Decoding the MiCA License: How Crypto Regulation Reshapes Payment Approvals

March 8, 2026

![]() 12 min

12 min

Decoding the MiCA License: How Crypto Regulation Reshapes Payment Approvals

The European payment landscape is undergoing a profound shift as crypto-assets move out of the regulatory gray zone. For years, payment professionals treated digital asset transactions with extreme caution, and this approach was entirely rational. Issuers viewed crypto on-ramps as inherently high-risk while acquirers applied heavy scrutiny to merchant accounts handling these flows. The resulting friction created constant headaches for payment operations teams. Now, the Markets in Crypto-Assets (MiCA) regulation is rewriting those rules by introducing a comprehensive licensing framework across the European Union. More importantly, it bridges the gap between traditional fiat rails and blockchain networks. For merchants and payment service providers, this is not merely a compliance milestone. It represents a fundamental transformation in how transaction risk is communicated, assessed, and ultimately approved across the global payment ecosystem.

1. The Historical Friction in Digital Asset Flows

To understand the impact of the MiCA framework, we first have to look at how traditional payment networks historically handled digital assets. For a long time, the intersection of fiat currency and cryptocurrency operated with a massive trust deficit. Traditional banking systems are built on predictability, clear jurisdictional oversight, and established counterparty risk models. Because early iterations of crypto-asset exchanges lacked these elements, card networks and issuing banks naturally adopted a defensive posture.

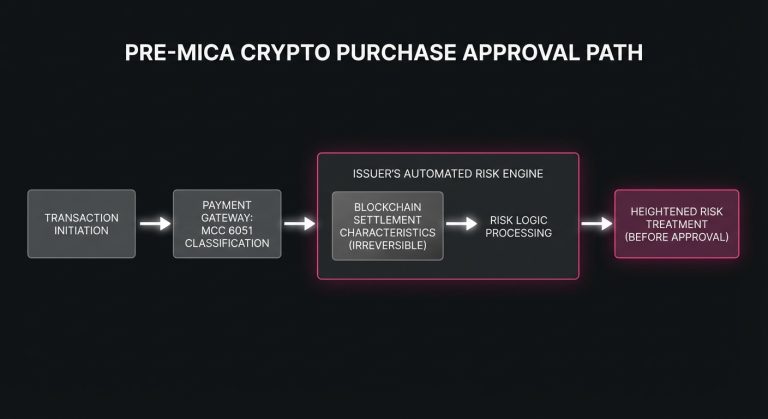

When a consumer initiated a transaction to purchase digital assets, the gateway routed the request using Merchant Category Code (MCC) 6051 for Quasi-Cash and cryptocurrencies. To an issuer’s automated risk engine, this MCC combined with the inherently irreversible nature of blockchain settlements triggered immediate red flags. The prevailing logic was simple: if a transaction involves an unregulated entity moving funds into an untraceable asset, the probability of fraud, money laundering, or account takeover is unacceptably high.

As a result, merchants operating in the digital asset space faced astronomical decline rates. A legitimate customer using their own card with sufficient funds would frequently encounter a generic payment declined message at checkout. These generic codes often defaulted to standard Do Not Honor or Suspected Fraud responses, providing payment operations teams with very little actionable data. You cannot optimize a payment flow when the underlying reason for the rejection is a blanket, system-wide block by the issuing bank.

2. What the MiCA License Actually Changes

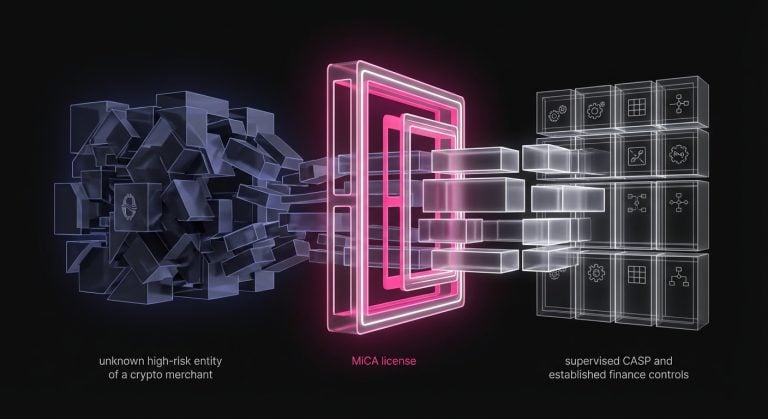

The Markets in Crypto-Assets regulation alters the foundational layer of this dynamic. By establishing a unified rulebook for the European Economic Area, MiCA creates a standardized legal entity known as the Crypto-Asset Service Provider (CASP). To obtain and maintain a MiCA license, a CASP must adhere to strict prudential requirements, maintain safeguarding protocols for client funds, implement robust governance structures, and comply with comprehensive anti-money laundering (AML) directives.

For the payment industry, this is the translation layer we have been waiting for. A MiCA license takes the operational reality of a crypto platform and maps it onto the risk vocabulary of traditional finance. When a merchant holds this license, they are no longer an unknown, unregulated offshore entity operating in a high-risk sector, but rather a regulated financial service provider operating under the supervision of European authorities. As of December 2025, 102 crypto-asset service providers had full MiCA authorization (Source).

This regulatory parity fundamentally alters the payment processing flow. Acquirers can now underwrite these merchants with confidence, knowing that a recognized authority continuously monitors their compliance. This confidence flows upstream to the card networks and crucially to the issuing banks who hold the ultimate decision-making power over transaction approvals.

The Shift in Issuer Perception

Issuing banks are inherently conservative, driven by the need to protect their cardholders and manage their own liability. Historically, their response to crypto flows was blunt. With the introduction of MiCA, however, issuers are beginning to refine their risk models. Instead of relying on rigid, rule-based blocks against any transaction categorized under crypto MCCs, they can now ingest the regulatory status of the merchant into their decisioning engines.

This shift allows issuers to rely on the merchant’s own Know Your Customer (KYC) and AML controls. If an issuer knows that the destination of the funds is a MiCA-compliant CASP, the perceived risk of the transaction drops significantly. The entity receiving the funds is legally bound to verify the identity of the purchaser and monitor the transaction for illicit activity. This shared burden of compliance is the exact mechanism that improves overall transaction approval rates.

3. Redefining Payment Authorization Under MiCA

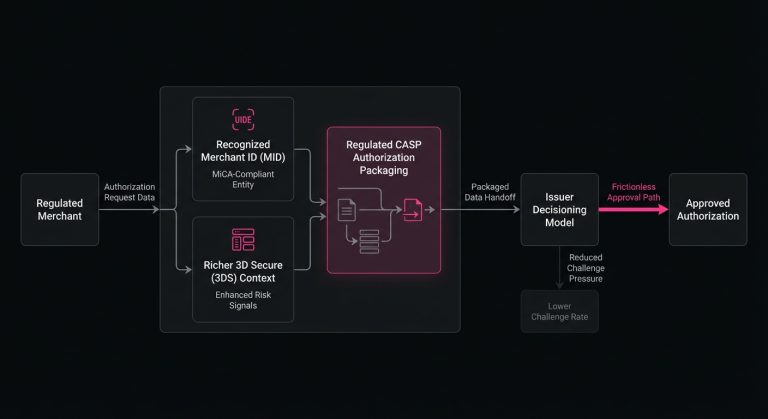

In the mechanics of a transaction lifecycle, the payment authorization request is a highly compressed conversation between a merchant and an issuer. Within milliseconds, data fields containing the transaction amount, merchant ID, terminal environment, and authentication data are transmitted, evaluated, and answered.

Before MiCA, the data elements associated with crypto merchants often lacked the contextual weight to override an issuer’s default skepticism. Now, acquirers and payment service providers can leverage a merchant’s licensed status to optimize how these authorization requests are packaged. While the ISO 8583 messaging standard does not have a dedicated field for a MiCA license, the broader ecosystem is signaling a change.

Payment operations teams can work with their acquirers to ensure that card issuer identifiers are properly registered and recognized as regulated financial institutions. Furthermore, the integration of 3D Secure (3DS) technology becomes much more effective. When a regulated CASP utilizes 3DS 2.x to pass rich device and contextual data to the issuer, the step-up challenge rate often decreases. The issuer’s risk model recognizes the combination of strong customer authentication and a regulated merchant environment. This results in a frictionless approval path that was previously impossible to achieve in the digital asset space.

4. E-Money Tokens and the Future of Settlement

Beyond authorization logic, MiCA introduces clear taxonomies for the assets themselves by explicitly defining Asset-Referenced Tokens (ARTs) and E-Money Tokens (EMTs). For payment professionals, the classification of EMTs is particularly fascinating. MiCA essentially defines EMTs, often colloquially referred to as stablecoins pegged to a single fiat currency, as a digital equivalent of traditional electronic money.

This classification has deep implications for the settlement layer of the payment ecosystem. If an EMT is legally recognized as e-money and subject to the same safeguarding and reserve requirements as funds sitting in a digital wallet or a prepaid card account, it can seamlessly integrate into standard treasury operations.

Merchants and payment processors may soon find themselves using MiCA-compliant EMTs for intra-day settlements, reducing their reliance on legacy correspondent banking networks. This capability accelerates the movement of funds, lowers foreign exchange friction, and provides merchants with faster access to working capital. The regulation effectively builds a secure bridge for stablecoins to function not just as speculative trading pairs, but as legitimate utility instruments within everyday payment operations.

5. Navigating Cross-Border Complexities

While MiCA provides absolute clarity within the European Economic Area, the payment industry is inherently global. A significant operational challenge arises when managing cross-border transactions, such as when a cardholder from the United States or Asia attempts to transact with a MiCA-licensed European CASP.

Global issuers do not immediately adopt European regulatory frameworks into their domestic risk models. A transaction that looks perfectly safe and compliant to a European acquirer might still trigger a high-risk alert for an issuer based in a different jurisdiction. Because of this discrepancy, payment operations teams must employ sophisticated routing and optimization strategies.

Managing these cross-border flows requires deep BIN lookup analysis. Teams must monitor issuer responses closely to identify which international banks recognize the lower risk profile of a MiCA entity and which still apply outdated heuristic blocks. By maintaining multiple acquiring relationships and routing transactions based on the cardholder’s region and the issuer’s historical behavior, merchants can mitigate the friction caused by uneven global regulatory standards.

6. Addressing Technical Friction and Payment Optimization

It is crucial to understand that regulatory clarity does not eliminate technical friction. While a MiCA license addresses the structural trust deficit, transactions will still fail for highly pragmatic reasons. Insufficient funds, temporary network latency, expired cards, and misconfigured gateway routing are persistent realities in any high-volume processing environment.

When a legitimate transaction fails, the merchant’s ability to recover that revenue depends entirely on their operational maturity. Blindly retrying a transaction without understanding the specific decline code is counterproductive because it frustrates the consumer and inflates transaction costs. It can also actively damage the merchant’s standing with card networks by artificially spiking decline ratios.

Intelligent handling of payment failures requires parsing the exact nature of the issuer’s response. If a transaction is declined due to a hard error, such as a lost or stolen card, retrying the request is futile. However, if the decline is a soft error like a temporary timeout or a transient risk flag, there is a strategic window for recovery.

This is the operational layer where specialized infrastructure becomes necessary. Platforms like SmartRetry focus specifically on this challenge by automating payment optimization and executing intelligent retries based on data science rather than guesswork. By analyzing the time of day, the specific issuer, network conditions, and historical approval patterns, merchants can retry failed payments strategically to maximize their chances of success. This targeted approach to payment recovery ensures that revenue is captured without triggering velocity limits or unnecessarily alarming the issuer’s fraud prevention systems.

The Role of Intelligent Timing

The timing of a retry is often just as important as the data payload itself. Network congestion or temporary batch processing windows at the issuing bank can cause seemingly random failures. A sophisticated recovery strategy involves implementing calculated delays and waiting for the optimal moment when the issuer’s systems are most likely to return an approval. This naturally lifts the merchant’s overall conversion metrics.

7. The Operational Shift for Product and Strategy Teams

For leaders in fintech and payment product management, the arrival of MiCA requires an immediate strategic review of existing infrastructure. Operating a payment stack in a regulated environment is fundamentally different from operating in an unregulated one, shifting the focus from merely trying to keep merchant accounts open to actively optimizing the unit economics of every transaction.

Product teams must work closely with compliance to ensure that the checkout user experience does not degrade from excessive data collection while still satisfying the rigorous KYC standards demanded by the regulation. This balancing act requires seamless integrations with identity verification providers and dynamic risk engines that can assess the user’s profile in real-time.

Furthermore, dispute management processes must be modernized. Historically, merchants dealing in digital assets struggled to defend against chargebacks because networks often sided with the cardholder in cases of friendly fraud. Under MiCA, licensed entities operate with the same rights and obligations as any other merchant. Thanks to robust identity verification and clear regulatory standing, CASPs are now in a stronger position to provide compelling evidence in dispute representments and protect their revenue from unjustified reversals.

8. Analyzing Issuer Metrics and BIN Performance

To fully capitalize on the regulatory advantages provided by a MiCA license, merchants must become obsessed with their data. The aggregate approval rate is no longer a sufficient metric. Payment operations professionals must drill down into performance by Bank Identification Number (BIN) to identify exactly which issuers are rewarding their compliant status and which are lagging behind.

If a specific issuer continues to exhibit unusually high decline rates for a fully licensed merchant, that data becomes a vital tool for negotiation. Acquirers can take this performance data directly to the card network to demonstrate that the issuer is inappropriately penalizing a regulated entity. Over time, this feedback loop forces the wider ecosystem to adjust and slowly drags legacy risk models into the modern era.

This analytical approach also dictates how new markets are entered. Before launching operations in a new member state, payment teams should analyze the historical behavior of the dominant issuers in that region. This helps set realistic expectations for initial conversion rates and allows teams to prepare targeted optimization strategies to manage the expected friction.

9. The Broader Ecosystem Impact

The second-order effects of the MiCA framework will ripple outward, influencing jurisdictions far beyond the borders of the European Union. Because global regulators are closely watching the European experiment, other regions are likely to adopt similar frameworks once MiCA proves that it is possible to integrate digital assets into the traditional financial system without compromising systemic stability. TRM Labs reviewed crypto policy developments across 30 jurisdictions in 2025, representing over 70% of global crypto exposure (Source).

For the payment industry, this means the eventual standardization of crypto flows on a global scale. The days of treating digital assets as an edge case or a specialized, high-risk vertical are coming to an end. Instead, they are becoming just another asset class subject to the same rules of settlement, authorization, and risk management as traditional fiat currencies or equities.

This normalization allows payment service providers to build more cohesive, universal platforms. Instead of maintaining separate technical stacks for fiat and crypto merchants, infrastructure providers can unify their offerings. They can apply the same advanced routing, fraud prevention, and recovery mechanisms across their entire portfolio. The ultimate beneficiary of this consolidation is the end consumer, who experiences a more reliable, predictable, and secure purchasing journey.

The intersection of regulatory compliance and payment technology is often viewed as a constraint, perceived as a set of rules that slows down innovation and adds operational overhead. However, in the context of digital assets, regulation is proving to be the exact opposite. It acts as the catalyst that removes structural barriers to entry. By providing a clear definition of trust, the MiCA license empowers merchants and payment professionals to move past the defensive tactics of the past decade. The industry can finally focus on what it does best: refining the authorization process, streamlining the movement of value, and optimizing the mechanics of modern commerce.

Still letting failed transactions slip through?

SmartRetry turns declines into approvals - automatically, intelligently, and without changing your payment provider.

Frequently asked questions about this topic

Share this article

Author

Roi Lagziel

Roi Lagziel is a payments engineer specializing in authorization optimization, retry strategies, and issuer-level behavior. His work focuses on building practical, data-driven systems that help payment teams reduce false declines and recover lost revenue.

Read all articles >