The honeymoon phase for frictionless credit at the checkout is officially over. For years, splitting a purchase into bite-sized, interest-free chunks was the ultimate conversion driver. Shoppers loved the immediate flexibility and ease of access, while merchants relied on the resulting inflated basket sizes. Payment operations teams simply integrated a checkout widget and watched their conversion metrics climb.

But as consumer adoption skyrocketed, the inevitable pivot toward traditional financial oversight arrived. Today, the spotlight is firmly on alternative credit mechanisms. Addressing checkout issues and navigating tighter payment authorization rules are now top priorities for revenue leaders as the ecosystem undergoes a fundamental shift.

The Macro Shift Driving the Regulation

Consumer behavior is shifting rapidly beneath the surface of the payments ecosystem. Before diving into the technical compliance checklists, it is critical to understand why the regulatory net is tightening right now. Inflationary pressures and economic headwinds have forced a broad re-evaluation of short-term debt, a trend reflected clearly across recent consumer data sets. For example, recent analysis, such as the insights detailed in The Pay Later Reset: Data Shows Young Consumers Retreat, Cards Hold Firm by PYMNTS.com, reveals that younger demographics are becoming much more cautious with delayed payment structures. They often revert to traditional credit rails when household budgets tighten.

Simultaneously, the broader financial implications of alternative credit have pierced mainstream consciousness. Consumers are beginning to realize that seemingly harmless, fragmented installments can have lasting impacts on their long-term financial profiles. When mainstream media outlets start running cautionary features titled Is your buy now, pay later habit denting your mortgage chances? by Sky News, it becomes glaringly obvious that the product has outgrown its regulatory sandbox. It is no longer just a slick software feature for eCommerce. It is a systemic financial product that directly impacts consumer livelihoods.

This realization has triggered an inevitable response from governing bodies. As observed in specialized industry coverage like Spotlight falls on Buy Now Pay Later as regulated product from today by motortrader.com, the narrative has aggressively shifted from growth-at-all-costs to long-term sustainability and consumer protection. A product that was once considered a minor retail add-on is now treated with the same severity as traditional lending.

Understanding BNPL Regulatory Requirements

This tightening of the reins does not happen in isolation. As highlighted in broader legal and financial briefings, such as UK to future-proof payment services: HMT consults on stablecoins, AI and Open Banking by Linklaters, authorities are actively modernizing their oversight to capture emerging technologies and alternative payment flows in one cohesive sweep. So, what exactly changes when a flexible checkout option officially becomes a fully regulated product?

At its core, the new regulatory framework mandates that short-term, interest-free credit adhere to the same foundational rules as traditional consumer credit. This requires rigorous affordability checks, with upcoming UK rules applying mandatory checks to purchases from £50 upward (Source). Providers can no longer rely purely on proprietary algorithms, localized soft data points, or a simple identity check to approve a transaction. They must now take definitive steps to ensure the consumer can genuinely afford the repayments without experiencing subsequent financial hardship.

Next, advertising and consumer messaging must become radically transparent. The terms free and no cost are heavily scrutinized and in many cases restricted. Merchants and credit providers must clearly outline the risks of missed payments upfront, including potential late fees and the harsh reality that unresolved debt may be reported to national credit reference agencies.

The regulation also grants consumers access to formal dispute resolution frameworks, such as a financial ombudsman service, alongside stronger purchase protections akin to traditional credit card safeguards. For the underlying payment processing flow, this means the regulatory burden is increasingly shared. While the primary credit provider bears the brunt of the legal liability, the merchant acting as the credit broker is also subject to strict compliance, operational oversight, and technical requirements. Enforcement is expected to be rigorous as authorities publicly look to make early examples of non-compliant, misleading checkout experiences.

Merchant Compliance Checklist

For merchants, the days of a passive, plug-and-play integration are permanently over. Operating in a regulated financial environment requires active, ongoing participation in the compliance lifecycle. Payment operations, product managers, and legal teams must collaborate to ensure the entire customer journey aligns with the new mandates.

Your immediate focus should be on the checkout interface itself. The messaging displayed right before a user clicks buy must be comprehensively audited. Are you clearly communicating that this payment method is a legally binding form of credit? All promotional banners, product page widgets, and checkout buttons must be updated to include mandatory risk warnings. If your user interface obscures the potential consequences of missed payments, you are likely operating out of compliance.

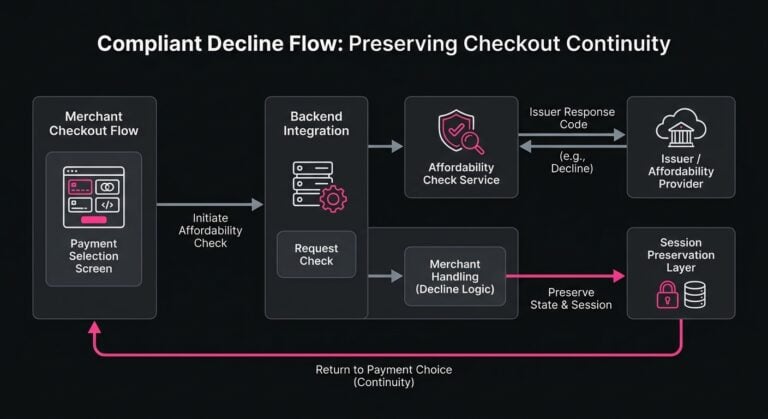

Next, examine your backend technical integrations. Strict affordability checks introduce latency and complexity into the checkout process, meaning merchants must ensure their APIs are equipped to handle new issuer response codes gracefully. When a provider declines a consumer based on an affordability check, your system must manage that specific declined scenario without breaking the session or locking the cart. The user should be routed seamlessly back to the payment selection screen to choose an alternative method, which minimizes unnecessary cart abandonment.

Documentation and data handling also require an immediate overhaul. Merchants will increasingly be required to store specific consumer consents and present comprehensive terms and conditions before the transaction authorization occurs. You will need a clear, unassailable audit trail demonstrating that the consumer was shown the required disclosures at the exact time of purchase. Regular compliance audits should be scheduled with your payment service providers to ensure both parties remain aligned on data sharing agreements, liability shifts, and mandatory reporting obligations.

Impact on Payment Performance

Any time you introduce friction into a checkout flow, you alter the fundamental conversion math. The transition to a regulated product inherently changes how payment teams forecast revenue, evaluate risk, and manage the overall transaction approval rate.

The most immediate and visible impact will be felt at the very top of the funnel. Mandatory affordability checks will inevitably lead to a noticeable increase in initial checkout rejections. Near term, merchants are expected to see BNPL approval rates drop by 10 to 20 percent (Source). While this might look like an alarming spike in payment failures on your daily operational dashboard, it is actually a legally necessary filtering mechanism. These buy now pay later declines are designed precisely to weed out high-risk transactions before they enter your ledger and become problematic debt.

However, the ripple effects extend far beyond the initial authorization. Alternative credit models rely heavily on the success of subsequent automated installment payments. Historically, these secondary captures have been vulnerable to high failure rates as consumer bank accounts fluctuate between paydays. If a consumer is approved under stricter affordability criteria upfront, logic suggests their ability to meet future obligations should actually improve. Consequently, you might paradoxically see a decrease in card declined events on the second, third, and fourth scheduled installments.

Yet macroeconomic realities dictate that subsequent installment failures will never drop to zero, as subscription payment issues and capture failures will persist. When an issuer response indicates insufficient funds for a scheduled capture, merchants and providers face a highly complex recovery challenge. Because the product is now heavily regulated, aggressive debt collection tactics, hidden fees, or rapid-fire automated retry attempts can easily cross the legal line into consumer harassment. Optimizing these secondary captures requires a highly sophisticated approach to payment recovery. You must balance the absolute need to reduce payment declines with strict adherence to consumer protection laws, ensuring any programmatic retry logic is intelligent, justified, and compliant.

SmartRetry’s Compliance Features

Navigating the recovery of missed installments in a highly regulated environment leaves zero room for brute-force tactical errors. When an automated payment fails, blindly hitting the payment gateway over and over is no longer just technically inefficient. It is a potential compliance violation that can draw regulatory scrutiny. This is exactly where modern, intelligent infrastructure becomes essential. For teams aiming to balance aggressive revenue recovery with strict regulatory adherence, leveraging specialized platforms like SmartRetry is the pragmatic move. SmartRetry focuses on payment optimization and intelligent retries of declined payment transactions. It helps merchants recover revenue and improve transaction approval rates without violating these strict compliance mandates. By utilizing machine learning to analyze the underlying issuer behavior, the platform determines the precise, optimal timing and conditions for a retry attempt.

Crucially, SmartRetry supports the sophisticated compliance features necessary for heavily regulated environments. It manages Strong Customer Authentication requirements gracefully, utilizing dynamic exemption routing where appropriate to minimize friction on subsequent captures. Every single retry attempt is logged with a comprehensive, immutable audit trail that provides full transparency into the automated recovery process. This ensures your operational efforts to retry failed payments never breach the legal thresholds of consumer harassment or run afoul of the new credit regulations. By seamlessly handling the complex nuances of issuer responses and adapting dynamically to specific decline codes, the platform improves the bottom line without exposing the merchant to unnecessary regulatory blowback.

Adapting to the Regulated Checkout Reality

Ultimately, the spotlight falling on alternative checkout financing is a sign of long-term industry maturation, not destruction. The transition from a frictionless, unregulated growth hack to a mature, regulated financial product forces the global payments industry to build more resilient, transparent, and sustainable systems.

Merchants who view these regulatory changes merely as an annoying compliance burden will likely struggle with increased payment issues, higher drop-off rates, and significant operational drag. Initial checkout conversion rates are also expected to decline by roughly 2-12 percent under the new BNPL friction. Conversely, those who treat this pivot as a strategic opportunity to refine and audit their payment processing flows will build stronger, more trusting relationships with their customer base. By integrating transparent messaging upfront, adapting to intelligent decline management, and legally optimizing how subsequent installments are recovered, businesses can maintain the checkout flexibility consumers still desire while vigorously protecting their own bottom lines. The rules of the game have fundamentally changed, but the core objective remains exactly the same. Merchants must deliver a seamless, reliable, and entirely compliant payment experience from the first click to the final, successful settlement.