The Blueprint for Frictionless Value: How Swift’s Blockchain Ledger is Rewiring Global Payments

Cross-border money movement has historically felt like navigating a maze blindfolded. You send a transaction into the ether and simply hope it emerges intact on the other side. Along the way, it bounces through a fragmented network of correspondent banks, where each stop introduces delays, unpredictable fees, and frustrating payment issues. But the foundational architecture of international finance is finally shifting. Swift’s blockchain-based strategy is helping to modernize the global payment processing flow. Rather than another speculative crypto experiment, this is a calculated infrastructure upgrade designed to eliminate the friction that has plagued interbank transfers for decades.

For businesses operating on a global scale, the mechanics of how money crosses borders are often abstracted away until something breaks. When a high-value transfer is delayed by days or an international checkout stalls unexpectedly, the root cause usually lies deep within legacy banking infrastructure. By moving toward a model built on shared digital ledgers, Swift is attempting to untangle this web, creating a more deterministic, transparent, and efficient system for moving value across the world.

The Correspondent Banking Conundrum

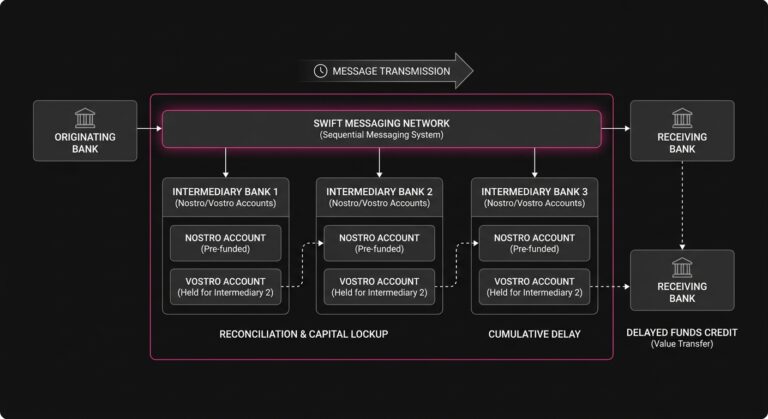

To understand why Swift’s blockchain initiatives matter, we first have to look at the plumbing we currently rely on. For half a century, international payments have operated primarily on a sequential messaging system. When a bank in London wants to send money to a bank in Singapore, it does not hand over digital cash in real-time. Instead, it sends a highly secure message instructing the receiving bank to credit an account. This reliance on messaging requires a chain of intermediary banks to settle the funds through pre-funded holding accounts, known as Nostro and Vostro accounts.

This system functions, but it is inherently fragile and highly capital-intensive, as every single hop in the correspondent banking chain requires independent reconciliation. If a single intermediary encounters a compliance flag, a mismatched AML data field, or even a regional banking holiday, the payment stalls. For the end user or merchant waiting on the funds, this often translates to opaque payment failures. Users are often left staring at a dashboard, wondering why a critical transfer is taking four days to clear or why it was rejected outright without a clear explanation.

The fundamental issue driving this friction is fragmented ledgers, with every participating bank maintaining its own isolated record of truth. Reconciling those separate ledgers across borders, time zones, and varying regulatory environments is a massive operational tax. The cost of trapping liquidity in intermediary accounts, combined with the manual effort required to investigate failed transfers, creates a baseline level of friction that affects every participant in the global economy. Even as the industry transitions to richer data standards like ISO 20022, the underlying architecture remains a messaging system rather than a unified state of truth.

Shifting from Messages to Shared States

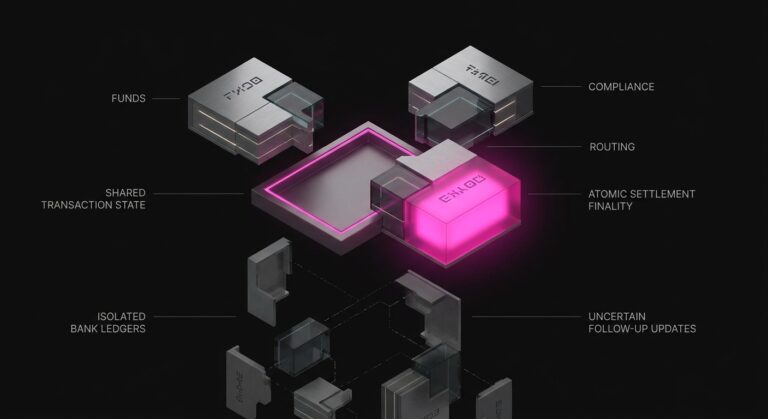

Swift’s exploration of blockchain networks, specifically through the concept of a unified ledger, fundamentally changes how interbank transactions operate. Instead of sending a message asking another bank to update its isolated ledger at some point in the future, institutions can interact with a shared, programmable environment in real-time.

It is similar to the difference between mailing a physical draft of a contract for edits versus collaborating simultaneously on a cloud-based document. A shared ledger provides a single, immutable source of truth that all authorized parties can view at the same time. When a transaction is initiated, the ledger can instantly verify that the sender has the available funds, that the receiver meets all compliance requirements, and that the routing paths are fully open.

This architectural shift opens the door to atomic settlement. In a distributed ledger environment, atomic settlement means the transfer of the asset and the final payment happen simultaneously. If one part of the transaction fails to meet the required conditions, the entire operation fails instantly before any money actually moves, leaving no ambiguous limbo state. Because the transaction is atomic, there is no scenario where funds leave one account but never arrive at the destination due to a downstream routing error. This deterministic outcome is a massive upgrade over the probabilistic nature of traditional cross-border routing.

Solving the Interoperability Puzzle

One of the biggest hurdles in modernizing global finance has not been a lack of new technology, but a glaring lack of interoperability. Over the last few years, central banks have actively developed Central Bank Digital Currencies, while commercial banks experiment with tokenized deposits and regulated fintechs build on public and private blockchains. Left unchecked, this rapid innovation creates digital silos that are just as fragmented as the legacy correspondent banking network they aim to replace.

Swift’s unique advantage is its deeply entrenched network effect. Connecting over 11,000 institutions across more than 200 countries, it already serves as the trusted connective tissue of global finance (Source). By acting as the central interoperability layer for these various blockchain networks, Swift can securely route tokenized assets across completely different protocols without requiring banks to overhaul their core systems.

Recent network experiments have demonstrated how this works in practice, showing how a tokenized deposit on an Ethereum-based private chain can be seamlessly exchanged for a digital asset on a Hyperledger network. The Swift infrastructure abstracts the underlying technical complexity, allowing financial institutions to transact across disparate blockchains using the same secure, standardized endpoints they already use today. Rather than rebuilding their entire tech stack, they simply tap into an upgraded, interoperable network.

The Downstream Impact on Transaction Lifecycles

While interbank settlement happens deep behind the scenes, its efficiency directly impacts the merchant and consumer experience. When macro-level infrastructure is slow, expensive, and opaque, the friction trickles down through the entire payment ecosystem, eventually reaching the checkout page.

Consider how payment authorization issues often manifest in everyday commerce. When a consumer attempts to pay for a digital service from a merchant located in another country, the complex routing required to authorize and settle that payment introduces significant latency. In the payments world, latency frequently leads to network timeouts that result in unexpected decline messages, leaving the consumer frustrated and the merchant with a lost sale.

By moving toward near-instant, blockchain-based settlement, the entire cross-border payments pipeline becomes substantially more resilient. Real-time verification of funds and immediate settlement reduce the window for fraud, eliminate currency fluctuation risks during transit, and lower the operational costs of cross-border commerce. When banks spend less time and money reconciling fragmented ledgers, those systemic efficiencies eventually translate to better acceptance rates and lower processing costs for merchants operating on a global scale.

Bridging Macro Infrastructure and Merchant Realities

Upgrading the interbank layer is a monumental step forward, but it does not solve every friction point in the payment lifecycle. Even if Swift achieves instantaneous, frictionless global settlement, merchants still have to navigate the highly unpredictable nature of issuer responses at the point of sale.

A unified ledger ensures that banks can talk to each other seamlessly, but it does not stop an issuing bank from rejecting a perfectly legitimate transaction due to aggressive risk models, velocity limits, or temporary system outages. When a vague decline response hits your system, having a fast settlement network operating in the background offers little comfort. Merchants still have to figure out how to salvage the revenue in the moment.

This is where localized, intelligent execution becomes critical. While Swift modernizes the macro routing of global finance, platforms like SmartRetry focus on the micro-level realities. They help merchants recover revenue through intelligent retries of declined transactions, reducing payment failures and optimizing the overall approval rate. By analyzing specific decline codes and understanding historical issuer behavior, merchants can dynamically route and retry failed payments at the optimal time. The underlying global pipes need to be fast and transparent, but local checkout logic must also be smart enough to handle the inevitable edge cases that occur between the merchant and the issuer.

Smarter Handling for Recurring Revenue Models

The intersection of faster global settlement and intelligent decline handling is particularly important for businesses relying on subscription models. Recurring billing requires a delicate, ongoing balance of timing, trust, and seamless backend execution.

When you process a recurring charge across borders, the variables multiply rapidly. An expired card, a temporary hold on the consumer’s account, or a regional compliance check at an issuing bank can easily disrupt the billing cycle. Unresolved subscription payment issues are notorious for causing involuntary churn, creating scenarios where the customer fully intended to maintain their service, but the payment ecosystem simply failed them.

As Swift’s blockchain initiatives streamline cross-border funds availability, issuing banks may eventually gain more accurate, real-time views of customer liquidity across different currencies. However, until the entire global ecosystem operates flawlessly across every endpoint, merchants must maintain sophisticated logic to bridge the gap. This means implementing payment optimization strategies that know exactly when a soft decline warrants a strategic retry two days later, versus a hard decline that requires immediate customer outreach. The goal is to minimize friction for the end user while maximizing captured revenue.

The Economics of Predictability

Ultimately, the integration of blockchain and shared ledgers into the Swift network is about replacing probability with predictability. For decades, global commerce has accepted a certain percentage of payment failures, extensive reconciliation delays, and trapped capital as the unavoidable cost of doing business internationally.

That mindset is rapidly becoming obsolete as the modern payment ecosystem shifts toward a state where outcomes are known instantly. Shared ledgers provide the transparency required to know exactly where funds are at any given millisecond, while smart contracts enable the automatic execution of payments only when predefined conditions are met. This drastically reduces counterparty risk and operational uncertainty.

For businesses moving money across borders, this predictability is a massive competitive advantage. It unlocks more accurate cash flow forecasting, frees up working capital previously held in pre-funded intermediary accounts, and reduces the substantial overhead associated with manual payment recovery, exception handling, and dispute resolution. By removing the guesswork from international settlement, businesses can allocate resources toward strategic growth rather than operational troubleshooting.

Preparing for the Next Era of Value Transfer

The transition from legacy messaging systems to interconnected, programmable blockchain ledgers will not happen overnight. Global financial infrastructure is massive, deeply entrenched, heavily regulated, and understandably risk-averse. Swift’s approach of running controlled interoperability trials, partnering with major global financial institutions, and gradually layering blockchain capabilities into its existing network is the most pragmatic and realistic path to widespread adoption. It is already working with over 30 financial institutions to build the blockchain-based ledger (Source), and 17 banks across 6 continents are preparing to pilot live transactions on the MVP (Source).

As these capabilities continue to come online, the baseline expectations for global payment performance will shift permanently. The days of waiting multiple business days for cross-border settlement, or accepting high international decline rates as a standard cost of doing business, are numbered. The foundational plumbing of the global economy is finally getting a necessary, structural overhaul.

For teams managing payments, product growth, and revenue operations, the mandate is clear. They must stay attuned to how macro-level infrastructure changes influence downstream authorization flows while building resilience and adaptability into checkout experiences. Combining the emerging efficiency of modern global networks with intelligent, data-driven retry logic at the merchant level is essential. By actively bridging the gap between how money moves internationally and how it is captured at the point of sale, businesses can build a payment stack that is highly resilient and primed for the future of global commerce.