The Hidden Mechanics of Cross-Border Card Declines

You built a great product, and a customer finally found your website. After reading your pitch, they loaded their cart, entered their credit card details, and clicked the buy button. Then a wall appears out of nowhere. The screen flashes a generic error, and the transaction fails. A perfectly good buyer walks away empty-handed, leaving your marketing spend wasted. This is the frustrating reality of international commerce. You might assume the buyer just lacked the funds or made a typo, but a payment declined message on a global order is rarely that simple. Resolving these payment issues requires looking past the surface to understand what actually happens when a transaction attempts to cross a border.

If you look closely at your payment analytics, you will likely notice a distinct geographic divide. Domestically, you might enjoy a comfortable and frictionless environment where the vast majority of transactions sail through. The moment you look at your international cohorts, however, the numbers drop significantly. What feels like a seamless global economy to the consumer is actually a highly fragmented backend system of regional risk models, localized network rules, and mismatched data standards.

The Great Geographic Divide in Payment Performance

To understand why international payments fail, you have to look at the baseline metrics of the payments industry. A healthy domestic merchant might see a transaction approval rate hovering around 90% to 95%. When that same merchant processes a card issued in a different country, that rate frequently plummets into the 70s and occasionally much lower depending on the region.

This drop is not because international customers are inherently less creditworthy or more prone to fraud. It happens because the cross-border card payment flow gets exponentially more complicated the further the data travels.

Every card payment operates within a four-party model involving the merchant, the acquirer, the card network, and the issuing bank. In a domestic transaction, these players share a common regional context. They often operate under the same regulatory umbrellas, understand identical formatting standards, and have deep historical data on local purchasing behaviors.

When a transaction crosses an ocean, that shared context disappears. A request originating from an gateway in North America and traveling to an issuing bank in Europe has to jump through multiple network nodes while passing through differing fraud filters and localization standards. Every single hop introduces a new opportunity for a timeout, a misread field, or a panicked risk model.

Why Issuers Panic When Borders Are Crossed

The entity holding the ultimate power in any card transaction is the issuing bank. Their primary job is not to ensure your business makes a sale. Instead, their focus is protecting the account holder and limiting their own financial liability. Issuers rely heavily on automated risk models to approve or decline a payment authorization request in milliseconds.

These models are trained primarily on domestic behavior because the vast majority of an average consumer’s spending happens close to home. Cross-border card spending accounts for only about 6% of total card spending (Source). If a card that usually buys coffee in London suddenly tries to purchase software from a merchant category code associated with a business in California, the issuer’s fraud model notices the anomaly.

From the issuer’s perspective, the authorization request arrives stripped of the rich behavioral context you have on your website. You know the customer spent thirty minutes reading your documentation before buying, but the issuer only sees a foreign merchant, an unusual time zone, and an unfamiliar acquiring bank. Faced with a lack of context, risk models default to conservatism. This creates an asymmetry of risk. A false decline annoys the customer, who will likely blame your website rather than their bank. Approving a fraudulent charge, however, costs the bank real money and administrative headaches. Consequently, a perfectly legitimate card declined event becomes a routine byproduct of overzealous fraud protection.

The Data Degradation Problem

Beyond simple risk paranoia, many cross-border failures are the result of technical data degradation. A payment message is more than just a dollar amount and a card number. It actually contains dozens of data fields, including billing addresses, device identifiers, and security codes.

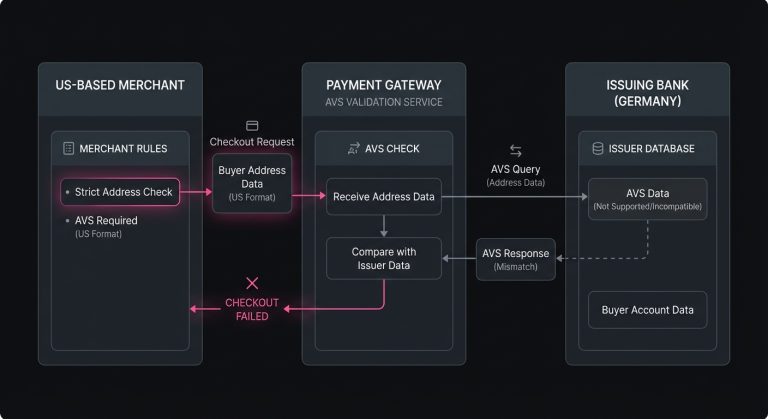

When these fields pass through different regional gateways, things frequently get lost in translation. Consider the Address Verification System, commonly known as AVS. In the United States, the UK, and Canada, this is a standard tool. Merchants routinely configure their gateways to decline transactions if the ZIP code or street address does not perfectly match the bank’s records.

AVS is virtually non-existent in many other parts of the world. If a US-based merchant strictly enforces an address check on a buyer from Germany, the transaction will likely fail. The resulting checkout issues occur not because the German buyer is a fraudster, but because the German issuing bank literally does not support the data field the merchant is demanding. The gateway sees a mismatch and hard-blocks the sale. By treating global data with local assumptions, merchants inadvertently construct invisible barriers to their own revenue.

The Nuance of Recurring International Billing

While a one-time checkout failure is frustrating, the complexity multiplies when you introduce recurring revenue models. Merchant-initiated transactions are notoriously difficult to manage across borders.

When a customer signs up for a subscription, the initial payment might require a security challenge, such as a one-time password sent to their phone, to help push the transaction through. On month two, that payment becomes a merchant-initiated transaction happening in the background.

Cross-border recurring billing suffers heavily from credential decay as cards naturally expire, get lost, or are reissued. In a domestic setting, merchants rely on network account updater services to automatically fetch the new card details. Unfortunately, international participation in these networks is inconsistent. A merchant in North America might find that their gateway simply cannot fetch updated card details for a customer in Asia.

When month three rolls around, the billing attempt hits a brick wall. These compounding payment failures lead directly to involuntary churn, silently draining the lifetime value of an otherwise loyal international customer base.

Demystifying the Issuer Response Codes

If you want to fix the problem, you need to look at the data coming back from the banks. When a transaction is rejected, the merchant receives an issuer response code. In a perfect world, these codes would tell you exactly what went wrong and how to fix it. In reality, they are notoriously vague and highly open to interpretation.

The classic example is Response Code 05, commonly labeled as Do Not Honor. It acts as the generic shrug of the global payments ecosystem. This code could mean the cardholder lacks funds, the transaction triggered a cross-border velocity limit, or the issuer’s authorization server was simply undergoing temporary maintenance.

Understanding these codes requires parsing them into actionable categories of hard declines and soft declines. A hard decline, such as a lost card or closed account, means the credential is dead. Trying to charge it again is a waste of time and risks penalizing your merchant account.

A soft decline is a temporary roadblock. Codes indicating insufficient funds, general processing errors, or generic risk flags fall into this category. Soft declines are where optimization efforts yield the highest returns, provided you know how to handle them gracefully. For more on the difference between hard and soft decline recovery, see Payment Declines: Recovery Tactics & Approval Gains.

Intelligent Recovery and the Art of the Retry

When a perfectly good international transaction fails due to a soft decline, your immediate operational instinct might be to simply try charging the card again. Blindly looping transactions is one of the quickest ways to damage your standing with card networks. It drives up processing costs, inflates decline ratios, and can eventually lead to your merchant account being flagged by network monitoring programs.

Effective retry logic relies on a highly nuanced approach to retrying logic. The context of the decline dictates the exact timing and method of the retry. If an international transaction fails due to insufficient funds, retrying it an hour later will achieve nothing. Waiting and retrying it on a common regional payday, such as the first or fifteenth of the month, changes the odds entirely. If a transaction fails due to a generic cross-border risk flag, retrying it when the foreign issuer’s batch processing is typically lighter might yield a different result. For a specialized guide on payment retries and timing, see our resource for operators.

This is the operational gap where platforms like SmartRetry become highly relevant. By focusing deeply on payment optimization and intelligently assessing when and how to attempt a retry, these systems help merchants recover revenue and improve transaction approval rates without running afoul of network rules. Instead of guessing, merchants rely on data models that understand the nuances of specific issuer behaviors across different regions. This ensures that every retry attempt has the maximum statistical probability of success.

To effectively retry failed payments and reduce payment declines, the strategy must shift from a brute-force approach to a surgical one. You are attempting to catch the issuer at a moment when their risk tolerance or technical availability is more favorable to the transaction. For more context on optimizing retry logic after issuer declines, read Issuer Decline Codes: Retry Logic & Auth Recovery.

Local Acquiring: The Structural Solution

While intelligent retries are an excellent way to handle failures, the best way to prevent them entirely is to restructure how the transaction is routed. The gold standard for international payment performance is multi-acquirer routing, often referred to as like-for-like processing.

If you have a large concentration of customers in Europe, passing those transactions through an acquirer based in North America ensures they will always be flagged as cross-border by European issuing banks. If you establish a European legal entity and process those payments through a regional acquirer, the transaction suddenly looks domestic. The merchant category code aligns, the data formatting matches local expectations, and the issuer’s risk models remain calm. Approval rates soar and can often jump by 10 to 20 percentage points overnight.

While local acquiring is highly effective, it requires significant operational overhead. A business has to manage foreign corporate entities, navigate local tax laws, integrate with multiple regional processors, and handle complex multi-currency reconciliation. For enterprise merchants with massive regional volume, the math easily justifies the effort. For mid-market companies, the overhead can be prohibitive, which makes routing optimization and intelligent recovery strategies much more vital. For more on how multi-acquirer setups can unlock higher approval rates in cross-border payments, check out our guide to multi-acquirer routing.

Navigating 3D Secure Without Killing Conversion

Another critical lever in cross-border optimization is the strategic use of 3D Secure. Historically, merchants viewed this authentication protocol as a conversion killer. It was seen as an obnoxious pop-up that forces customers to remember a password they have not used in years.

Today, the landscape is entirely different. With the introduction of the modern 3DS2 protocol, merchants and issuers can share rich background data like device telemetry and IP context. More importantly, it often facilitates a frictionless flow where the issuer authenticates the buyer without requiring any active input from the user.

In Europe, regulations like Strong Customer Authentication have made 3D Secure mandatory for many transactions. In other regions, it remains optional. When dealing with cross-border friction, intentionally triggering this authentication can act as a powerful trust signal to a paranoid foreign issuer. For an in-depth discussion, visit our resource on 3D Secure and auth rates.

By pushing a transaction through 3D Secure, the merchant shifts the liability for fraud away from themselves and onto the issuing bank. Because the issuer now has cryptographically verified proof that the buyer is legitimate, they feel significantly safer approving the cross-border request. Merchants can implement a dynamic ruleset where they only step up transactions that carry a high probability of a cross-border decline. This approach rescues risky payments while maintaining a smooth checkout for low-risk traffic.

Shifting from Reactive to Proactive Optimization

Treating payment infrastructure as a static utility is a common operational pitfall. The global financial ecosystem is not a fixed map but rather a living network. Bank Identification Number tables update constantly, issuers tweak their fraud models weekly, and regional data privacy laws dictate new gateway routing rules. What worked to clear a transaction in Brazil six months ago might trigger a hard block today.

Building resilience against cross-border friction requires a shift in perspective. Revenue optimization teams must monitor authorization rates not just at a high level, but sliced by country, bank identifier, issuer, and processor. If a specific issuing bank in the UK suddenly starts rejecting a large portion of your recurring billing traffic, your systems need to catch that anomaly immediately rather than waiting for an end-of-quarter churn analysis.

Authorization optimization is fundamentally about recognizing patterns in chaos. It involves testing different data payloads, experimenting with routing paths, and respecting the operational constraints of banks on the other side of the world.

The inherent friction of global finance is not going to disappear. Moving money across borders will always involve a delicate balance of risk, regulation, and technology. A transaction failure, however, is rarely a definitive end to the story. By moving away from passive acceptance and embracing data-driven recovery and routing strategies, you shift the probabilistic nature of payments in your favor. The businesses that scale globally are not just the ones with the most compelling products. They are the organizations that possess the operational clarity to ensure they actually get paid.

Want to dig deeper into the technical and strategic levers controlling cross-border payment performance? Head to our in-depth guide on cross-border payments for actionable recovery strategies specific to international payment flows.

The reason international approval rates plummet is the inherent complexity in payment authorization for global transactions, driven by multiple regional systems, issuer models, and risk logic.

One of the strongest tools available for merchants facing suspicious international declines is 3D Secure, which often increases issuer trust and pushes more cross-border transactions through with higher approval rates.

To avoid risking merchant standing, it’s vital to adopt a smarter approach to repeated card attempts—see best practices for payment retries which avoid network penalties and maximize cross-border recovery.

When codes like response code 05 (“Do Not Honor”) appear during international attempted charges, they rarely spell out what’s truly wrong. Learn what Do Not Honor means, and which recovery tactics actually work in these confusing situations.

This careful handling also extends beyond single declines. For a comprehensive breakdown of card decline recovery strategies for operators—including international contexts—check out this guide.

For specifics on which declines can (and can’t) be recovered, separate hard and soft declines with tactical recovery designed for global payment teams.

As you scale internationally, routing matters too. Explore how multi-acquirer routing boosts cross-border authorization rates and can meaningfully increase approvals overnight.

Not sure what a specific decline code means? Use our payment decline codes lookup tool for fast, clear answers.

Unfamiliar with bank tables and identifiers critical to regional routing? Cross-check any card using our BIN Lookup Tool or Card Issuer Lookup for geographic and risk context.

Finally, for company-specific acceptance quirks, don’t forget strict network logic enforced by Visa, Mastercard, and American Express—each has distinct requirements worth understanding for smoother international billing.