The payments ecosystem is undergoing a quiet but massive shift. Issuers are no longer acting as passive vaults holding onto customer deposits. Instead, they are actively mapping and anticipating the exact moments money enters and exits an account. This changes everything for merchants trying to process a transaction. When you understand how an issuer views a consumer’s financial rhythm, you stop guessing and start aligning your billing strategies with reality. For merchants, navigating payment failures means acknowledging that the banks on the other side of the transaction are playing a much more sophisticated game than they were a decade ago.

The Invisible Engine Behind Authorization

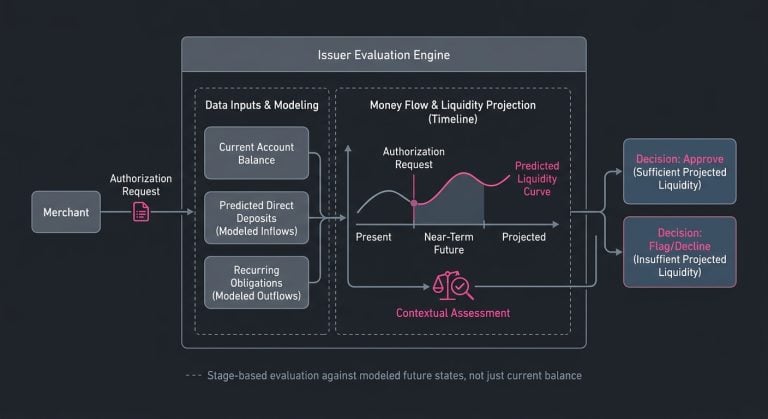

For a long time, the relationship between an issuer and a consumer was relatively static. Funds cleared, balances updated, and when a merchant requested an authorization, the logic was largely binary: either the funds were present or they were not. Risk models were heavily reliant on simple velocity checks and basic geographical mismatch logic.

Today, the issuers pulling ahead in the market are those building deep, predictive models into their customers’ money flows. They know when direct deposits hit, exactly how long it takes for funds to settle, and what the typical recurring obligations look like for a specific account. They are categorizing spend dynamically and predicting liquidity gaps before the consumer even realizes they are running low on funds.

When a merchant initiates a transaction, that request enters a payment gateway that is scrutinized by these highly tuned models. The issuer isn’t just checking a ledger balance. They are evaluating the probability that the requested funds belong to a predictable cadence of income and outflow. If a merchant’s request lands at an awkward moment in that flow, say, a day before the expected payroll deposit or sandwiched between two historically large utility drafts, the issuer’s models might flag the transaction. Understanding this dynamic is the first step toward moving away from blind processing and toward strategic alignment.

Moving From Custodians to Active Flow Managers

Issuers are investing heavily in understanding money flows because predictability equals profitability. By analyzing behavioral data, issuers can offer features like early direct deposit, automated overdraft protection, and timely short-term credit offers. They are integrating into the financial lives of their users so deeply that they become indispensable.

For the merchant, this issuer sophistication presents both a challenge and an opportunity. When an issuer rejects a transaction, they are communicating a specific state of the customer’s financial flow at that exact microsecond. A transaction declined message is rarely a permanent judgment on the customer’s intent to pay. It is often simply a timing issue. The funds might be held in pending status, shifted to a savings pocket, or simply waiting for the next morning’s clearing cycle.

Merchants who view issuers merely as gatekeepers miss the broader picture. The banks winning the consumer loyalty war are doing so by actively orchestrating liquidity. If a merchant attempts to force a transaction through without respecting that orchestration, the friction ultimately falls back on the merchant’s bottom line in the form of lost revenue and increased processing costs.

Why Timing Is Everything in Recurring Billing

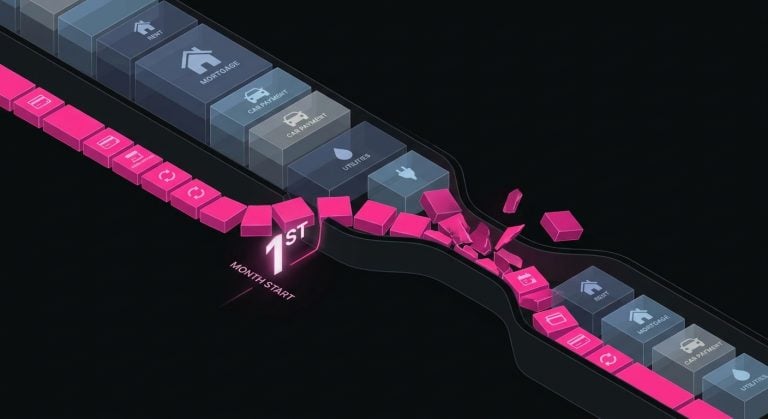

Nowhere is the impact of money flows more apparent than in the recurring billing space. Subscription businesses thrive on predictability, but they frequently shoot themselves in the foot by relying on rigid, calendar-based billing schedules.

There is a long-standing myth in retail and digital subscriptions that the first of the month is the optimal time to bill a customer. While it is true that many people receive paychecks or government benefits on the first, it is also the exact day that rent, mortgages, car payments, and utilities are drafted. Wallets are heavily congested, so when a merchant attempts to process a charge amidst this heavy traffic, subscription payment issues are almost guaranteed to spike. The issuer’s risk models see a rapid succession of debits and may temporarily lock the card, or the account simply hits a localized liquidity trough.

The most successful subscription models observe the natural cadence of their users. If a customer historically has a successful authorization on the 15th of the month, arbitrarily moving their billing date to the 1st purely for the sake of the merchant’s accounting convenience introduces unnecessary friction. Understanding when an issuer typically sees funds clear for a specific user demographic allows a merchant to time their billing requests to hit when the account is flush, rather than when it is heavily contested.

Decoding the Decline: What Issuers Are Actually Saying

When a merchant receives a card declined response, the immediate reaction is often to try again or to reach out to the customer. However, the specific response code provided by the issuer contains vital clues about the underlying money flow.

Decline codes broadly fall into two categories: soft declines and hard declines. Hard declines, such as a stolen card, closed account, or invalid card number, are terminal. No amount of waiting or timing will turn a closed account into an approved transaction. Soft declines, however, are where the opportunity for optimization lies.

The most common soft decline is insufficient funds decline. In the context of an issuer managing money flows, an NSF does not necessarily mean the customer is broke. It simply means the funds are not available at that specific moment. Another frequent and notoriously vague code is Do Not Honor. This code is often used as a catch-all when the issuer’s risk models are tripped by something outside the normal pattern of behavior, but it does not expressly forbid future attempts.

Experienced payment teams know that treating an NSF decline exactly the same as a Do Not Honor decline is a fast track to wasted processing fees. The issuer is providing feedback based on their internal models. If you ignore that feedback and repeatedly hammer the network with identical requests, you risk damaging your merchant trust score with that issuer, leading to an overall degradation of your authorization rates across the board. For online merchants, around 85% is considered a strong bank authorization rate (Source).

The Merchant Playbook for Aligning With Money Flows

Adapting to this environment requires a shift in how merchants manage their payment operations. It is no longer enough to simply integrate with a payment gateway and hope for the best. Proactive payment optimization is required to navigate the complexities of issuer behavior today.

Shifting Away From Static Rules

Historically, merchants relied on static dunning schedules to manage declines. A common approach was to attempt a retry on day one, day three, and day five following the initial failure. This logic is fundamentally flawed because it ignores the reality of how banking systems operate. Weekends and bank holidays affect clearing times, meaning a transaction that failed on a Friday due to insufficient funds is highly unlikely to succeed on a Saturday since no new deposits will have cleared.

Optimizing these requests means analyzing historical decline data to identify patterns, such as whether your customers tend to have higher approval rates on Fridays or if the second half of the month shows a dip in liquidity for a specific market segment. Aligning your processing schedule with these observed tendencies drastically improves the chances of capturing the funds smoothly.

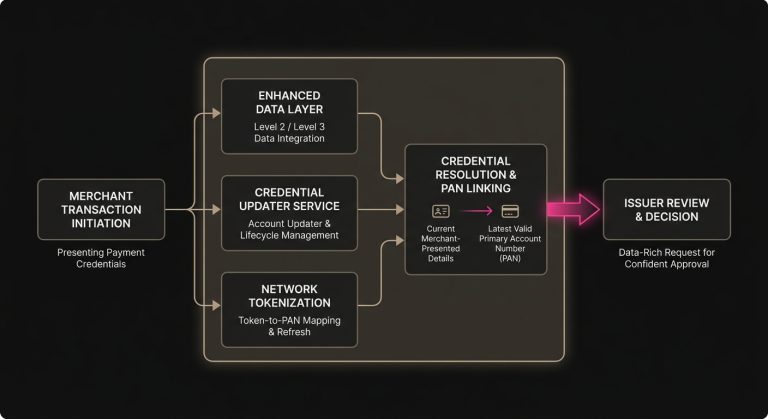

Embracing Data-Rich Transactions

Issuers want confidence. The more context a merchant can provide about a transaction, the more likely the issuer’s risk models will allow it to proceed. Passing additional data elements, often referred to as Level 2 or Level 3 data, gives the issuer a clearer picture of what is being purchased and who is making the purchase.

Utilizing network tokens and account updater services ensures that the payment credentials being presented are as current as possible. When an issuer issues a new card to a customer, they seamlessly map the old token to the new primary account number behind the scenes. Merchants utilizing these tools signal to the issuer that they are operating a sophisticated, secure payment environment, which naturally aligns with the issuer’s goal of protecting the customer’s money flow.

Rethinking the Retry Strategy Without Breaking the Bank

When a legitimate transaction fails, the natural impulse is to try again. However, aggressive and blind retries are actively penalized today. Card networks like Visa and Mastercard have implemented strict rules and associated scheme fees to discourage merchants from repeatedly submitting failed authorization requests.

To retry failed payments effectively, merchants must balance the desire to recover revenue with the operational cost of the retry attempts. Attempting to charge a card six times in a single week for a ten-dollar subscription will likely cost more in processing and penalty fees than the subscription is actually worth, while also risking having the merchant identifier flagged for abusive behavior by the issuer.

This is where intelligent infrastructure becomes highly valuable. Platforms like SmartRetry are designed to handle the complexities of payment optimization by applying dynamic logic to declined transactions. Rather than relying on rigid calendars, these systems analyze the specific decline codes, card types, and historical success patterns to determine the precise moment a retry is most likely to succeed. This helps merchants intelligently recover revenue and improve their transaction approval rates without running afoul of network rules. Smart routing can recover up to 5% of declined transactions as approvals (Source).

The Nuance of the Processing Window

Understanding the processing window is another critical element. Some acquirers process transactions in batches, while others operate in real-time. If you are timing a retry based on the assumption that a direct deposit clears at midnight, but your acquirer batches transactions at 2:00 AM, you might miss the optimal window if the issuer updates balances at 3:00 AM.

Experienced payment operations teams map these timelines closely. They understand the time zones of their primary customer base, the batch times of their payment service providers, and the typical maintenance windows of the major issuing banks. It sounds incredibly granular, but in high-volume environments, optimizing for these micro-timing events can yield significant revenue recovery that would otherwise be written off as bad debt.

The Trade-Offs of Intelligent Payment Recovery

Every decision in payment processing involves a trade-off. The pursuit of the perfect authorization rate must be weighed against the realities of customer experience and operational overhead.

When a transaction fails, a merchant generally has two paths: silent recovery or active dunning. Silent recovery involves utilizing smart retries and network tools to capture the funds without ever bothering the customer. This provides the best customer experience since the subscriber never realizes there was an issue, but it does take time. If a merchant’s service delivery requires immediate payment, such as a food delivery app or a ride-sharing service, silent recovery is not a viable option. The transaction must be approved immediately or the service cannot be rendered.

Active dunning involves reaching out to the customer via email, SMS, or in-app notifications to request updated payment information. This is highly effective for hard declines, but it introduces friction. For a digital subscription, forcing a user to log in and update a credit card is often the exact moment they decide to evaluate whether they actually need the service, leading directly to voluntary churn.

Effective payment recovery requires segmenting these approaches based on the product, the customer’s history, and the specific decline reason. You rely on intelligent retries for soft declines where time is on your side, and you reserve active outreach for scenarios where the payment method is clearly unrecoverable.

Bridging the Gap Between Acquirer and Issuer

The fundamental tension in the payments ecosystem often stems from the gap in perspective between the acquiring bank, representing the merchant, and the issuing bank, representing the consumer. Acquirers are incentivized to push transactions through to generate volume, while issuers are focused on protecting the consumer’s funds and mitigating risk.

When issuers pull ahead by building into customers’ money flows, they are essentially raising the bar for the rest of the ecosystem. They are demanding that acquirers and merchants treat the authorization process as a conversation rather than a simple command.

Merchants bridge this gap by maintaining clean, well-managed payment hygiene. This means avoiding the temptation to force transactions through via multiple gateway routing without a clear, data-driven reason, and respecting the issuer’s response codes by adjusting processing cadence accordingly. When an issuer recognizes a merchant as a responsible actor in the ecosystem, one who does not bombard the network with invalid requests, that merchant often enjoys subtly higher approval rates simply because their traffic is deemed lower risk.

Where the Ecosystem Is Heading

The days of viewing a payment as a disconnected, standalone event are over. Financial institutions are moving toward a highly synchronized environment heavily influenced by open banking, instant payment rails, and predictive artificial intelligence. The concept of a customer’s money flow will only become more transparent and real-time.

In the near future, we will likely see issuers providing even more nuanced feedback to the merchants who are equipped to interpret it. Instead of a generic decline, the data exchange might indicate exactly when funds will be available, allowing for perfectly timed, frictionless processing.

Until then, the advantage belongs to the teams who are paying attention to the signals currently available. The issuers have already figured out that money is fluid, behavioral, and highly predictable. They have built their infrastructure around this reality to protect their customers and grow their portfolios. The merchants who recognize this shift, analyze the rhythms of their own transaction data, and adopt intelligent, respectful billing practices are the ones capturing the revenue that others leave behind. They understand that a declined transaction is rarely a closed door. More often than not, it is simply a matter of finding the right moment to knock.

Still letting failed transactions slip through?

SmartRetry turns declines into approvals - automatically, intelligently, and without changing your payment provider.

Frequently asked questions about this topic

Issuers increasingly assess predicted income, spending cadence, and liquidity timing, not just current balance. Merchants that align billing to those patterns can reduce avoidable declines.

Hard declines are unrecoverable, like closed accounts or invalid cards. Soft declines, such as insufficient funds or do not honor, may succeed later with better timing or updated data.

Static retries ignore clearing cycles, weekends, holidays, and issuer timing. That can waste fees, trigger network penalties, and lower approval rates with repeated low-value attempts.

They help keep credentials current when cards change and signal a more secure payment setup. That reduces avoidable failures and supports smoother recurring payment recovery.

Use silent recovery for soft declines when time is available. Use active dunning for hard declines or when payment must be captured immediately to deliver the service.

Share this article

Author

kyle.regacho

Author at SmartRetry, sharing insights on payment recovery, routing, and revenue protection.

Read all articles >More in General:

May 9, 2026

How to Avoid Payment Declines at the 2026 FIFA World Cup

This article explains how merchants can reduce cross-border declines during the World Cup through smarter routing, richer auth data, and recovery tactics that protect revenue and lift approval rates.

May 6, 2026

How AI Payment Orchestration Improves Authorization Rates and Decline Recovery

This article explains how AI-driven orchestration helps payment teams route transactions smarter, time retries better, and reduce involuntary churn to recover more revenue.