Fraud in the payments industry has a very loud siren, and it usually sounds like a chargeback. When a chargeback hits, it demands immediate attention. Dashboards flash red, risk teams scramble to investigate the root cause, and financial penalties loom in the background. But this intense focus on the most visible threat often creates a dangerous blind spot. While operations teams are busy fighting these loud payment issues, a much larger volume of legitimate revenue slips quietly out the back door. The truth is that chargebacks are just one piece of a much larger and more complex fraud puzzle. If you only look at the transactions that slip through the cracks and result in a dispute, you are missing the massive ecosystem of payment failures that happen before a transaction ever settles.

To truly master payment optimization, professionals need to zoom out. The ecosystem is a delicate balancing act between keeping bad actors out and letting good customers in. When merchants focus too heavily on preventing chargebacks, they inevitably introduce friction elsewhere, often at the expense of their own growth. Understanding the broader context of authorizations, payment declines, and recovery strategies is the only way to build a resilient payment infrastructure.

The Loudest Siren in the Room: Why We Fixate on Chargebacks

It is entirely understandable why merchants obsess over chargebacks. They are measurable, penalizing, and carry an administrative burden that directly impacts the bottom line. Unlike a simple transaction declined at checkout, a chargeback initiates a tedious, multi-party process that drains operational resources.

A chargeback occurs when a cardholder disputes a transaction with their issuing bank. The triggers for these disputes generally fall into three distinct categories. First is true fraud, which involves stolen credit card details. Second is friendly fraud or first-party misuse, where the cardholder makes a purchase but later denies it or claims the item never arrived. Finally, there is merchant error, such as duplicate billing or confusing billing descriptors.

The financial impact extends far beyond the lost cost of goods sold. Merchants lose the original transaction amount, pay a non-refundable chargeback fee to their acquirer, and lose the marketing acquisition cost spent to bring that customer to the site in the first place. Worse, if a merchant’s chargeback ratio climbs too high, typically crossing the 0.9% to 1% threshold, they risk being placed into monitoring programs by major card networks. This can lead to escalating fines or even the loss of processing privileges.

Because the stakes are so high, businesses pour immense resources into evidence preparation and representment. Risk teams compile delivery confirmations, IP address logs, session histories, and customer communications to prove a transaction was legitimate. This manual process is expensive and time-consuming. Merchants win an average of 45% of the chargebacks they represent, and register a net recovery rate of 18% (Source). Consequently, the natural reflex for many businesses is to tighten their risk rules and turn up the dials on their fraud prevention tools to block anything that looks remotely suspicious.

This is exactly where the puzzle starts to warp.

The Invisible Iceberg: When Fraud Prevention Goes Too Far

When a merchant prioritizes a zero-chargeback environment above all else, they inevitably create a new, often more expensive problem: false declines. A false decline, or false positive, happens when a legitimate customer attempts to make a purchase, but the transaction is blocked by either the merchant’s overly aggressive fraud filters or the issuing bank’s risk models.

If chargebacks are the visible tip of the iceberg, false declines are the massive, submerged block of ice that tears the hull out of merchant profitability. Industry data consistently suggests that the revenue lost to falsely declined good customers dwarfs the revenue lost to actual fraud.

The damage of a false decline compounds over time. When a good customer encounters checkout issues and sees their card declined despite having sufficient funds, the resulting frustration often damages the brand relationship permanently. A significant percentage of consumers who experience a false decline will abandon the merchant entirely and purchase from a competitor. You are not just losing the value of that single shopping cart. You are destroying the lifetime value, or LTV, of that customer.

This dynamic illustrates the core tension in payment optimization. The risk team is incentivized to keep fraud low, while the growth team is incentivized to push transaction approval rates as high as possible. Treating chargebacks as the sole metric of success empowers the risk team to over-block, effectively solving a fraud problem by creating a revenue problem.

Bridging the Gap Between Risk and Revenue

To solve this, organizations must shift their perspective. Fraud prevention cannot exist in a vacuum separate from revenue generation. The goal should never be to eliminate fraud entirely, because the only way to achieve zero fraud is to process zero payments. Instead, the goal is to find the optimal threshold where the cost of fraud is balanced against the cost of lost sales.

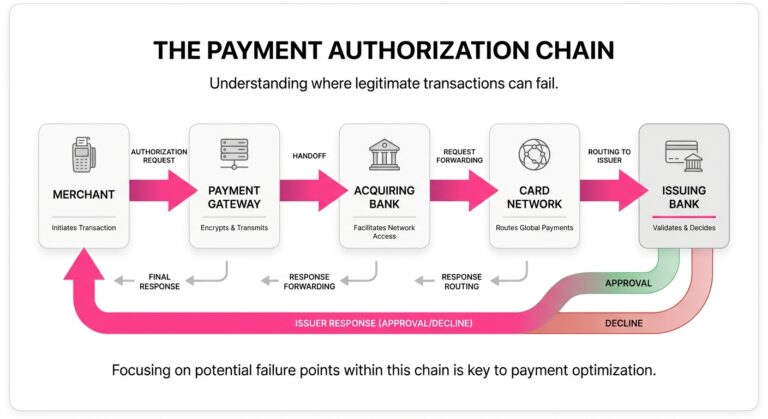

Deconstructing the Payment Processing Flow

To understand why legitimate payments fail, we have to look closely at the mechanics of payment authorization. When a customer clicks buy, a complex, split-second conversation happens between the merchant, the payment gateway, the acquiring bank, the card network, and the issuing bank.

The issuer response is the ultimate deciding factor in this flow. Issuers use their own proprietary, highly secretive risk models to determine whether to approve or decline a request. They look at velocity, location, transaction size, mismatching CVV or Address Verification System data, and the merchant’s historical risk profile.

Because issuers are on the hook for protecting their cardholders, they err on the side of caution. If a merchant sends authorization requests with messy, incomplete, or poorly formatted data, the issuer is more likely to decline the transaction. Furthermore, issuers rarely provide clear, actionable feedback. Instead of a detailed explanation, merchants receive vague decline codes like Do Not Honor or Generic Decline.

These generic codes often masquerade as fraud prevention when, in reality, they might be the result of a network timeout, a temporary hold on the cardholder’s account, or a rigid, outdated rule in the issuer’s legacy system. If a merchant simply assumes that every decline is a successful block of a fraudulent attempt, they leave a massive amount of recoverable revenue on the table.

The Role of 3D Secure in Authorization

One of the ways merchants attempt to balance authorization rates with fraud prevention is through Strong Customer Authentication. By shifting the liability of fraud back to the issuer, this protocol protects the merchant from chargebacks. However, introducing it can also add friction into the checkout flow and potentially cause cart abandonment. Modern implementations like 3DS 2.0 utilize rich data sharing to perform frictionless authentication in the background. This minimizes the impact on the user experience while still securing the transaction. Understanding when to dynamically route transactions through 3DS is a critical component of looking beyond the basic chargeback metric.

Recurring Revenue and Subscription Payment Issues

The complexity of the fraud and payment puzzle multiplies when applied to subscription and recurring billing models. In a traditional e-commerce checkout, the customer is present to authenticate the transaction, enter a new card, or fix a typo. In a subscription model, the initial transaction might go through flawlessly, but subsequent billing cycles happen asynchronously.

Subscription businesses face a unique set of billing challenges. Over time, credit cards expire, get lost, or are replaced due to data breaches elsewhere. When it is time for the monthly or annual renewal, the merchant attempts to charge a card that is no longer valid. This results in an involuntary churn event. The customer didn’t want to cancel their service. The payment infrastructure simply failed to collect the funds.

Treating these subscription payment issues as a fraud problem is a misdiagnosis. A transaction declined on a recurring billing cycle for Insufficient Funds or Expired Card requires an entirely different operational response than a high-risk order placed with a stolen card at 3:00 AM.

To combat involuntary churn, merchants deploy sophisticated dunning management and account updater services. Network tokenization is becoming a vital tool for ensuring continuity in recurring billing. This process replaces the primary account number with a secure token that updates automatically when a card is reissued. Yet, even with these tools in place, a percentage of transactions will still fail due to temporary network outages or soft declines.

The Strategy of the Second Chance: Intelligent Retries

This brings us to one of the most critical, yet frequently misunderstood, pieces of the payment puzzle: how to handle a declined transaction.

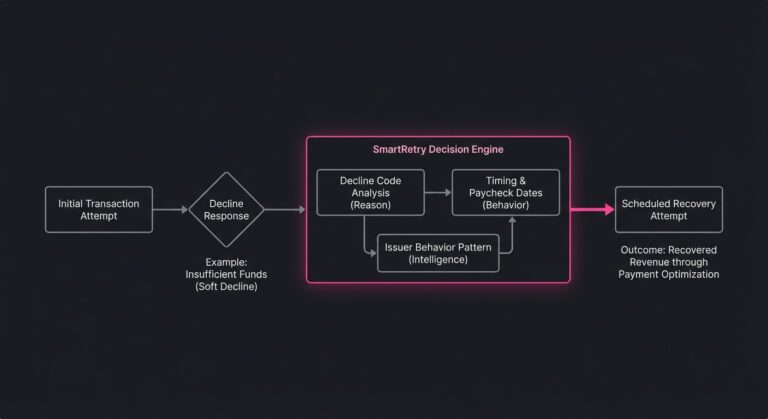

When a transaction is declined, the immediate question should be: Is this a hard decline or a soft decline? A hard decline occurs for reasons that are permanent and unresolvable, such as a stolen card, a closed account, or invalid card details. Retrying a hard decline is not only futile, but it can also damage a merchant’s reputation with card networks and result in processing penalties.

A soft decline, on the other hand, is temporary. It might occur because the cardholder briefly exceeded their credit limit, the issuing bank’s server experienced a momentary timeout, or a velocity check was triggered by legitimate but rapid purchasing behavior. Soft declines represent a massive opportunity to retry failed payments and recover lost revenue.

However, a brute-force approach to retrying payments, such as pinging the issuer repeatedly at random intervals, is a poor strategy. It increases processing costs, annoys issuers, and yields diminishing returns. Optimization requires a surgical approach to the retry schedule.

Timing is Everything in Payment Recovery

The success of a retry depends heavily on timing, the specific decline code, the day of the month, and the underlying issuer’s historical behavior. For example, retrying an Insufficient Funds decline on the 1st or 15th of the month, when many consumers receive their paychecks, often yields higher success rates than retrying on the 23rd.

This is where a nuanced approach to recovery becomes essential. Platforms like SmartRetry approach this specific challenge by focusing on payment optimization and the intelligent retrying of soft declines. This helps merchants recover legitimate revenue while improving overall transaction approval rates without manually overriding core risk controls. By utilizing data science to determine the optimal moment to re-attempt a transaction, businesses can rescue revenue that would otherwise be categorized as a permanent loss. This transforms a point of friction into a silent success.

Shifting the Paradigm: From Fraud Defense to Payment Optimization

To fully grasp why chargebacks are just one piece of the puzzle, organizations must transition from a defensive mindset to an optimization mindset. Fraud defense asks: “How do we stop bad transactions?” Payment optimization asks: “How do we confidently approve the maximum number of good transactions while keeping risk within an acceptable margin?”

This paradigm shift requires breaking down the silos between different departments. Payment product managers, risk analysts, and growth marketers must work from the same set of data.

Granular Data as the Great Unifier

When you view payments holistically, data becomes your primary tool for navigating the trade-offs. Merchants should be tracking their authorization rates just as closely as their chargeback ratios. If a new fraud rule is deployed and the chargeback rate drops by 0.1%, but the overall authorization rate plummets by 3%, that rule is likely costing the business more money than it saves.

Merchants must also analyze their decline codes by issuer and by Bank Identification Number. You might discover that a specific issuing bank is disproportionately declining your transactions due to the way your gateway formats the billing descriptor. Fixing that formatting issue is a payment optimization win that has absolutely nothing to do with fighting fraud, yet directly increases revenue.

The Role of Machine Learning

Payment optimization increasingly relies on machine learning models that can analyze hundreds of data points in milliseconds. Unlike rigid, rules-based systems that automatically decline transactions over a certain amount or distance, machine learning evaluates the context of the transaction. It can recognize that while a purchase looks anomalous based on location, the behavioral biometrics and device fingerprint match the user’s historical profile. This suggests a legitimate customer traveling abroad rather than a fraudster.

By feeding these models outcome data, including successful retries and post-transaction dispute records, the system learns the subtle differences between a risky transaction and a merely unusual one.

Seeing the Entire Board

Treating chargebacks as the ultimate measure of payment health is like driving a car while only looking in the rearview mirror. It tells you what went wrong in the past, but it doesn’t help you navigate the obstacles currently in front of you.

Navigating payments effectively requires a wider lens. It takes an understanding that every rule designed to block a bad actor has a corresponding impact on a good customer. Businesses must acknowledge the probabilistic nature of issuer decisions, the complexities of subscription billing continuity, and the immense value of intelligent recovery strategies for temporary failures.

By stepping back to view the entire payment processing flow, from the initial click at checkout, through the silent calculations of the authorization request, to the strategic handling of subsequent declines, organizations can unlock new tiers of growth. True payment mastery is not about building the thickest walls to keep fraud out. It is about engineering the smartest, most dynamic gates that let legitimate revenue flow in without interruption.