in Mexico but their primary acquiring relationship is with a bank in New York, every local purchase made by a Mexican fan with a Mexican card is treated as a cross-border transaction. This significantly increases the likelihood of friction.

To optimize this flow, enterprise merchants often establish multiple acquiring relationships across different regions. By utilizing intelligent routing logic, they can direct a transaction from a Canadian cardholder to a Canadian acquirer, and a US cardholder to a US acquirer. This domestication of volume dramatically reduces the transaction’s risk profile in the eyes of the issuer.

Establishing local business entities and managing multiple acquirers naturally introduces operational and regulatory overhead. Merchants must weigh the cost of this setup against the projected uplift in revenue. For an event the size of the 2026 World Cup, the math often heavily favors multi-acquirer routing, provided the merchant has the orchestration capabilities to route transactions dynamically based on the card’s Bank Identification Number.

Decoding the Language of Denials

Even with pristine routing and rich data payloads, declines remain an unavoidable reality of digital commerce. The key to mitigating their impact lies in understanding the nuanced language of payment decline codes. When an issuer rejects a transaction, they send back a code explaining why, but unfortunately, these responses are frequently vague.

Declines generally fall into two categories: hard declines, soft declines. A hard decline indicates a permanent issue like a stolen card, a closed account, or an invalid primary account number. Attempting to process these transactions again is not only futile but can also lead to network penalties and damage the merchant’s reputation with the issuer.

Soft declines are temporary in nature. They occur for reasons like insufficient funds, temporary holds, or suspected fraud due to unusual spending patterns. A soft decline does not mean the customer is fraudulent or lacks the ability to pay. It simply means the transaction cannot be approved under the current conditions at this exact moment.

When a “Do Not Honor” Actually Means “Try Again Differently”

The most notoriously frustrating issuer response is the Do Not Honor decline. It acts as a generalized catch-all that issuers use when they want to decline a transaction but prefer not to specify the exact rule that was triggered. Often, an 05 decline is simply a soft decline masquerading as a hard one.

This is where true payment optimization begins. Savvy merchants know that a Do Not Honor response from a specific European issuer might actually indicate a formatting error in the billing address field, while the same response from a North American issuer could mean a velocity limit has been hit.

Instead of immediately surfacing a payment declined message to an eager fan trying to secure a last-minute match ticket, the merchant’s system can evaluate the response contextually. If the decline appears to be a soft, risk-based denial, there are often pathways to salvage the sale. This might involve prompting the user to authenticate the transaction via a challenge flow or making slight, compliant adjustments to the authorization data before initiating a secondary attempt.

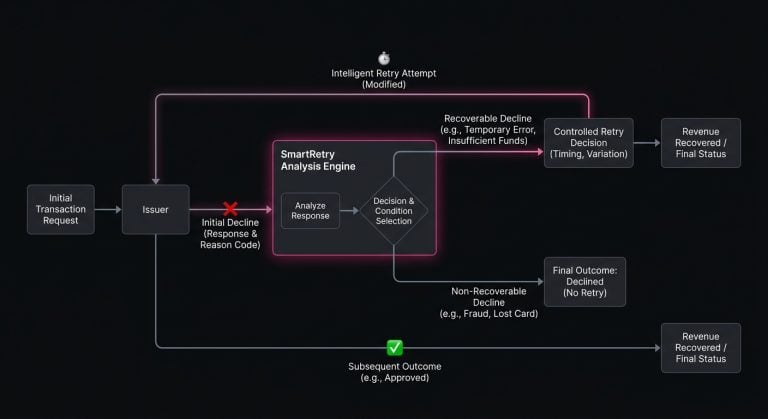

The Geometry of Intelligent Retries

Handling soft declines effectively requires a delicate balance. If a merchant’s system simply hammers the gateway with rapid, identical retry attempts, the issuer will likely flag the activity as an aggressive bot or a brute-force fraud attack. This can lead to the merchant’s entirely legitimate volume being temporarily blacklisted. Meaningful payment recovery relies on nuance, timing, and strategic variation.

Dedicated retry logic address this exact problem. Platforms like SmartRetry focus specifically on this layer of payment optimization by analyzing the initial issuer response to determine the exact conditions under which a transaction might succeed on a subsequent attempt. By deploying retry logic of declined payment transactions, these systems help merchants safely recover revenue and improve overall transaction approval rates without tripping risk thresholds or incurring unnecessary processing penalties.

The geometry of a successful retry strategy involves mapping the decline code, the issuer’s historical behavioral profile, the time of day, and the transaction value. It is a highly probabilistic exercise where you are essentially asking the system to predict whether a subsequent attempt will be viewed more favorably by a risk engine operating inside a black box.

Timing the Second Attempt

The timing of a retry is arguably the most critical variable. If a transaction is declined due to a suspected fraud trigger, retrying the exact same payload three milliseconds later is almost guaranteed to fail because the issuer’s system hasn’t had time to register any changing conditions.

For high-urgency purchases like stadium food or digital transit passes, merchants might only have a window of a few seconds to retry failed payments before the customer abandons the cart. In these scenarios, the retry logic can instantly attempt to route the transaction through a secondary gateway or a different acquiring path.

For less urgent purchases, such as pre-ordering commemorative merchandise, the optimal strategy might involve waiting several hours. This delay allows time for the cardholder to notice a fraud alert from their bank, acknowledge that the transaction is legitimate, and clear the block on their account. When the automated retry occurs later that afternoon, the pathway is clear. The transaction then succeeds seamlessly without any further effort from the customer.

Network Tokens and the Trust Factor

One of the most powerful tools available for preparing payment systems for the 2026 World Cup is network tokenization. Traditionally, merchants pass the raw 16-digit Primary Account Number through the payment flow. These numbers are static, vulnerable to theft, and frequently replaced when a card is lost or expires.

Network tokens issued directly by card networks like Visa and Mastercard replace the account number with a unique digital identifier tied specifically to a single merchant. Issuers inherently trust network tokens more than raw account data because the token is provisioned securely and includes dynamic cryptograms that validate each specific transaction.

Because of this elevated trust, transactions utilizing network tokens generally observe noticeably higher approval rates. Implementing network tokens is a highly effective way for merchants processing large volumes of cross-border traffic to bypass the rigid legacy fraud rules that often catch foreign travelers. Furthermore, when a fan inevitably loses their physical card amidst the chaos of a stadium crowd and receives a replacement from their bank, network tokens automatically update in the background to ensure uninterrupted service.

Navigating Alternative Payment Methods

While credit and debit cards remain dominant in North America, the World Cup brings a truly global audience with many fans preferring not to use traditional card networks at all. A comprehensive strategy for avoiding payment issues must account for these diverse international preferences.

European visitors might expect to see Open Banking options or regional favorites like iDEAL, while South American fans will almost certainly look for Pix, the instant payment system that has transformed digital commerce in Brazil. Meanwhile, Asian travelers frequently rely on digital wallets like Alipay or WeChat Pay.

Integrating these alternative payment methods does more than just cater to consumer preference. It structurally changes the risk profile of your checkout. Because these methods often require biometric authentication at the device level or redirect the user directly to their banking app, they inherently carry lower fraud risks and boast incredibly high approval rates. By shifting a portion of your international volume away from traditional card rails and onto localized payment methods, you naturally bypass complex cross-border authorization hurdles entirely.

Keeping the Streams Alive During Extra Time

Not all World Cup transactions occur at the stadium or the merchandise stand. For global broadcasters and streaming platforms, the tournament brings a massive influx of new subscribers as fans sign up for monthly passes or temporary streaming packages just to watch the games.

Managing these recurring billing models introduces a different set of challenges, particularly regarding subscription payment issues. A fan might successfully authenticate and pay for their first month while physically at home. However, if the recurring charge hits while they are traveling abroad or if their card expires during the tournament, the renewal can fail.

To maintain these streams, digital merchants must employ sophisticated lifecycle management tools. Account updater services that actively ping networks for fresh card details before the billing cycle hits are essential. Combining these tools with intelligent retry schedules tailored for subscription models ensures that a fan doesn’t lose access to the final match due to a preventable backend decline.

Winning the Conversion Game

Preparing for the massive transactional wave of the 2026 FIFA World Cup is not about finding a single silver bullet. Because the global payments ecosystem is far too fragmented for a one-size-fits-all solution, success requires a layered, highly orchestrated approach to authorization and recovery.

Merchants who view a decline as the end of the road will inevitably leave significant revenue behind. Conversely, those who treat declines as data points will build a far more resilient checkout experience. These data points act as signals that inform routing decisions, prompt authentication challenges, or trigger intelligent retry sequences.

By analyzing issuer behavior, localizing acquiring strategies, adopting network tokens, and gracefully managing inevitable soft declines, businesses can actively protect their revenue. This ensures the only friction fans experience is the tension on the pitch, not frustration at the checkout screen. The payment infrastructure built to handle the strain of this global event will capture immediate revenue while establishing a much higher baseline of operational maturity long after the final whistle blows.