The payments landscape is undergoing a fundamental shift. For years, deferred payment options were the darling of ecommerce checkouts, offering frictionless credit with minimal oversight. Merchants loved the immediate conversion bumps, while consumers embraced the ability to split payments across multiple months. But the era of unchecked installment lending has officially ended. As the industry digests the reality that Buy Now Pay Later is now a regulated product, a transition covered heavily by publications like motortrader.com, payment teams are re-evaluating their strategies. This shift changes the fundamental math on checkout optimization, approval rates, and decline management. Regulators are stepping in, and for the professionals managing payment processing flow, the days of treating installment plans as a simple conversion button are over.

Understanding BNPL Regulation Requirements

Bringing a previously unregulated financial product under the formal credit umbrella is a massive logistical undertaking. At its core, the new regulatory framework requires Buy Now, Pay Later (BNPL) providers to adhere to the same stringent rules that govern traditional credit cards and personal loans. For years, these services existed in a grey area, utilizing soft credit checks and relying on the technicality that short-term, interest-free credit didn’t require full regulatory authorization.

That loophole has now been firmly closed. Regulatory bodies have recognized that while the individual transaction amounts might be small, the aggregate debt accumulated by consumers is significant, with total BNPL balances outstanding in the United States estimated to have reached roughly $30 billion by the end of 2025 (Source). This shift isn’t happening in isolation but forms part of a broader push to modernize financial oversight. This is perfectly illustrated by recent legal briefings such as the UK to future-proof payment services: HMT consults on stablecoins, AI and Open Banking – Linklaters report. Governments are determined to pull all peripheral financial technologies into the supervisory fold, ensuring that consumer protections evolve at the same pace as payment innovation.

For BNPL providers, the regulations mandate comprehensive affordability assessments before extending credit. This means moving away from instant approvals based on superficial data and toward rigorous checks that evaluate a consumer’s actual ability to repay. Furthermore, consumers now gain robust statutory rights, including the ability to escalate complaints to financial ombudsmen and protection under consumer credit laws that hold lenders jointly liable for breaches of contract by merchants.

The Consumer Shift Driving the Rules

To understand the mechanics of these new rules, it is helpful to look at the consumer behavior that forced the regulators’ hands. The narrative surrounding deferred payments has matured rapidly. What began as a trendy way to buy sneakers has evolved into a tool used for everyday essentials, leading to a precarious stacking of invisible debt.

Recent behavioral data underscores a distinct shift in how the market views these products. Analysis such as The Pay Later Reset: Data Shows Young Consumers Retreat, Cards Hold Firm – PYMNTS.com reveals that as macroeconomic pressures mount, the initial enthusiasm for managing multiple installment loans has cooled. Consumers are realizing that managing five different split payments across various apps is far more complex than managing a single traditional credit card balance. Among BNPL users, 58 percent reported having used BNPL for five or more purchases (Source).

Simultaneously, the long-term financial consequences of these micro-loans have entered the mainstream consciousness. The ease of access masked the reality of the credit footprint. We have moved entirely past the honeymoon phase of frictionless credit, landing squarely in the reality captured by mainstream headlines like Is your buy now, pay later habit denting your mortgage chances? – Sky News. When retail spending habits begin interfering with major life milestones like securing a mortgage, regulatory intervention becomes inevitable. This heightened awareness means merchants must now handle BNPL not just as a marketing tool but as a sensitive financial touchpoint.

Merchant Compliance Checklist

While the heaviest regulatory burden falls on the BNPL providers themselves, merchants are far from exempt. If you offer installment payments at your checkout, your compliance responsibilities have expanded significantly. The integration is no longer just a simple API key and a visual widget. It requires a holistic review of how credit is presented to your customers.

The primary action items for merchants include overhauling marketing and checkout messaging. Regulatory bodies are cracking down on financial promotions. Merchants must ensure that BNPL is never presented as risk-free or guaranteed. The potential consequences of missed payments must be prominently displayed alongside the payment option. The days of minimizing the fine print are gone.

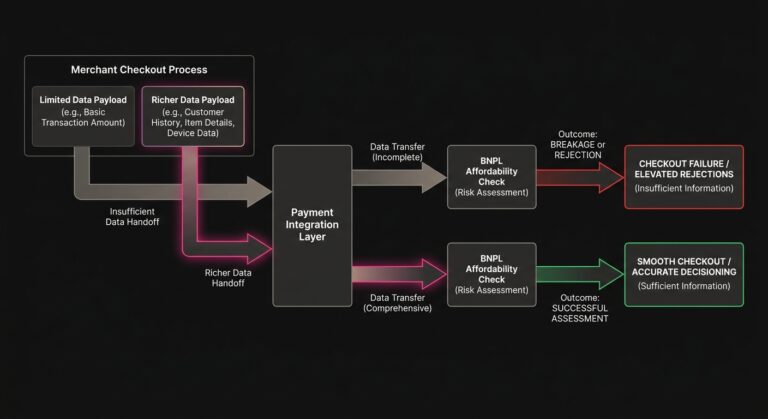

Technically, merchants must audit their payment integrations to support more complex data hand-offs. Because BNPL providers now must conduct thorough affordability checks, they require richer data payloads from the merchant during the checkout process. If your current integration only passes basic cart totals and an email address, you may face integration breakages or artificially high rejection rates.

Additionally, merchants must prepare for changes in the dispute resolution process. Because consumers now possess stronger statutory rights regarding these transactions, the refund and chargeback workflows will closely mirror those of traditional credit cards. Your payment operations team must ensure that your customer service protocols are aligned with the new regulatory obligations of the BNPL provider. This is particularly important regarding how quickly canceled orders or returned items are communicated back to the lender to halt upcoming consumer payments.

Impact on Payment Performance

For professionals focused on revenue optimization, the most pressing question is how these regulations will alter transaction approval rates. The answer requires a sober look at the mechanics of risk decisioning. Regulation inherently introduces friction, and in the world of payments, friction invariably leads to drop-off.

As BNPL providers implement mandatory, rigorous affordability checks, the immediate consequence will be a noticeable spike in buy now pay later declines. Previously, a provider might have accepted a borderline transaction to capture market share. Today, the regulatory risk of extending unaffordable credit outweighs the acquisition benefit. When an affordability check fails, the issuer response is immediate. The transaction is blocked.

This introduces a complex challenge for the payment processing flow. When a customer experiences a payment declined event at the very bottom of the checkout funnel, the psychological momentum of the purchase is broken. If they intended to spread a £300 purchase over three months and are suddenly denied, they face a stark choice. They must either abandon the cart or fund the entire amount immediately via a traditional card.

Because of this, merchants should anticipate a secondary ripple effect in the form of an increase in traditional checkout issues and card declined events. A customer rejected for an installment plan may attempt to use a debit card with insufficient funds or a credit card near its limit, leading to subsequent payment failures. Managing this specific type of soft decline requires a delicate orchestration of the checkout UI, offering graceful fallbacks that guide the consumer toward an alternative payment method without making them feel financially penalized.

To minimize revenue leakage, merchants need to closely monitor their authorization data. Segmenting declines by payment method helps identify exactly where the new regulatory friction is causing the most damage. Relying on aggregate approval metrics will mask the specific drop-offs occurring within the installment payment channels.

SmartRetry’s Compliance Features

When payment issues arise, whether from a stringent BNPL affordability rejection, a traditional network decline, or subscription payment issues, having a highly responsive infrastructure is the difference between a lost customer and a recovered sale. When a primary payment method fails, the immediate next steps dictate the final conversion rate. This is where an intelligent approach to retry failed payments becomes critical.

SmartRetry is designed precisely for these complex payment processing realities. As a platform focused on payment optimization and intelligent retries of declined payment transactions, it helps merchants recover revenue and improve transaction approval rates by analyzing the specific decline codes returned by the issuer. If a transaction is rejected due to a hard compliance block, blindly retrying it is useless and potentially damaging to your merchant standing. However, if the payment fails due to transient network issues, momentary insufficient funds on a fallback card, or asynchronous timeout errors during an extended credit check, SmartRetry applies optimized, data-driven retry logic to salvage the transaction. By intelligently routing transactions and dynamically adjusting to the nuances of different payment provider responses, merchants can reduce payment declines and maintain healthy revenue flows even as the regulatory environment tightens.

Navigating the Next Era of Checkout Optimization

The transition of Buy Now, Pay Later from a frictionless growth hack into a regulated financial product represents a maturation of the ecommerce ecosystem. While the immediate operational requirements and the potential for increased payment failures might seem daunting, this regulation ultimately creates a more sustainable and predictable payment environment.

The merchants who will thrive in this new landscape are those who stop viewing checkout as a static integration and start treating it as a dynamic, responsive system. Optimization is no longer just about offering the most payment methods. It is now about engineering the most resilient payment recovery flows. By understanding the specific triggers of modern transaction declines, respecting the new compliance boundaries, and implementing intelligent strategies to manage the inevitable friction, payment teams can protect their revenue and build deeper, more trustworthy relationships with their customers. The spotlight has certainly fallen on installment payments, but with the right operational discipline, it simply illuminates a path to more robust payment performance.