The payment landscape is shifting under our feet. For years, deferred payment options operated in a comfortable regulatory gray area, offering seamless checkout experiences and minimal friction. Merchants loved the conversion boost while consumers loved the flexibility. But the era of frictionless, unregulated micro-credit is officially. The spotlight falls on Buy Now Pay Later as a regulated product from today, a pivot actively documented by motortrader.com and numerous other industry voices. As oversight tightens, payment operations teams face a new reality. The days of treating these methods as simple pass-through transactions are gone. Now, we must treat them like the credit products they actually are, complete with affordability checks, strict compliance mandates, and a real risk of increased payment failures.

This shift is not happening in a vacuum. Recent coverage exploring the Pay Later Reset highlights a distinct retreat among younger demographics, while traditional credit cards hold firm. Consumers are waking up to the reality of deferred debt, heavily influenced by mainstream warnings questioning whether a buy now, pay later habit is denting mortgage chances. As credit bureaus begin ingesting this data, missing a micro-payment suddenly carries macro consequences. This regulation is also part of a much larger governmental push. The UK’s effort to future-proof payment services, where HM Treasury consults on stablecoins, AI, and Open Banking, proves that regulatory bodies are modernizing their approach to the entire financial technology stack. Deferred payments are simply the first major domino to fall in this new era of digital finance oversight.

Understanding Buy Now Pay Later Requirements

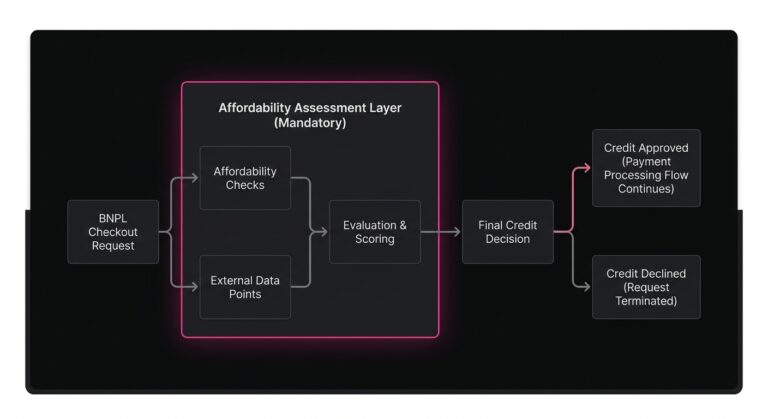

To adapt to this new environment, we first need to dissect what regulatory bodies are actually demanding. At its core, the regulation shifts Buy Now Pay Later (BNPL) from a purely technological checkout feature to a formally regulated consumer credit product. This means that providers and the merchants who offer these services must adhere to strict financial conduct rules that were previously reserved for traditional lenders and credit card issuers.

The primary requirement centers on affordability. Regulators are no longer satisfied with instantaneous, blind approvals. Providers must now conduct proportionate affordability checks before extending credit. This fundamental change forces a structural alteration in the payment processing flow. Instead of a simple risk and fraud assessment, the system must now evaluate a consumer’s financial health in real time, pulling in external data points to ensure the borrower can reasonably afford the repayment schedule.

Consumer protection rules are also being drastically strengthened, starting with mandatory, transparent disclosures at the point of checkout. Consumers must be explicitly warned about the consequences of missed payments, including potential damage to credit scores and the involvement of debt collection agencies. Regulatory frameworks now introduce stronger dispute resolution rights, allowing consumers to take grievances to financial ombudsmen. For payment teams, this means the technical infrastructure must support complex data routing, capture explicit consent, and maintain immutable audit trails of the terms presented to the user at the exact moment of purchase.

The Shift in Consumer Liability

A critical subtext of this regulation is the formalization of consumer liability. Under the old model, the financial consequences of a missed installment were often limited to late fees or suspension from a specific BNPL platform. Under the regulated model, a payment declined on a subsequent installment can trigger formal credit reporting. This high-stakes environment means merchants must be highly communicative and operationally flawless in how they present these payment methods, ensuring they do not accidentally mislead a consumer into a credit agreement they do not fully understand.

Merchant Compliance Checklist

While the heaviest compliance burden falls on the BNPL providers themselves, merchants are by no means exempt. If you are offering regulated deferred payments on your checkout page, you share the responsibility for consumer clarity and fair treatment. Adapting to this requires a systematic review of your checkout architecture and customer communication protocols.

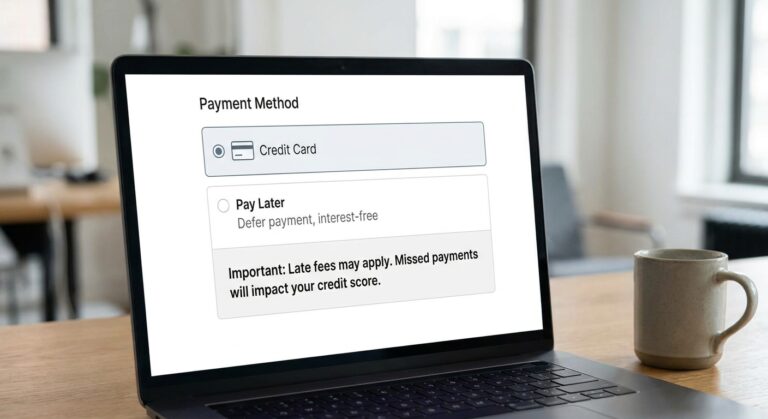

First, your checkout user interface requires an immediate audit. Regulators are cracking down on sludge design and dark patterns, meaning you cannot pre-select a deferred payment option as the default method. Consumers must actively opt in to financing. The marketing language surrounding these buttons must also be updated. Phrases such as interest-free need to be accompanied by clear warnings about late fees and credit impacts. These warnings must be presented prominently rather than buried in an external terms of service link.

Second, merchants must update their data sharing agreements and privacy policies. Because affordability checks require more robust consumer data, the information passed from the merchant to the payment provider via the API must be handled with strict adherence to data protection regulations. You must ensure you have the appropriate consent to transmit this data for the purpose of a credit assessment.

Third, customer service and dispute workflows must be entirely revamped. When a consumer experiences a transaction declined due to an affordability check, your frontline support team must know how to handle it. They cannot manually override the decision, nor should they encourage the user to manipulate their data to force an approval. Establishing clear, compliant playbooks for handling these specific checkout issues is essential to avoiding regulatory penalties and maintaining consumer trust.

Impact on Payment Performance

For professionals focused on revenue optimization, the most pressing question is how these regulations will impact the bottom line. The reality is that compliance introduces friction, and in the world of payments, friction is the historic enemy of conversion. By mandating affordability checks and stricter consumer warnings, regulators are intentionally designing a system where it is harder for consumers to take on debt.

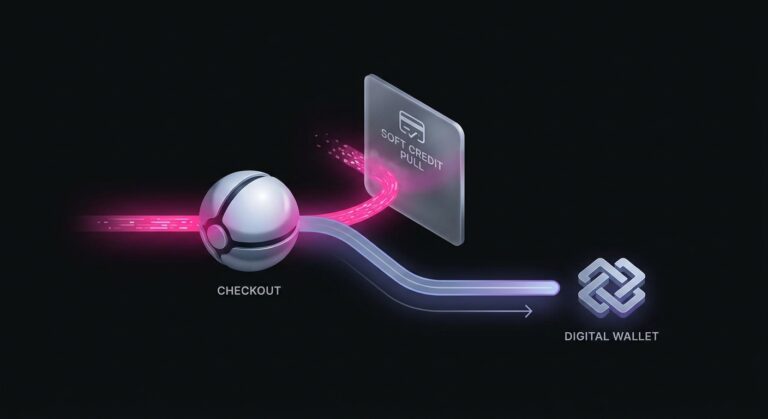

Consequently, we will see a significant rise in buy now pay later declines at the point of origin. When a user initiates a checkout, the payment authorization request is no longer just checking if the card is valid or if the transaction looks fraudulent. Instead, it waits for an issuer response based on a soft credit pull, and if the consumer fails that check, the transaction is rejected. From a merchant perspective, this creates a critical drop-off point. If your checkout UI does not gracefully handle that decline by immediately offering an alternative, lower-friction payment method, like a standard debit card or a digital wallet, you will lose the sale entirely. The overall approval rate for deferred payment methods will inevitably decrease as lending criteria tighten.

Managing the Lifecycle of Deferred Payments

The performance impact extends far beyond the initial checkout. Deferred payment models rely on scheduled, subsequent billing cycles. Whether the BNPL provider assumes the risk or the merchant operates a white-labeled installment plan, collecting the remaining balance is where operational nightmares begin.

When a consumer’s card on file fails during a subsequent installment, it mimics the exact mechanics of subscription payment issues. You are suddenly dealing with a card declined for non-sufficient funds, expired credentials, or network blocks. In the past, some systems might have aggressively retried these cards to force the payment through. Under the new regulatory scrutiny, aggressive and thoughtless retry logic can be classified as predatory debt collection. Excessive retries not only incur heavy network penalties but also place merchants and providers in the crosshairs of consumer protection agencies.

SmartRetry’s Compliance Features

This exact intersection of revenue recovery and strict compliance is where intelligent infrastructure becomes indispensable. When dealing with failed subsequent installments or recurring billing models, relying on blunt force to retry failed payments is both costly and risky. SmartRetry provides a sophisticated layer of payment optimization that aligns perfectly with strict regulatory requirements. Rather than blindly pinging the network, the platform analyzes specific decline codes and issuer behavior to determine the optimal timing for a retry.

Crucially for regulated environments, SmartRetry handles the complexities of Strong Customer Authentication exemptions and Merchant Initiated Transaction flagging with precision. When recovering a declined installment, the system ensures the transaction is coded correctly so it does not falsely trigger an authentication challenge that the consumer is not present to complete. By maintaining detailed, immutable audit trails of every retry attempt and strictly capping retry frequency to align with network rules and consumer protection guidelines, SmartRetry allows merchants to reduce payment declines and maximize payment recovery without crossing the line into aggressive collection tactics.

Adapting to the Maturing Payment Ecosystem

The transition of deferred payments from a novel growth hack to a heavily regulated financial product should not be viewed as a negative development. In many ways, it is a necessary maturation of the digital economy. The initial explosive growth of micro-credit was unsustainable without guardrails. As consumer awareness grows, evidenced by shifting habits and the realization that quick checkouts can have long-term impacts on financial milestones like securing a mortgage, the ecosystem is naturally self-correcting.

For merchants and payment professionals, this regulatory wave is an opportunity to build more resilient, trustworthy commerce experiences. The companies that will thrive in this new landscape are those that stop viewing compliance as a hurdle and start viewing it as a baseline for payment optimization. By building transparent checkout flows, graciously handling affordability-based declines, and utilizing intelligent systems to manage subsequent payment failures, merchants can protect their revenue while respecting the financial health of their customers.

Ultimately, the spotlight falling on these products today is a signal to the entire industry. The era of frictionless debt is evolving into an era of responsible, optimized commerce. Embracing this change, upgrading your technical infrastructure to handle complex authorizations, and refining how you manage payment issues will ensure that your business remains competitive, compliant, and highly profitable in the heavily scrutinized future of digital payments.