The Phantom Decline: Decoding the Gateway vs. Issuer Blame Game

It happens without warning: a sudden spike in failed transactions hits your dashboard. You investigate the logs, and the payment gateway points the finger at the issuing bank. Your customer service team reaches out to the affected buyers, who immediately call their banks. A few hours later, the verdict comes back. The bank representatives claim they never even saw the transaction attempts and insist everything is fine on their end.

You are now stuck in the most frustrating loop in the payments industry. The gateway blames the issuer, and the issuer says the gateway is hallucinating. Meanwhile, legitimate transactions drop, your approval rate tanks, and revenue evaporates. In 2023 alone, false declines were estimated to cost U.S. retailers $81 billion (Source).

When multiple cards are declined and both sides claim innocence, someone is usually wrong, but rarely is anyone intentionally lying. The disconnect stems from the immense complexity of payment architecture. A single transaction must traverse a labyrinth of risk engines, network switches, and banking ledgers in milliseconds. When a breakdown occurs in this chain, the resulting error codes are often mistranslated, truncated, or completely misunderstood by the frontline support teams tasked with explaining them.

To solve these phantom declines, you have to look past the generic dashboard messages and understand the specific mechanics of the payment gateway. By dissecting exactly how and where an authorization request can quietly die, revenue teams can stop pointing fingers and start recovering lost transactions.

The Anatomy of a Ghost Decline

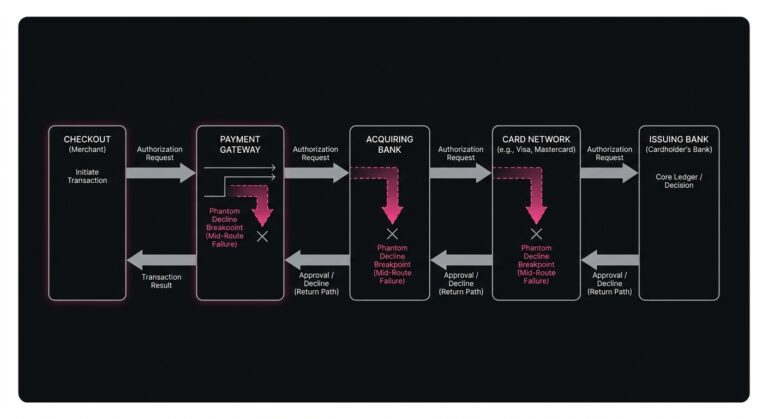

To understand how a transaction can simply vanish between two massive financial institutions, we first need to look at the journey of a standard payment authorization. When a customer clicks the buy button, the request travels from your checkout environment to your payment gateway. The gateway formats this request and hands it to the acquiring bank or processing partner. The acquirer routes it to the card network, such as Visa or Mastercard, which then forwards it to the issuing bank’s processing system. Eventually, the issuer checks the customer’s core banking ledger to verify available funds.

If all goes well, an approval message travels back through those exact same hops. When something goes wrong, a decline code gets passed back down the chain.

The core problem arises because decline codes are not universal, high-fidelity messages. They are archaic, two-digit codes inherited from the era of dial-up card terminals. When a failure occurs, every node in the chain attempts to map the error to something the next node will understand. By the time a complex network routing error or a localized fraud flag reaches your merchant dashboard, your gateway has likely simplified it into a generic Card Declined or Do Not Honor message.

When you see a payment declined across multiple different cards simultaneously, and the banks claim ignorance, the transaction almost certainly never reached the bank’s core ledger. It was killed somewhere in the middle of the journey.

Suspect One: The Gateway’s Silent Risk Engine

When investigating widespread checkout issues, the first place to look is your own payment gateway. Gateways today are not just dumb pipes passing data along. They are sophisticated gatekeepers equipped with aggressive internal risk and velocity engines.

Gateways monitor the flow of transactions for signs of card testing or distributed fraud attacks. If a gateway’s machine learning model detects an anomaly, it will intervene. This could be triggered by a slight variation in the billing address formatting, a mismatched device fingerprint, or simply too many transactions coming from a specific IP subnet.

When the gateway kills a transaction internally, the request never reaches the acquiring bank or the card network. However, to prevent bad actors from reverse-engineering the fraud rules, the gateway often masks this intervention. Instead of displaying a clear Blocked by Internal Fraud Rule message, it might log a generic issuer response code and effectively categorize it as a standard decline.

When your operations team contacts the gateway’s support desk, the frontline agent looks at the same masked dashboard you do. They see a generic decline code and confidently inform you that the issuing bank rejected the card. Yet when the customer calls their bank, the representative truthfully reports that no authorization attempt was ever made.

To bypass this blind spot, payment teams need to look at the raw API responses rather than the sanitized UI dashboard. If the raw payload lacks a network authorization code or a network transaction ID, the request never left your gateway.

Suspect Two: The 3D Secure Black Hole

Another major contributor to phantom payment failures is the authentication layer, specifically 3D Secure. In regions with Strong Customer Authentication (SCA) mandates, or for merchants opting into 3DS for liability shifts, transactions undergo a two-step process of authentication first and authorization second.

During the authentication phase, the merchant pings the issuer’s Access Control Server (ACS) to verify the cardholder’s identity. This might involve a push notification to the customer’s banking app or a one-time password sent via SMS.

If this authentication step times out, fails due to a browser popup blocker, or crashes because of a misconfigured routing table at the issuer’s ACS, the payment fails immediately.

Because authentication happens before authorization, no actual request for funds is ever drafted or sent through the traditional payment processing flow. When the customer calls their bank to ask why their purchase was declined, the teller checks the authorization ledger. Seeing zero declined authorizations, they naturally assume the merchant’s website is broken.

When dealing with a sudden cluster of unexplained declines, separating your authentication logs from your authorization logs is a critical diagnostic step. If transactions are dropping before an authorization attempt is even minted, 3DS drop-offs or ACS routing failures are likely the culprits.

Suspect Three: The Network and Acquirer Limbo

Sometimes, the transaction safely leaves your gateway, successfully clears authentication, and hits the acquiring bank, only to vanish into the ether before reaching the issuer. The card networks themselves act as massive, silent filters.

Visa and Mastercard operate global risk engines like Visa Advanced Authorization (VAA). These network-level tools evaluate transactions in real time and score them based on global threat telemetry. If a transaction scores too high for risk, the network kills the authorization request and sends a decline message straight back to the acquirer.

Networks also enforce strict rules regarding Merchant Category Codes (MCC) and cross-border processing. If your acquirer improperly formats a transaction, or if the network temporarily flags a specific Bank Identification Number (BIN) range due to an ongoing cyber event, the network returns a decline.

Because the network intercepted the request, the issuing bank is completely oblivious. The gateway receives a decline code from the network, maps it to a generic Declined by Issuer bucket, and the blame game begins anew.

Diagnosing network-level failures requires asking your gateway or acquirer for the System Trace Audit Number (STAN) and the Acquirer Reference Number (ARN). If the acquirer can provide a STAN but the issuer claims no record of the transaction, the failure occurred at the network switch.

Suspect Four: The Issuer’s Front Door vs. The Back Office

Perhaps the most fascinating and frustrating cause of the not-our-end phenomenon is the internal architecture of the issuing banks themselves. A bank today is not a single monolith. Instead, it operates as a fragile ecosystem of third-party processors, legacy mainframes, and edge APIs.

When an authorization request arrives at an issuing bank, it first hits the issuer processor. These massive technology vendors, such as TSYS, Fiserv, or Marqeta, manage the bank’s risk rules, card limits, and network connectivity. Only after the processor approves the transaction does it ping the bank’s core ledger to reserve the funds.

Issuer processors maintain incredibly strict fraud parameters. If a transaction looks suspicious, or if there is a momentary timeout between the processor and the core ledger, the processor will decline the transaction at the edge.

When a frustrated customer calls the 1-800 number on the back of their credit card, they connect to a retail support agent. This agent lacks access to the issuer processor’s highly technical edge logs and only sees the core banking ledger. Because the processor killed the transaction at the front door, the attempt never reached that core system.

The agent looks at the screen, sees no record of a decline, and assures the customer that their account is fine. They naturally conclude that the merchant must be experiencing checkout issues.

The issuer actually did decline it, but the left hand of the bank didn’t tell the right hand. This architectural quirk is responsible for millions of hours of wasted troubleshooting across the commerce ecosystem. It is the ultimate phantom decline, born entirely from internal banking silos.

Suspect Five: Stand-In Processing (STIP) Anomalies

There are also moments when the network attempts to reach the issuing bank, but the bank’s servers are down for maintenance or experiencing an outage. To keep global commerce flowing in these situations, card networks offer a service called Stand-In Processing (STIP).

During a STIP event, Visa or Mastercard will step in and approve or decline transactions on behalf of the unresponsive issuer. They rely on pre-agreed rules like daily spending limits to make these decisions. If the network declines a transaction during this window, it sends a decline code back to the merchant.

When the issuing bank’s servers eventually come back online, the network sends them a batch file detailing everything that happened while they were asleep. However, the retail banking support agents rarely look at STIP logs when a customer calls to complain about a failed purchase. They only look at the live ledger, see no record of the immediate decline, and once again pass the blame back to the merchant.

How to Break the Stalemate

When you are caught in the middle of this operational nightmare, the most ineffective strategy is continuing to rely on Tier 1 support desks. You cannot solve a complex payment optimization problem by acting as a messenger between a confused gateway rep and an equally confused bank teller. You have to take control of the data.

The first practical step to reduce these payment declines is to look for patterns in the BINs. When you notice a massive spike in failures, export the first six or eight digits of the affected cards.

If the failing cards belong to a wide variety of different issuing banks, such as Chase, Citi, Bank of America, and Capital One all failing simultaneously, the problem is absolutely not on the issuer side. It is statistically impossible for dozens of independent banks to coordinate a localized outage. In this scenario, the bottleneck is your gateway, your acquirer, or an MCC configuration issue at the network level.

Conversely, if every single failed transaction maps back to the exact same issuing bank, you know the gateway and the network are functioning properly. The issuer is either experiencing an unannounced outage, a STIP event, or their edge processor has updated a risk rule that negatively targets your specific merchant profile.

Armed with this BIN analysis, you can bypass front-line support entirely. When escalating a ticket to your payment provider, you no longer just report that transactions are failing. Instead, you specify that you are experiencing a total decline rate on a specific BIN across multiple unique customer profiles while all other BINs process normally. You can then request the network trace IDs for those specific payloads to verify the routing.

This approach changes the nature of the conversation by forcing payment providers to look at raw telemetry rather than generic dashboard readouts, which significantly accelerates resolution time.

The Role of Intelligent Retries in Revenue Recovery

While diagnosing the root cause of phantom declines is essential for long-term health, operations teams still face the immediate challenge of salvaging the revenue trapped in those failed attempts. This is especially critical for recurring billing models, where subscription payment issues can rapidly compound into involuntary customer churn.

When a transaction drops due to a transient network timeout, an ACS routing failure, or a temporary STIP event, treating it as a hard, permanent decline is a costly mistake. Many of these infrastructure blips resolve themselves within hours or even minutes. However, blindly hammering the gateway with immediate retry attempts is equally dangerous, as it can trigger velocity filters and flag your merchant account for aggressive card testing behavior.

This is where sophisticated payment recovery strategies come into play. Having a system to intelligently retry failed payments is critical for handling transient errors or false declines. Revenue losses from false declines have been projected to be 70x greater than fraud losses (Source). Platforms like SmartRetry focus on this exact layer of payment optimization. They analyze decline codes and timing rules to attempt transactions again when they have the highest probability of success. This approach helps merchants recover revenue and improve approval rates without triggering further fraud flags.

By applying intelligent logic to the recovery process, merchants can dynamically adjust their response based on the nature of the failure. If an analysis of the API payload suggests an issuer processor timeout, the system can automatically schedule a retry for off-peak processing hours. If the failure indicates a 3DS drop-off, the merchant can trigger an alternative localized payment method or route the transaction through a secondary acquirer with different routing tables.

Redefining Payment Optimization

The conflict between payment gateways and issuing banks is a natural byproduct of a highly fragmented financial infrastructure. Trillions of dollars flow through systems originally designed decades ago, heavily patched with advanced risk overlays, authentication mandates, and edge computing layers. Perfect visibility simply does not exist in this environment.

For revenue leaders, product managers, and payment operations teams, the key takeaway is that you cannot blindly trust the simplified error codes presented on a dashboard. An Issuer Decline is often a catch-all bucket for a dozen different systemic failures occurring anywhere between the checkout button and the bank’s core ledger.

When the blame game begins, the merchants who win are those who refuse to participate in it. Instead of waiting for a support ticket to slowly wind its way through multiple organizations, sophisticated teams dig into their own raw data. They map their authentication drop-offs, track performance at the BIN level, and understand the structural difference between an issuer processor and a core banking system.

By elevating your internal understanding of the payment processing flow, you transform transaction failures from a mysterious external problem into a manageable operational metric. You stop wasting time on futile phone calls and start implementing strategic routing rules, advanced authorization telemetry, and intelligent recovery systems. In an ecosystem where everyone points fingers, the organizations that take full ownership of their payment lifecycle are the ones that ultimately capture the revenue.