Merchant Discount Rate Explained: How Payment Teams Can Reduce Costs and Improve Approvals

March 18, 2026

![]() 14 min

14 min

Every time a customer clicks a checkout button, a complex financial relay race begins. Within milliseconds, data changes hands across multiple networks as value is verified, secured, and ultimately transferred from consumer to merchant. But this invisible machinery does not run for free. Sitting right in the middle of this payment processing flow is the Merchant Discount Rate, or MDR. For many businesses, MDR is simply viewed as a necessary tax, a non-negotiable line item on the monthly profit and loss statement. However, treating payment processing costs as a static penalty misses a massive opportunity for financial efficiency. If you peel back the layers of how these fees are calculated, you quickly realize that MDR is highly dynamic and context-dependent. It responds to transaction routing, data presentation, and how you handle scenarios where a payment is flagged or stalled by the network. Understanding the mechanics of MDR changes the operational conversation from asking how much you are paying to asking how efficiently you are running your checkout infrastructure.

The Invisible Architecture of Payment Fees

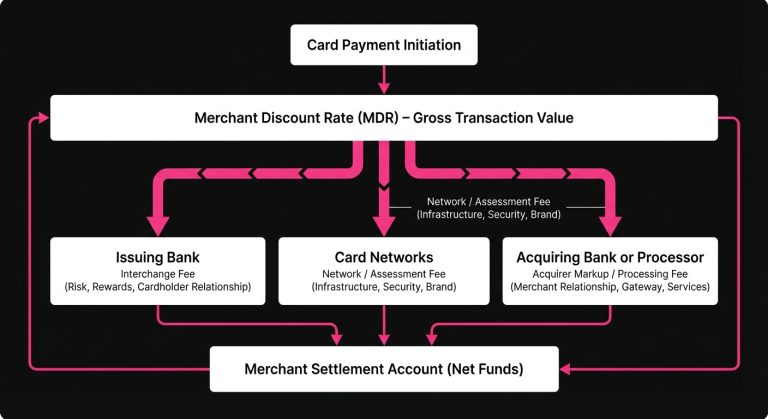

When a business accepts a credit or debit card payment, the fee deducted before the funds settle into their merchant bank account is the MDR. While it often feels like a single monolithic charge, it is actually a composite of three distinct fees, each distributed to a different participant in the payment ecosystem. To optimize these costs, payment operations teams must first understand exactly who gets paid and what risk or service that payment covers.

The Three Pillars of the Merchant Discount Rate

The total fee is divided among the issuing bank, the card networks, and the acquiring bank or processor. Each component behaves differently and offers different optimization opportunities.

- Interchange Fees: This is typically the largest chunk of the MDR, paid directly to the issuing bank that provided the customer with their card. It compensates the issuer for taking on the credit risk of the transaction, managing the consumer account, and funding rewards programs. Interchange is non-negotiable and strictly set by the card networks, but it is highly variable based on the transaction type, card type, and geographic region.

- Scheme Fees (Assessments): Paid to the card networks themselves, such as Visa or Mastercard, for the privilege of utilizing their global infrastructure and switching technology. These are generally smaller fixed percentages or per-transaction cents. While the baseline assessments are static, networks often levy additional nuanced fees based on cross-border elements or the use of specific network services like tokenization or account updater tools.

- Acquirer Markup: The fee paid to your acquiring bank or Payment Service Provider (PSP) for facilitating the transaction, communicating with the networks, and settling the funds into your account. Because this fee is set by the processor in exchange for their technology and services, it is the only truly negotiable piece of the MDR pie.

The Role of Payment Facilitators vs. Direct Acquirers

The architecture of your processing partner also influences your costs. Modern Payment Facilitators (PayFacs) aggregate thousands of merchants under a single master merchant account. This makes onboarding incredibly fast and developer-friendly, but it often requires the PayFac to charge a standardized, slightly higher margin to absorb the collective risk. Conversely, establishing a direct relationship with an acquiring bank requires more rigorous underwriting and setup, but it often yields lower, highly customized acquirer markups tailored to your specific processing volume and risk profile.

Decoding the Pricing Models: Finding the True Baseline

The way your payment service provider bundles interchange, scheme fees, and their own markup dictates your visibility into your true operational costs. Processors generally offer a few main pricing structures, and choosing the correct one is often the first major decision in any payment optimization strategy. If you cannot see the underlying components of your fees, you cannot effectively optimize them.

The Opaque Reality of Tiered Pricing

In a tiered pricing model, the processor sorts your transactions into broad categories, typically labeled as Qualified, Mid-Qualified, and Non-Qualified. A standard, low-risk debit card might be deemed Qualified and receive the lowest rate, while a premium rewards credit card or an international transaction gets downgraded to Non-Qualified, incurring a massive fee spike. The structural flaw here is that the processor alone decides the criteria for these tiers. Merchants often observe their rates creeping upward as processors silently shift more transaction profiles into the expensive Non-Qualified buckets, making this model generally unfavorable for growing businesses.

The All-in-One Illusion of Blended Pricing

Blended pricing takes the complexity of interchange, scheme fees, and markup, and flattens it into a single predictable rate, such as 2.9% plus 30 cents. It is easy to understand, simple to reconcile, and requires zero deep payments expertise to manage. This predictability, however, comes at a premium. Because the processor is absorbing the underlying variability of interchange costs, which fluctuate depending on the card used, they must pad their margin to protect themselves against expensive transactions. If a customer uses a highly regulated, low-cost debit card that only costs a fraction of a percent in interchange, you still pay the flat 2.9%. The processor pockets the significant difference.

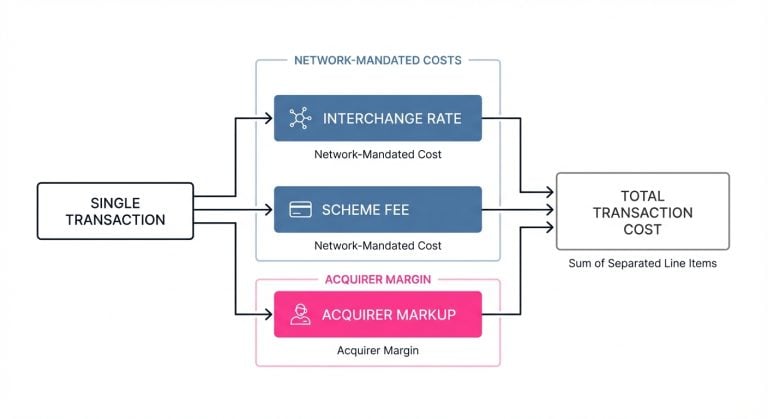

The Structural Transparency of Interchange++

Interchange++ (often abbreviated as IC++) unbundles the fees completely. Under this model, you pay the exact interchange rate mandated by the network, the exact scheme fee, plus a clearly defined, pre-negotiated markup to the acquirer. If a specific transaction costs 0.2% in interchange, that is exactly what you pay, plus your acquirer’s margin. This model requires more sophisticated accounting reconciliation, as your monthly statement will show hundreds of different line items based on card types, regions, and capture methods. However, for mid-market and enterprise merchants, Interchange++ is almost always the most cost-effective structure. It allows you to see exactly where your margin is going and exposes the structural inefficiencies in your checkout that are driving up costs.

The Hidden Drivers That Multiply Your Processing Costs

Once you have visibility into your fees through a transparent pricing model, you begin to notice that not all transactions are created equal. The network rules that govern interchange and scheme fees are incredibly granular, penalizing certain transaction profiles while rewarding others. Understanding these drivers is the key to actively managing and reducing your baseline MDR.

Card Composition and the Cost of Rewards

A standard consumer credit card carries a relatively manageable interchange rate. A premium, high-tier rewards card, however, costs significantly more to process. The cash-back bonuses, airline miles, and concierge services that consumers love are largely funded by the merchant via higher interchange fees. Corporate and commercial purchasing cards are even more expensive. If your platform heavily processes corporate cards, your baseline MDR will naturally sit higher than a standard consumer retailer. You cannot control what card a customer pulls out of their wallet, but understanding your ticket size and card mix is essential for projecting processing costs accurately.

Regional Regulations and Cross-Border Penalties

Geography plays a massive role in payment costs due to varying regulatory environments. In regions like the European Union, interchange fees for consumer cards are heavily capped by legislation, making payment processing structurally cheaper. In the United States, while debit interchange is regulated for large banks under the Durbin Amendment, credit card interchange remains largely unregulated and significantly higher. Cross-border transactions are also notorious margin killers. When a customer in the UK buys from a US-based merchant entity, the transaction incurs cross-border scheme fees and often elevated interchange rates. Global merchants relying on a single domestic acquirer to process international volume frequently experience inflated MDRs.

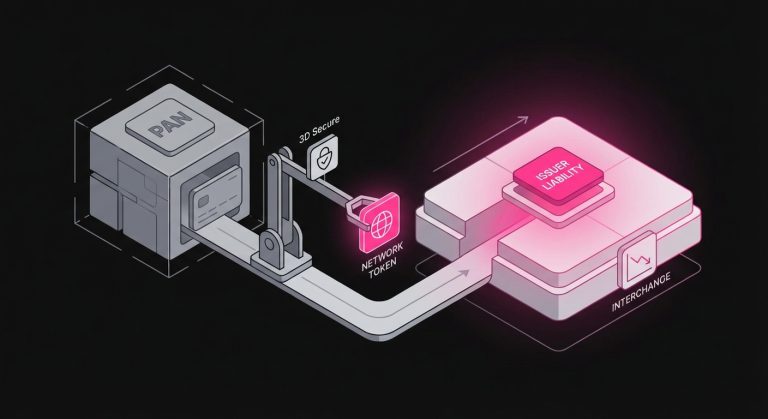

Network Tokens and the Shift in Liability

Networks assess risk based on how a payment is captured and authenticated. In the digital realm, card-not-present transactions inherently carry a higher risk of fraud than in-store purchases, which is reflected in higher e-commerce interchange rates. For example, one 2026 fee breakdown put card-present retail EMV/contactless interchange at 1.50% + $0.10, versus 1.80% + $0.10 for eCommerce card-not-present transactions (Source). Merchants, however, can utilize network tokens and 3D Secure authentication to alter this dynamic. By replacing a primary account number, or PAN, with a secure network token, or by stepping up authentication through 3D Secure, the merchant effectively mitigates fraud risk and shifts liability back to the issuer. In return for this enhanced security, card networks frequently reward these transactions with lower interchange rates.

Strategic Cost Optimization: Pulling the Operational Levers

Lowering your MDR is not solely about aggressive contract negotiations with your acquirer. It relies heavily on structuring your payment data and routing logic to align with network preferences, giving you distinct operational levers that can materially impact the rates you pay on a per-transaction basis.

Passing Enriched Data: Level 2 and Level 3 Processing

For B2B merchants processing a high volume of corporate cards, passing enhanced transaction data is one of the most effective ways to lower interchange costs. Corporate cards are expensive because issuers view large B2B purchases as higher risk and require more administrative overhead. By passing Level 2 and Level 3 data, which includes granular invoice-level details such as line-item descriptions, exact tax amounts, freight charges, and purchase order numbers, you provide the issuer with a comprehensive view of the purchase context. This transparency significantly reduces the perceived risk, prompting the networks to reclassify the transaction and reward the merchant with a substantially lower interchange rate that can yield major cost savings over time. The scale of the opportunity is large in B2B, with total annual B2B payment volume estimated at $150T-$180T USD in 2026 (Source).

Intelligent Routing and Multi-Acquiring Strategies

If you process significant volume internationally, routing transactions through local acquirers is a powerful structural change. By establishing legal entities or utilizing merchant-of-record models in key global markets, you can process transactions domestically rather than cross-border. A transaction that might incur a high cross-border penalty fee could drop significantly in cost when routed through a local acquiring bank in the customer’s region. Beyond direct cost savings, local routing often yields a more favorable payment authorization response from regional issuers, directly improving your overall success rates.

The Art of Acquirer Negotiation

While operational optimizations reduce the interchange and scheme components of your MDR, the acquirer markup remains the variable you can negotiate. Approaching these negotiations requires preparation, data, and a clear understanding of your own risk profile.

Moving Beyond Gross Volume

Many merchants assume that processing high transaction volume automatically entitles them to lower acquirer markups. While volume is important, acquirers care equally about risk and operational overhead. A merchant processing $50 million annually with high chargeback rates, erratic processing spikes, and frequent payment issues is far less attractive, and more expensive to support, than a merchant processing $20 million with pristine, predictable, and low-risk transaction flows. When negotiating, presenting a clean risk profile, low fraud metrics, and a well-managed chargeback ratio provides far more leverage than volume alone.

Benchmarking and Ongoing Audits

Payment pricing is not a set-it-and-forget-it exercise. Card networks update their interchange tables and scheme fee structures biannually, typically in April and October. Processors often adjust their own pricing or introduce new ancillary fees alongside these network updates. Regularly auditing your processing statements ensures that your acquirer is passing through network changes accurately and that your negotiated margin remains competitive relative to current market benchmarks. For example, Mastercard’s 2025-2026 US Region Interchange Programs list a Restaurant rate of 1.19% + 0.10 (Source).

The Interplay Between Declines, Retries, and Margin

Payment optimization extends far beyond the successfully cleared transaction. How you operationalize your response when you encounter checkout issues has a direct impact on both your bottom line and your overall cost of acceptance. Repeatedly hitting the networks with failing transactions is an incredibly expensive habit that damages profitability.

Distinguishing Between Hard and Soft Declines

To manage costs effectively, merchants must differentiate between the types of issuer rejections. A hard decline occurs when a transaction is permanently blocked, often due to a lost, stolen, or expired card, or a closed account. Attempting to retry a hard decline is futile because it will never succeed and only incurs unnecessary processing fees. A soft decline, however, is temporary. It might result from a temporary lack of funds, a suspected but unconfirmed risk flag, or a momentary timeout in the network’s processing flow. These soft declines present an opportunity for recovery, provided they are handled delicately.

The True Cost of Aggressive Retries

When a card is declined, the immediate reflex for many merchants, especially in subscription billing models, is to attempt the transaction again. While some retries are necessary, blindly hammering the network with repeated, rapid-fire attempts incurs authorization fees for every single ping regardless of the outcome. Worse, aggressive retry logic can actively harm your merchant profile. If issuers associate your merchant ID with a high volume of payment failures and frantic, poorly timed retry attempts, their risk algorithms may begin to throttle your approvals across the board. This degrades your overall issuer response, driving down baseline authorization rates and increasing your cost of revenue acquisition.

Intelligent Recovery Workflows

Recovering revenue requires a strategic, data-informed approach rather than brute force. When facing a declined transaction, particularly involving recurring billing or subscription payment issues, the operational goal is to recover the revenue with the fewest, highest-probability attempts.

Platforms like SmartRetry focus specifically on this complex layer of payment optimization, utilizing intelligent retry logic that analyzes specific issuer behaviors, network decline codes, and historical timing patterns to recover failed payments efficiently. By mapping the correct retry strategy to the exact reason a transaction stalled, such as waiting for a high-probability day of the week to retry an insufficient funds error, merchants can successfully retry failed payments and recover revenue. This methodical approach helps reduce payment declines and significantly boosts the transaction approval rate, all without racking up unnecessary authorization penalties or damaging the merchant’s standing with issuing banks.

Engineering a More Profitable Payment Infrastructure

Historically, payment teams have focused almost entirely on basic utility by keeping the checkout operational and ensuring money moves from point A to point B. In that paradigm, the Merchant Discount Rate was simply the toll paid to the networks. But as digital commerce has matured, the role of payment operations has shifted from a back-office necessity to a strategic growth lever.

The Compounding Effect of Granular Optimization

When you actively optimize your payment infrastructure, the financial results compound rapidly. Moving from an opaque pricing model to Interchange++ brings immediate transparency, while implementing Level 3 data protocols or adopting network tokenization shaves crucial basis points off your baseline interchange costs. Routing internationally through local acquirers eliminates heavy cross-border penalties. Managing payment issues with intelligent, data-driven retry logic ensures you are not squandering hard-earned margin on doomed authorization attempts. Together, these incremental structural improvements can rescue hundreds of thousands, if not millions, of dollars in margin for a high-volume enterprise.

Realigning the Checkout Strategy

It is important to remember that the ultimate goal is not always to achieve the absolute lowest possible MDR in a vacuum. If you implement incredibly rigid fraud filters to block all moderately risky transactions, your interchange rates might drop, but your top-line revenue will plummet due to false declines and lost customers. True optimization is about finding the operational sweet spot where you are paying fair market value for the risk and value of each transaction, maximizing your successful approvals while ruthlessly eliminating structural inefficiencies.

The global payment ecosystem will always remain complex, with issuers, acquirers, and card networks constantly adjusting their rules, rates, and routing algorithms. Within that shifting complexity, however, lies the opportunity for operational differentiation. By treating your Merchant Discount Rate not as a static, unavoidable bill, but as a dynamic reflection of your underlying payment architecture, you gain the ability to engineer better outcomes. This requires looking beneath the surface of the standard monthly processing statement, questioning the default settings of your acquiring partners, and actively designing a transaction flow that works in your favor. When a business stops accepting its payment processing costs as a given, it unlocks a powerful operational advantage, turning the intricate mechanics of global payments into a measurable, sustainable engine for profitability.

Still letting failed transactions slip through?

SmartRetry turns declines into approvals - automatically, intelligently, and without changing your payment provider.

Frequently asked questions about this topic

Share this article

Author

Roi Lagziel

Roi Lagziel is a payments engineer specializing in authorization optimization, retry strategies, and issuer-level behavior. His work focuses on building practical, data-driven systems that help payment teams reduce false declines and recover lost revenue.

Read all articles >More in Uncategorized:

March 8, 2026

Why Virtual Card Payments Fail in Travel and How Payment Teams Improve Approval Rates

This article explains why travel virtual cards fail at hotels and what operators can do to recover approvals, cut manual intervention, and protect margins across issuing and acquiring.

March 8, 2026

Decoding the MiCA License: How Crypto Regulation Reshapes Payment Approvals

This article explains how MiCA helps crypto merchants and PSPs translate compliance into stronger issuer trust, smarter authentication, and better payment approval performance across regulated flows.

March 8, 2026

The Hidden Mechanics of Cross-Border Card Declines

This article explains why international card transactions underperform, from issuer risk models to data mismatches and recurring billing gaps, and shows operators where to act to recover revenue and reduce false declines.