Navigating the Squeeze: Managing Chargeback Ratios and Acquirer Thresholds

The email usually arrives quietly, sitting in your inbox alongside routine operational alerts. Yet its contents are enough to command the immediate attention of your entire payments team. Your acquirer is writing to inform you that your chargeback ratio is trending dangerously close to the network threshold. The warning is polite but strictly procedural, leaving you a limited window to correct the trajectory. If the ratio continues to climb, the consequences shift from simple alerts to financial penalties. Scaling a business is hard enough without the sudden threat of merchant account restrictions.

For payment professionals, growth leaders, and revenue operations teams, managing chargebacks is an intricate balancing act. It requires maintaining a frictionless customer experience while simultaneously guarding against fraud, friendly fire, and systemic processing errors. When a business experiences increased chargeback ratios, the issue rarely points to a single point of failure. Instead, it usually reveals a complex interplay between customer behavior, billing clarity, authorization mechanics, and post-transaction communication.

Understanding how to keep these ratios under acquirer thresholds requires moving beyond basic fraud filters. It demands a holistic look at the entire payment lifecycle, from the moment an initial payment authorization occurs to the weeks following delivery or service fulfillment.

The Mechanics of the Acquirer Threshold

To manage the problem, you first have to understand how the networks measure it. Major card networks like Visa and Mastercard operate massive ecosystems built on trust. When consumers lose faith in their cards, the networks lose their core value proposition. To maintain this trust, they hold acquiring banks responsible for the merchants they underwrite.

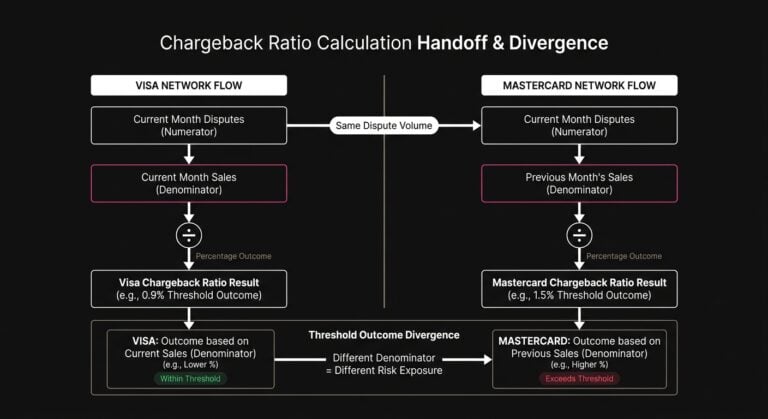

Acquirers then pass this accountability down to you. The primary metric used to measure merchant health is the chargeback ratio. Generally, this is calculated by taking the total number of chargebacks in a given month and dividing it by the total number of transactions processed. While the math seems straightforward, the nuances are often frustrating.

Visa’s Dispute Monitoring Program and Mastercard’s Excessive Chargeback Program establish clear guardrails. Typically, an early warning is triggered when a merchant hits a 0.65% ratio, with the standard threshold sitting at 0.9% to 1.0%, alongside a minimum volume of disputes, which is usually 100. Mastercard also has a monitoring program that fines businesses with a chargeback rate of 1.5% or higher (Source). However, the way the denominator is calculated varies. Visa typically divides current month disputes by current month sales, whereas Mastercard historically divides current month disputes by the previous month’s sales.

This difference matters. If your business experiences a sudden drop in sales volume, perhaps from a seasonal dip or a paused marketing campaign, your denominator shrinks. Consequently, the chargebacks trickling in from last month’s higher sales volume will cause your current month’s ratio to artificially spike. You can breach a threshold without a single increase in actual dispute volume simply because your transaction volume fluctuated.

Deconstructing the Triggers

When your ratio begins to climb, the immediate instinct is to blame fraudsters. While true criminal fraud involving purchases made with stolen financial data is a persistent threat, it is often not the primary driver of a spiking chargeback ratio. Instead, the industry is heavily influenced by first-party misuse, commonly known as friendly fraud.

Friendly fraud occurs when a legitimate customer makes a purchase and receives the good or service, but subsequently disputes the charge with their issuing bank. The psychology behind this behavior varies. Sometimes it is malicious and effectively amounts to digital shoplifting, but more often it stems from confusion or convenience.

Consumers have learned that calling their bank is often faster than dealing with a merchant’s customer service labyrinth. If they experience frustrating checkout issues, face a convoluted return policy, or simply fail to recognize the billing descriptor on their bank statement, the bank becomes their primary recourse.

For businesses operating recurring billing models, subscription payment issues are a massive catalyst for disputes. Customers who forget they signed up for a service or find the cancellation process too difficult will frequently bypass the merchant entirely. They call their issuer to claim the charge is unauthorized and secure a refund. This leaves the merchant with a lost customer, lost revenue, and a penalized ratio.

The Impact of Processor Communication

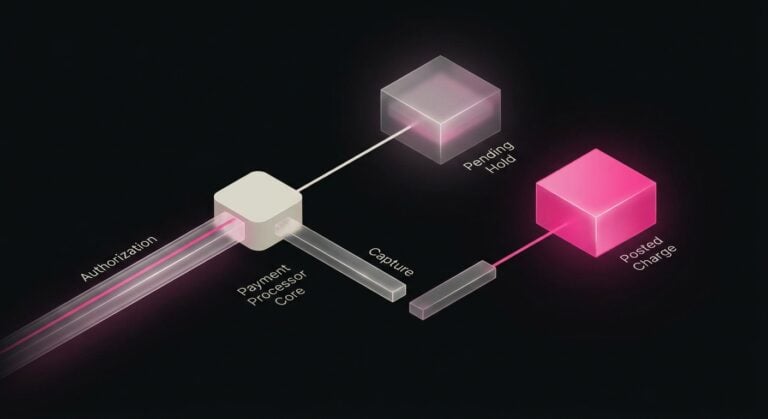

Another frequent, yet overlooked, trigger involves how a business communicates with the payment processor during the transaction flow. Inconsistent capture timing, where a transaction is authorized but not captured for several days, can lead to consumer confusion. The customer sees a pending hold, assumes it cleared, and then sees the actual charge post days later, mistakenly believing they were double-billed.

The Hidden Financial Shockwave

The direct cost of a chargeback is painful. The merchant loses the cost of goods sold, shipping expenses, transaction fees, and the original revenue. On top of that, acquirers levy a non-refundable chargeback fee that typically ranges from $15 to $25 per dispute just to process the paperwork. Stripe, for example, charges a $15 fee for each chargeback (Source).

The hidden costs associated with breaching acquirer thresholds, however, are far more dangerous to a growing business. When you cross the 1% threshold, you enter a probationary period where acquirers view you as an elevated risk. To mitigate their own exposure, they may implement a rolling reserve. This means the processor will hold back a percentage of your daily sales, often 5% to 10%, for up to 180 days. For cash-flow-sensitive businesses, having a significant portion of operating capital locked away can stall growth or jeopardize payroll.

If the ratio remains uncorrected, the situation escalates. The processor may increase your per-transaction processing rates, effectively taxing every future sale. In the worst-case scenario, the acquirer will simply terminate your merchant identification number. Losing your ability to process payments is an existential threat. Furthermore, terminated merchants can be placed on the Member Alert to Control High-Risk Merchants list, effectively blacklisting the business from securing processing with other reputable acquiring banks for years.

The Denominator Effect: Why Authorization Rates Matter

Because the chargeback ratio is a fraction, merchants often focus entirely on the numerator by trying to reduce the raw number of disputes. However, defending the denominator is just as critical.

Your total transaction count acts as a buffer. The higher your transaction volume, the more disputes you can absorb without breaching the percentage threshold. This is why a declining transaction approval rate is a silent killer for chargeback ratios.

If your payment systems are poorly routed or if you rely on aggressive fraud filters that flag legitimate customers, you will experience a high volume of payment failures. Every time a transaction is blocked or a card is declined unnecessarily, you lose a successful transaction that would have otherwise padded your denominator.

To protect the ratio, merchants must actively work to reduce payment declines and ensure their processing logic is highly optimized. By maintaining high approval rates on legitimate traffic, businesses create the mathematical breathing room necessary to absorb the inevitable background noise of standard disputes.

The Interplay Between Declines, Retries, and Chargebacks

It may seem counterintuitive, but the way a merchant handles a declined payment event directly influences future chargeback volume. When a transaction fails, the logic determining what happens next is critical.

Consider a scenario where a customer attempts to purchase a high-ticket item, but their bank declines the transaction due to a temporary risk hold. The confused customer frantically clicks the submit payment button three more times, resulting in three consecutive decline messages before they finally give up.

From the issuing bank’s perspective, those initial clicks may have generated pending authorization holds that reserve funds on the customer’s account despite the final capture being declined. When the customer checks their mobile banking app an hour later, they see four separate pending charges for the same item. Panic sets in, and they immediately call their bank to report fraudulent double-billing. Even if those holds were destined to drop off naturally within a couple of days, the customer’s premature dispute has just hit your merchant account.

This highlights the absolute necessity of intelligent retry logic. Blindly hammering the payment gateway after a failure not only incurs gateway fees but creates massive consumer confusion. Merchants must interpret the specific issuer response to determine if a retry is safe, warranted, or likely to cause a subsequent dispute.

This is where specialized payment optimization comes into play. Platforms like SmartRetry act as a layer of intelligence in these scenarios by focusing on the careful resubmission of declined transactions. By analyzing decline codes and timing retries logically instead of aggressively, such systems help merchants recover revenue and improve approval rates without triggering the erratic billing patterns that provoke consumer panic and friendly fraud.

Evidence, Representment, and the Burden of Proof

When disputes do occur, merchants have the right to fight back through a process called representment. This involves submitting compelling evidence to the issuing bank to prove the original transaction was legitimate and the cardholder received the value they purchased.

Successfully navigating representment requires meticulous record-keeping. The issuing bank is not a neutral arbiter since their primary customer is the cardholder. As a result, the merchant’s evidence must be overwhelming to successfully overturn a dispute.

Standard evidence packages include address verification service matches, card verification value checks, IP addresses, device fingerprinting, and clear communication records. For physical goods, tracking numbers showing delivery to the billing address are paramount. For digital goods or software, server logs showing the customer logging in and utilizing the service are highly effective.

Leveraging Compelling Evidence Rules

The networks continuously update their rules to help merchants fight friendly fraud. For example, Visa’s Compelling Evidence 3.0 framework allows merchants to use historical data to their advantage. If a merchant can prove that the same cardholder made at least two previous, undisputed purchases using the same device, IP address, or login credentials, liability can often be shifted back to the issuer.

Fighting chargebacks is highly resource-intensive. Operations teams must evaluate the cost-benefit analysis of representment, as spending two hours of an analyst’s time to fight a $15 chargeback is poor economics. Sophisticated teams build automated rulesets to auto-accept low-value disputes while aggressively fighting high-value claims and repeat offenders.

Strategic Prevention Tactics: Fixing the Leak

While representment is necessary for payment recovery, it is an inherently reactive process. The most effective way to manage acquirer thresholds is to prevent the dispute from ever being initiated. This requires auditing the entire payment processing flow through the eyes of the consumer.

The most basic yet frequently failed prevention tactic is a clear billing descriptor. The text appearing on a customer’s credit card statement must be instantly recognizable. If a parent company name, an obscure holding company, or a bizarre abbreviation appears, the customer will likely fail to recognize the charge. Including a customer service phone number directly in the billing descriptor gives the confused cardholder a way to contact you before they call their bank.

Communication during the fulfillment cycle also heavily impacts dispute rates. With next-day delivery setting the standard, consumer patience is practically non-existent. If an item is delayed, over-communicate. A customer who knows their item is backordered but receives a polite update is far less likely to initiate a dispute than one who feels completely ghosted.

For software and subscription models, the mandate is simple. You must make cancellation incredibly easy. Hiding the cancellation button behind a phone call or a multi-step retention maze guarantees an increase in friendly fraud. A self-serve cancellation portal might marginally increase churn in the short term, but it actively protects your merchant account and preserves your ability to process payments in the long run.

Furthermore, leveraging network tools like Verifi and Ethoca can serve as an early warning system. These tools are often referred to as chargeback alerts or rapid dispute resolution systems, and they notify merchants the moment a cardholder initiates a dispute with their bank. The merchant is then given a brief window, usually 24 to 72 hours, to proactively refund the transaction. While you still lose the revenue, a refunded transaction does not count toward your chargeback ratio, which effectively shields your acquirer thresholds.

Shifting from Reactive to Strategic

Treating chargebacks simply as a cost of doing business is a luxury scaling merchants can no longer afford. As transaction volumes grow, the mathematical realities of acquirer thresholds become unforgiving. Waiting until you receive a warning letter from your processor puts your operations in a highly defensive and deeply compromised position.

Managing these thresholds requires recognizing that a dispute is rarely an isolated event. It is usually the final and loudest symptom of friction somewhere earlier in the customer journey. The root cause might be a confusing checkout experience, an overly aggressive retry strategy on failed payments, or a simple lack of clarity in a recurring billing cycle.

By prioritizing high authorization rates, employing intelligent logic when handling declines, providing clear communication, and leveraging network prevention tools, businesses can stabilize their ratios. The goal is not merely to placate an acquiring bank, but to build a resilient payment infrastructure that protects revenue and fosters genuine consumer trust. When the payment flow is highly optimized, the threat of the network threshold fades, allowing the organization to return its focus to sustainable growth.