Building a reliable checkout experience often feels like wrestling with a ghost. You construct the perfect payload, send a cleanly formatted request into the processing ether, and anticipate a logical, structured response. Instead, you receive a cryptic puzzle. Payment failures are rarely straightforward, and they rarely offer the clean resolution engineering teams hope for. When a payment authorization is rejected, the resulting data is supposed to explain exactly what went wrong. In reality, that data is often a tangled, contradictory mess. Issuers rely on decades-old infrastructure, risk models shrouded in secrecy, and a completely fragmented interpretation of industry standards. For the developers and product teams tasked with turning these responses into smooth user experiences, this ambiguity is a daily frustrating reality.

The core of the problem lies in the disconnect between what digital merchants need and what traditional financial infrastructure was built to provide. Modern software development thrives on predictability. If an API call fails, a developer expects an HTTP status code that clearly categorizes the failure, allowing them to route the user to an appropriate error state or trigger an automated retry. Payment systems, however, operate on a completely different paradigm. Understanding why these decline codes are so inconsistent and learning how to design resilient systems around them is one of the most complex challenges in payment optimization.

The Illusion of a Shared Language

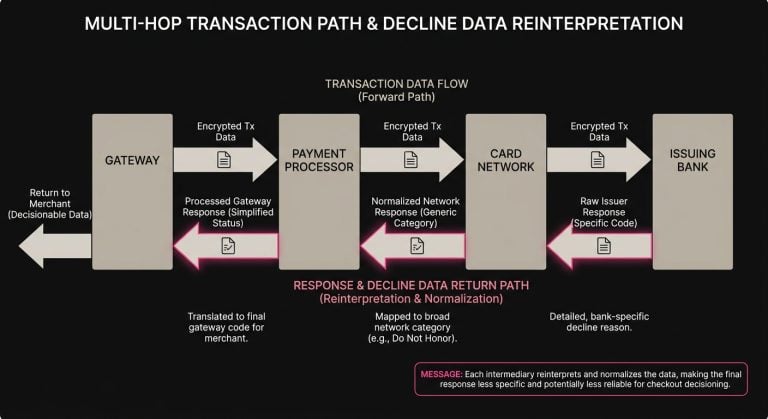

To understand the chaos of issuer responses, you have to look at the journey of a transaction. When a customer clicks the buy button, the transaction data does not travel directly from your server to the customer’s bank. It hops from your gateway to a payment processor, passes through the card network, and finally reaches the issuing bank. At every single hop in this payment processing flow, the data is translated, repackaged, and interpreted.

The industry technically operates on standardized messaging frameworks, most notably ISO 8583. In theory, this standard provides a universal dictionary of response codes. Code 04 means Pick up card, Code 51 means Insufficient funds, and Code 54 means Expired card. If every financial institution on earth adhered strictly to these definitions, developers could simply map these responses to specific UI elements and retry loops, and the problem would be solved.

The reality is that ISO 8583 is treated less like strict legislation and more like mild guidance. An issuer in London might use a specific code to indicate a hard block due to suspected fraud, while a regional credit union in the American Midwest might use that exact same code to indicate that their internal authorization server timed out. When the decline message travels back down the chain to the merchant, processors often attempt to normalize these varied responses into their own unified API formats. By the time the webhook hits your server, the original context of the decline has been filtered through multiple translation layers, leaving you with a generic rejection that obscures the true cause of the failure.

Decoding the Catch-All Responses

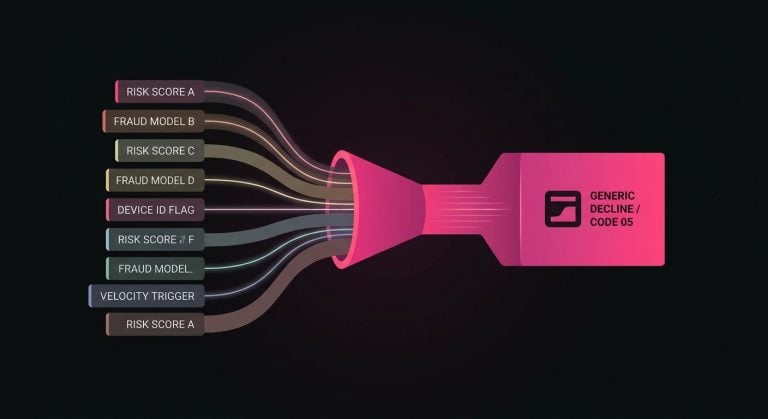

No conversation about inconsistent issuer responses is complete without mentioning the infamous Code 05: Do Not Honor. For developers new to payments, encountering this code for the first time is deeply confusing. It sounds authoritative but conveys absolutely zero actionable information. It simply means the issuer decided not to approve the transaction and declined to elaborate on the reason.

Issuers lean heavily on generic codes for a highly rational reason, which is risk management. An issuing bank’s primary responsibility is protecting their cardholder’s funds and managing their own credit exposure. If their machine learning models detect a potentially anomalous transaction, they will block it. However, they do not want to broadcast the exact parameters of their fraud models to the outside world. Providing a highly specific decline reason could theoretically give bad actors the information they need to adjust their tactics and bypass security filters. Consequently, a transaction declined due to an unusual location, an IP mismatch, or a suddenly high velocity of purchases will often be masked behind a vague Do Not Honor or Generic Decline response.

This intentional obfuscation protects the bank, but it severely damages the merchant’s transaction approval rate. Visa reports that the global average approval rate for card-not-present transactions is 85% (Source). It leaves payment operations teams staring at dashboards full of identical failure codes, wondering how many of those customers actually lacked the funds, how many simply triggered a paranoid fraud filter, and how many were legitimate buyers caught in a temporary network glitch.

The Shifting Meaning of Specific Codes

Even when issuers use seemingly specific codes, the definitions tend to drift. Take Code 51, traditionally reserved for Insufficient Funds. On the surface, this is a clear, actionable hard decline. However, observed data across massive transaction volumes reveals that some issuers return Code 51 when a customer hits a daily spending limit, even if their account balance is perfectly healthy. Others might return an Expired Card code for a card that is demonstrably valid. This happens when a new card has been issued to the customer and activated, rendering the previous credential obsolete in the bank’s internal systems, regardless of whether the expiration date on the plastic has actually passed.

When the ground truth of a decline code shifts based on the specific issuing bank, the time of day, or the merchant category code, building static logic around these responses becomes a highly fragile endeavor.

The Engineering Challenge of Categorization

For the developers tasked with building the checkout architecture, this inconsistency creates an architectural dilemma. Software engineers naturally gravitate toward building robust state machines. Their first instinct is often to create a comprehensive mapping matrix. They want to enumerate every possible decline code and match it with a specific system action and user message.

When teams first attempt to solve this, they usually divide the world into two clean buckets. The first is hard declines, which represent permanent failures like lost cards, stolen cards, or closed accounts. Logic dictates that these should never be retried, and the user should be immediately prompted for a new payment method. The second bucket is soft declines, representing temporary states such as insufficient funds, network timeouts, or general system errors. Standard logic suggests these can be safely retried later.

The problem arises when the data refuses to stay in its assigned bucket. If an issuer returns a vague code that historically acts like a soft decline but is suddenly used to indicate a permanently closed account, your system’s response will be wrong. Engineering teams that hardcode retry logic based on literal interpretations of API responses inevitably create problematic edge cases. The system will either needlessly abandon recoverable revenue or aggressively retry transactions that have zero mathematical chance of succeeding.

Maintaining these mappings requires constant manual intervention. As card networks update their rules and issuing banks silently migrate to new risk platforms, the underlying behavior of decline codes shifts. A logic tree that worked perfectly in the first quarter might start throwing unexpected errors months later, forcing developers to constantly patch and update their routing logic instead of focusing on core product features.

Crafting the Right Message for the Customer

The downstream effect of technical ambiguity is friction in the user experience. A customer clicking the submit button at checkout is in a state of high intent. If the payment fails, the immediate goal of the interface is to salvage the transaction without alienating the buyer. But how do you explain an error to a user when your own backend doesn’t fully understand it?

If a developer directly maps an issuer’s decline code to a user-facing error message, the results can be disastrous. Imagine a scenario where a customer with a high account balance attempts to buy an expensive item, but the issuer blocks it due to an aggressive risk filter while returning a vague Insufficient Funds code. If your interface explicitly says, “Your payment was declined due to insufficient funds,” you are not just providing unhelpful information. You are actively insulting the customer. The buyer knows they have the money. They will likely assume your website is broken and abandon the cart out of frustration.

Checkout issues require a delicate touch. The most effective user messaging strategies acknowledge the failure without assigning definitive blame or displaying raw API data. Instead of trying to translate the untranslatable, thoughtful product teams group unknown or vague declines into constructive prompts. A message like, “We couldn’t process this card right now. Please check your details, try a different payment method, or contact your bank,” provides the user with immediate, actionable paths forward. It shifts the focus away from the technical failure and toward a resolution, preserving the customer relationship even when the underlying financial infrastructure is being uncooperative. Checkout.com found that 42% of consumers would stop shopping with a merchant after two failed payment attempts (Source).

Designing a Nuanced Retry Strategy

If user messaging manages the psychological impact of a decline, retry logic handles the mechanical and financial impact. Knowing when and how to retry failed payments is the defining characteristic of a mature payments organization. Because decline codes are inherently untrustworthy, relying solely on them to trigger retries is a strategic error.

The stakes for getting this wrong are surprisingly high. Card networks like Visa and Mastercard actively monitor how merchants behave after a transaction is declined. If a merchant’s system blindly retries a hard decline, such as a card marked as lost or stolen, multiple times in rapid succession, the networks will flag this behavior. Persistent and aggressive retrying of terminal states can lead to substantial financial penalties, increased authorization costs, and even the revocation of processing privileges.

Conversely, being too timid with retries means leaving valid revenue behind. A significant percentage of soft declines will clear if simply attempted again at a different time. The challenge is figuring out which vaguely coded declines are actually soft declines in disguise.

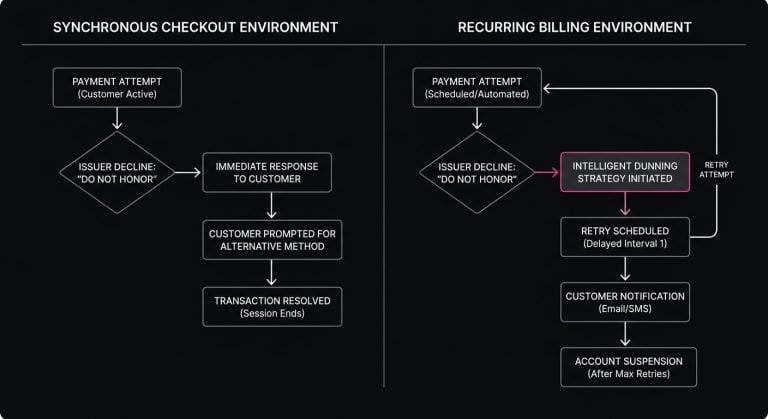

Checkout Versus Recurring Environments

The approach to retrying a payment must change drastically depending on the context of the transaction. Immediate retries are rarely effective in a synchronous checkout environment where the user is present. If an issuer declines a card while the user is actively staring at the screen, retrying the exact same payload three seconds later will almost certainly result in another decline. The only real exception is if the error was explicitly flagged as a localized network timeout. In these user-present moments, the best retry strategy relies on the customer. You can prompt them to verify their security code, enter a different card, or authenticate the purchase via their banking app if strong customer authentication is required.

Subscription payment issues introduce an entirely different operational cadence. The user is typically not present in a recurring billing environment. If a monthly renewal fails with a Do Not Honor code, prompting the user immediately might cause unnecessary churn. Often, the failure is tied to transient variables. The customer might not have received their direct deposit yet, the issuing bank could be running routine weekend maintenance, or the network might be experiencing high latency.

Intelligent dunning strategies replace immediate action in these asynchronous scenarios. Instead of blindly retrying every failed invoice on a daily basis, sophisticated billing systems space out the attempts. They might wait three days, shift the time of day to align with typical banking batch processing hours, or wait for the first or fifteenth of the month when account balances are statistically more likely to be replenished. The decline code is treated as a single data point in a broader context rather than an absolute command.

Shifting Toward Probabilistic Payment Optimization

Given that static rules and literal interpretations of decline codes consistently fall short, the industry has slowly moved toward a probabilistic approach to authorization management. Instead of asking what a specific code means, experienced payment teams ask a different question. They want to know the statistical odds of a specific transaction succeeding if the parameters are modified.

This level of optimization requires looking beyond the isolated decline code and analyzing the surrounding metadata. Payment routing systems evaluate the bank identification number of the card. If a specific identifier from a regional bank historically throws generic decline codes during Sunday maintenance windows, the system can automatically suppress retries for those cards until Monday morning. If a transaction fails with a generic error but the customer has successfully purchased from the merchant three times in the last year, the system might weigh historical trust higher than the immediate decline. This allows for a carefully timed retry rather than an immediate failure state.

Building the infrastructure to support this kind of dynamic, data-driven retry logic is incredibly resource-intensive. It requires deep historical datasets, machine learning models to identify shifting issuer behaviors, and the engineering bandwidth to constantly tune the algorithms. Redirecting core product engineering teams to build a proprietary payment science division simply does not make sense for most merchants. Leveraging specialized tools becomes the most viable path in these cases. Platforms like SmartRetry integrate directly into existing flows to handle the heavy lifting of payment optimization. By utilizing shared network intelligence and smartly retrying declined transactions, these platforms help merchants recover revenue and improve transaction approval rates without requiring them to build analytical infrastructure from scratch. Visa reports that optimization recommendations have achieved up to a 3 percentage point increase in approval rates (Source).

By treating the issuer response as a probabilistic signal rather than an absolute truth, merchants can decouple their success rates from the inconsistencies of the legacy financial system. They stop fighting the unreliability of the codes and start designing systems that anticipate and gracefully navigate around the friction.

Making Peace with the Chaos

The fragmentation of issuer responses is not a temporary bug in the system. It is a structural reality of the global financial network. Thousands of independent institutions operating on varying technological stacks with differing risk appetites will never perfectly align on a single, crystalline taxonomy of decline codes. Acknowledging this reality is the first step toward building better payment flows for product managers, growth leaders, and developers.

The goal is not to achieve perfect clarity on why every single transaction fails, primarily because that level of transparency simply does not exist. Instead, the objective is to build a resilient checkout and billing architecture that degrades gracefully when confronted with ambiguity. This requires writing user messaging that prioritizes guidance over technical accuracy. It also means engineering state machines that can adapt to shifting data patterns and employing retry strategies that balance recovered revenue with strict adherence to network rules.

Navigating the noise of inconsistent decline codes requires a blend of operational pragmatism and technical flexibility. Moving away from rigid, hardcoded interpretations and embracing intelligent, context-aware payment optimization allows teams to transform a source of daily frustration into a measurable competitive advantage. It ultimately ensures that poor communication from an issuing bank does not stand between a willing customer and a successful transaction.