The digital environment is shifting rapidly. Fundamental assumptions about truth, identity, and digital authenticity are tested daily. A UC Berkeley professor recently captured this cultural moment by observing that things are getting weird online. Even seemingly straightforward media, like widely circulated photos of Mitch McConnell, are no longer trusted at face value. This deep-seated skepticism has moved beyond social media feeds and political discourse to actively rewire the underlying infrastructure of global commerce. When visual truth becomes malleable, the concept of digital identity becomes deeply suspect. For professionals managing revenue and digital transactions, this crisis of trust is not an abstract philosophical debate but a practical pain point within the payment processing flow. Issuing banks are tasked with protecting billions of dollars in capital against increasingly sophisticated synthetic identity fraud and AI-driven attacks. They are responding the only way they can by aggressively tightening their algorithmic risk models.

The Rising Tide of Algorithmic Skepticism

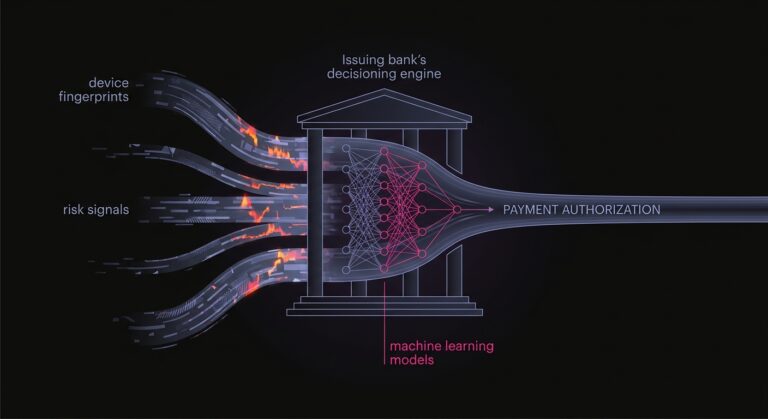

The payment ecosystem is built on a foundation of trust that is currently bearing unprecedented weight. When an issuing bank receives a request for payment authorization, it has mere milliseconds to determine whether the person clicking buy is the legitimate cardholder or a sophisticated bot leveraging stolen credentials. AI can now mimic voices, generate realistic identification documents, and automate checkout attacks at scale. As a result, traditional markers of trust are no longer sufficient.

To combat this, financial institutions rely heavily on complex machine learning models that assess hundreds of data points. These range from device fingerprints and IP velocity to behavioral biometrics and historical purchase patterns. However, these models are now fed increasingly volatile data from an unpredictable digital environment. This causes their parameters for what constitutes a safe transaction to narrow significantly.

Regulators and governments are highly aware of this paradigm shift. The UK Treasury recently initiated consultations focused on how to future-proof payment services. They are looking closely at the intersecting roles of stablecoins, artificial intelligence, and Open Banking. These initiatives highlight a global recognition that legacy payment architectures are struggling to balance robust security with seamless user experiences. For merchants, this systemic friction translates into a frustrating reality of unavoidable spikes in payment issues. When risk algorithms become overly defensive, perfectly legitimate customers get caught in the crossfire. This results in entirely avoidable payment failures. McKinsey estimates that of payment transactions typically fail across industries.

The Hidden Costs of Payment Blind Spots

When a legitimate transaction is stopped in its tracks, the damage extends far beyond a single lost sale. The opacity of contemporary payment networks creates a scenario where merchants often have little to no visibility into why a specific transaction failed. According to recent industry data, of CFOs say payment blind spots directly increase customer friction. This lack of transparency is a critical vulnerability. When finance and operations teams cannot clearly trace the root cause of a declined payment, they are unable to engineer a solution to prevent it from happening again.

The business impact of this friction is profound across all sectors. Systemic inefficiencies and opaque payment networks tie up critical working capital in the B2B space. This problem is severe enough that a construction fintech recently secured £2.9m in funding specifically to tackle industry payment delays. If multi-million dollar supply chains are choked by payment friction, the impact on high-volume, lower-margin B2C merchants is equally devastating.

When a customer encounters a transaction declined message at the checkout screen, the immediate result is embarrassment and frustration. Buyers in a highly competitive digital market rarely attempt a second card or contact their bank to resolve checkout issues. They usually just abandon the cart and move to a competitor. For subscription-based businesses, the stakes are even higher since payment issues are a leading cause of involuntary churn. An issuer risk model might randomly flag a renewal as suspicious. When this causes a recurring payment to decline, the merchant loses not just a single transaction but the entire lifetime value of that customer. PYMNTS reports that of consumers who experienced a false decline stopped shopping with the merchant where the decline occurred.

Engineering Trust Through Orchestration

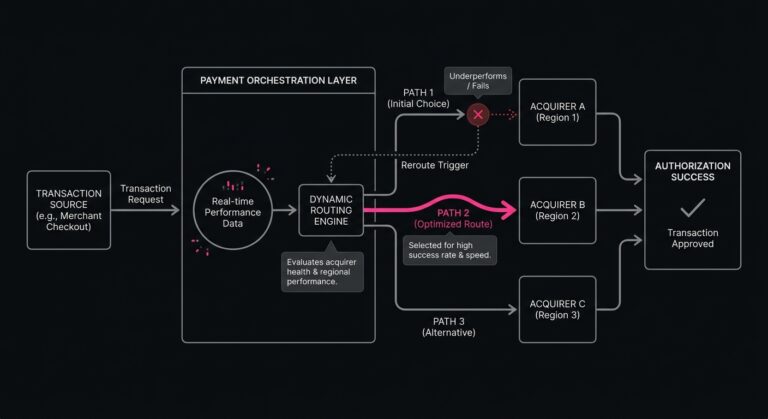

Navigating this complex landscape requires a fundamental shift in how organizations approach their payment infrastructure. Plugging into a single payment gateway and hoping for the best is no longer sufficient. This realization is driving the growing importance of payment orchestration across banking and enterprise commerce. Payment orchestration layers allow merchants to dynamically route transactions across multiple acquirers, processors, and geographic regions based on real-time performance data.

By utilizing an orchestration layer, payment teams can build sophisticated routing rules that optimize for the highest probability of success. A specific acquiring bank might experience an outage, or an issuer might suddenly reject a disproportionate number of cross-border transactions. In these scenarios, the orchestration engine can seamlessly route the transaction through a different pathway. This kind of dynamic payment optimization is critical for maintaining a high transaction approval rate in an unpredictable digital environment. Checkout.com cites merchant case studies where intelligent routing across multiple acquirers improved authorization rates by 2 to 5 percentage points.

However, orchestration alone is only part of the solution. Merchants must fundamentally change how they communicate trust to the issuing banks to truly reduce payment declines. This requires enriching the payment payload with as much verified data as possible. Implementing Network Tokens, selectively utilizing EMV 3-D Secure, and passing level 2 and level 3 data can provide issuers with the contextual confidence they need to approve the transaction. Giving the bank machine learning models clear and verifiable data cuts through the noise. This dramatically lowers the chances of triggering a false positive.

Decoding the Issuer Response

Even with the most optimized routing and enriched data payloads, some transactions will still fail. The key to effective revenue recovery lies in how a merchant system interprets and reacts to the issuer response. The issuing bank returns a decline code when a payment is rejected. Historically, many systems treated all declines as a binary failure. They handled a hard decline such as a closed account or stolen card exactly the same as a soft decline like insufficient funds or a temporary network timeout.

Understanding the nuance behind these codes is where the real work of payment recovery begins. Attempting to retry failed payments blindly without analyzing the underlying reason is not only ineffective but actively harmful. Issuing banks monitor merchant retry velocity. An issuer algorithm will classify a merchant as high-risk if they aggressively pummel the network with identical authorization requests for a card that has already been flagged as lost. This damages the overall trust score of the merchant and leads to even more payment declines across the board.

Payment teams must instead deploy highly surgical and context-aware logic. If a payment declines due to insufficient funds, the system should intelligently wait and retry the transaction on a date when the customer is statistically more likely to have a positive balance. Right after a traditional payroll cycle is an ideal time for this. If the decline is due to a temporary system error, a rapid retry through a secondary gateway might be the perfect solution. This analytical approach transforms payment failures from a total loss into a recoverable opportunity.

Bridging the Gap Between Risk and Revenue

Building and maintaining this level of granular and responsive logic internally is a massive engineering undertaking. It requires constant monitoring of global decline trends, deep integration with multiple processors, and the ability to update retry algorithms on the fly as issuer behavior changes. Diverting core engineering resources to manage the nuances of decline codes is simply not a viable trade-off for many organizations.

This is exactly where specialized recovery platforms provide outsized value. SmartRetry acts as an intelligent layer specifically focused on the nuances of payment optimization and automated recovery. By analyzing the exact nature of a decline and applying machine learning to determine the optimal timing, routing, and conditions for a secondary attempt, SmartRetry helps merchants recover lost revenue. It does this without risking their underlying processor reputation or overall transaction approval rates. The platform effectively handles the unpredictability of current authorization logic, allowing internal teams to focus on core product growth rather than chasing down failed transactions.

The friction between sophisticated fraud prevention and seamless customer experiences will only intensify over time. The algorithms protecting global capital are not going to become less vigilant. If anything, they will become more complex, opaque, and demanding of verifiable trust. Merchants who treat payment authorization as a static pass-fail event will continue to see their margins eroded by unexplained declines and involuntary churn. Conversely, those who treat payments as a dynamic conversation will build a highly resilient revenue engine. By optimizing their data payloads, orchestrating their routing, and intelligently managing their retries, these businesses will thrive no matter how unpredictable the digital environment becomes.