When Issuers Step Into Customer Money Flows, Everyone Wins

The traditional payment ecosystem used to operate on a simple, binary logic. A customer attempts a purchase, the merchant asks for funds, and the issuer checks a static ledger. If the money is present, the transaction goes through. If not, the payment is declined. But the mechanics of consumer finance are rarely that clean. Income arrives in staggered cycles, and bills hit accounts at unpredictable times. The gap between what a customer actually earns and what their ledger shows at 2:00 AM on a Tuesday can be vast. For decades, this gap resulted in countless frustrated buyers and lost revenue for businesses. Now, a subtle but massive shift is underway. The most successful issuers are no longer just guarding a vault of money. They are actively building their systems around the actual flows of customer capital.

By understanding the velocity, timing, and predictability of how money moves into and out of an account, forward-thinking issuers are fundamentally changing the issuer authorization landscape. They are moving away from the rigid constraints of traditional core banking ledgers to embrace dynamic decision-making. For merchants and payment professionals, this shift changes everything from how checkout flows are designed to how recovery strategies are deployed.

The Limitations of the Static Ledger

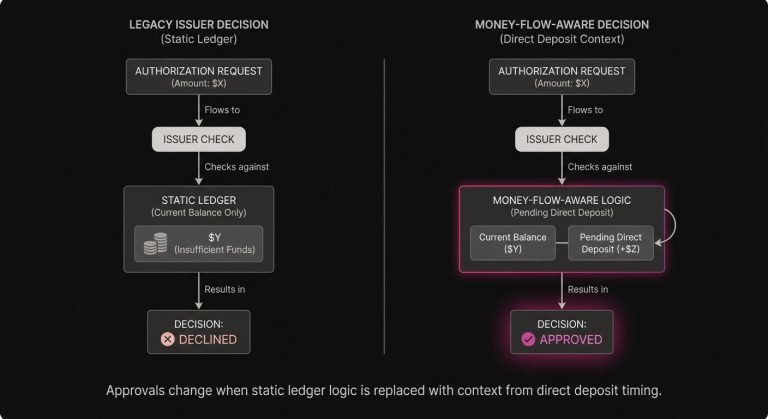

To appreciate why this shift matters, it helps to look at the operational reality of legacy payment processing. Historically, an issuer’s primary job during a transaction was to answer a single question in milliseconds: Does this account have the available balance or credit line to cover this specific amount right now?

It is a highly efficient system, but it lacks context. A static ledger does not know that a customer’s direct deposit typically clears on the 15th of the month, nor does it factor in that the customer has successfully paid this exact merchant $14.99 on the same day for the last thirty-six months. It only sees a balance of $12.00 against an authorization request for $14.99, resulting in an immediate decline.

This lack of context has been a major driver of payment issues across the card declines landscape. For merchants, a decline based on a temporary lack of funds looks operationally identical to a decline based on a fundamentally dead account. The merchant receives a generic decline code, the customer receives an opaque error message, and a potentially long-term revenue stream is jeopardized over a timing mismatch of just a few hours.

Reading the Flow of Funds

The issuers pulling ahead in the market have realized that a static balance is a poor indicator of a customer’s actual purchasing power or reliability. Instead of treating every authorization as an isolated event, they are analyzing the broader financial flow.

Modern issuing infrastructures can detect patterns in direct deposits, recurring transfers, and standard spending behaviors. If an issuer knows a payroll deposit is currently pending and will settle by morning, they may choose to approve a transaction that would otherwise trigger a non-sufficient funds decline. They are essentially underwriting the micro-timing of the customer’s money flow.

This approach dramatically improves the user experience and reduces unnecessary checkout issues. For the issuer, it builds immense top-of-wallet loyalty. Customers tend to favor the card or account that reliably works without causing friction or embarrassment at the point of sale. For the merchant, it means higher initial approval rates without requiring any change to their own checkout architecture, and a strong bank authorization rate averages around 85% for online merchants (Source).

The Shift from Risk Avoidance to Flow Facilitation

Historically, issuers operated primarily as risk managers where every transaction was viewed through the lens of potential loss. While risk management remains critical, the framing has evolved, and leading issuers now view themselves as facilitators of commerce.

When an issuer builds into the customer’s money flow, they are actively looking for reasons to approve a transaction rather than default reasons to decline it. This might involve allowing a small negative balance buffer for long-standing customers or offering a temporary grace period for recurring bills. By absorbing a minuscule amount of calculated timing risk, these issuers are capturing significantly higher transaction volumes.

The Anatomy of the Modern Issuer Response

As issuers become more sophisticated, the payment processing flow becomes far more nuanced. When a transaction is submitted, the authorization request travels through the merchant’s gateway, to the acquirer, across the card network, and finally to the issuer.

In the past, the issuer response was often a blunt instrument. A code like Do Not Honor or Insufficient Funds provided little actionable intelligence. Today, the conversation between the merchant and the issuer is richer, driven by enhanced data and better signaling.

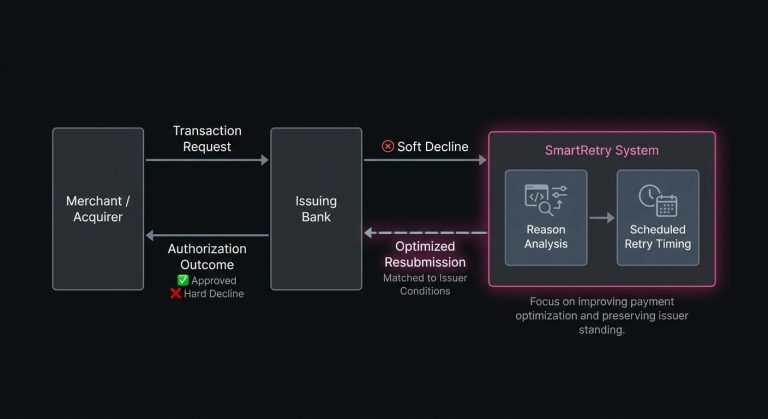

However, even with smarter issuers, payment failures still occur. The difference now is that these failures are often highly contextual. A decline might not mean a permanent rejection, but rather a request to try again later. If an issuer is tracking a customer’s spending velocity and notices unusually high activity, they might issue a soft decline as a temporary protective measure. If the merchant understands this operational reality, they know that the right response is patience and a well-timed subsequent attempt rather than immediate panic.

Navigating the Recurring Dilemma

Nowhere is the impact of smart issuers felt more deeply than in the world of recurring billing. Subscription payment issues have long been the bane of growth teams. Churn caused by involuntary payment failures often outpaces active cancellations, silently eating away at a company’s lifetime value metrics.

Recurring payments challenge the static ledger model because they happen in the background. The customer is not actively looking at their balance before initiating the purchase, so if a subscription attempts to renew the day before payday, the risk of a decline spikes.

Issuers that understand money flows recognize the predictable nature of subscriptions. They know that a Netflix or Spotify charge is an expected part of the customer’s monthly financial rhythm. Some innovative banking platforms even provide tools within their consumer apps that forecast upcoming subscriptions, ensuring the customer leaves enough funds available.

Network Tokens and the Trust Paradigm

To facilitate these approvals, issuers rely heavily on merchants providing the right data. This is where technologies like network tokenization come into play. When a merchant uses a network token instead of a raw Primary Account Number, they are signaling to the issuer that the transaction is part of an established, secure relationship.

Issuers strongly prefer network tokens because they remain valid even if the underlying physical card is lost or replaced. By adopting tokenization and properly flagging recurring transactions with the correct network indicators, merchants give smart issuers the exact data they need to confidently approve the payment, directly lifting the transaction approval rate.

The Merchant’s Strategic Response: Payment Optimization

If issuers are moving away from brute-force decision-making and toward nuanced flow analysis, merchants must adapt their own systems to match. It is not enough to simply send a transaction into the void and hope the issuer approves it. Modern revenue teams must treat payment optimization as a core operational discipline.

Payment optimization involves looking at the entire lifecycle of a transaction to remove friction and increase the probability of success. It requires understanding the subtle differences between acquirers, the specific preferences of regional issuers, and the optimal time to request an authorization.

For example, if data shows that an issuing bank in a specific market consistently declines recurring payments submitted at midnight but approves them at 9:00 AM, a merchant optimizing their flow will shift their billing batch times accordingly. The goal is to align the merchant’s request for funds with the issuer’s preferred window for releasing them.

The Nuance of Resolving Declines

Despite the best optimization efforts, some percentage of transactions will inevitably be declined. How a merchant handles these declines separates average operational teams from high-performing ones.

The immediate instinct for many merchants is to force the transaction through by repeatedly attempting to process the card. This brute-force method ignores the reality of how modern issuers operate. Hammering an issuer’s authorization system with identical requests does not magically generate funds in the customer’s account. In fact, it often triggers fraud-prevention algorithms, turning a temporary soft decline into a permanent hard decline and potentially penalizing the merchant’s network standing.

To effectively reduce payment declines, businesses must interpret the underlying reason for the failure. A hard decline indicating a lost card or closed account means no amount of retrying will work, and the customer must be engaged directly for a new payment method. On the other hand, a soft decline indicates a temporary block or insufficient funds. In these cases, the transaction is often recoverable provided the merchant employs a thoughtful strategy.

Intelligent Recovery and Operational Harmony

This is where the concept of intelligent retries changes the financial equation. Rather than guessing when a customer might have funds, sophisticated revenue teams rely on data-driven recovery models. They look at historical success patterns, day-of-week trends, and the specific decline codes returned by the issuer to schedule subsequent attempts.

When a merchant encounters a soft decline, the traditional approach was often to simply run the card again later and hope for a different outcome. But as issuers become more sophisticated about how and when funds move, merchants need an equally thoughtful approach to payment recovery. This is the operational philosophy behind platforms like SmartRetry, which focus on payment optimization and intelligent retries of declined transactions. By analyzing the underlying reasons for a failure and timing retries to align with actual financial realities, rather than relying on aggressive or blind attempts, merchants can successfully recover revenue and improve transaction approval rates. This strategy also keeps them in good standing with the issuing banks.

The focus shifts from simply retrying a card to gracefully recovering a customer relationship. By treating a declined transaction as a temporary scheduling issue rather than a permanent failure, merchants can recover significant revenue without frustrating the customer or alerting the issuer’s risk systems. For a merchant processing $1B annually, a 1% lift in authorization rate equals $10M recovered without new customers or additional spend (Source).

Balancing Aggression with Network Health

There is always a trade-off in payment recovery. Attempting to retry failed payments too rarely leaves valid revenue on the table. However, retrying them too aggressively incurs excessive network authorization fees and risks compliance penalties from Visa or Mastercard.

The optimal strategy requires balance and an understanding that authorization networks are probabilistic. A strategy that yields a 15% recovery rate on the first retry might drop to a 2% recovery rate by the fourth attempt. At a certain point, the operational cost of the retry outweighs the expected value of the recovered funds. Experienced payment professionals constantly tune these thresholds, optimizing for the highest possible net revenue rather than chasing a theoretical 100% approval rate.

Looking Ahead: A Collaborative Payment Ecosystem

The evolution of issuer behavior from static gatekeeping to dynamic flow analysis represents a maturing of the digital economy. The historical friction between merchants trying to pull funds and issuers trying to protect accounts is gradually giving way to a more collaborative ecosystem.

As issuers pull ahead by building deeply into their customers’ money flows, they are essentially doing the heavy lifting of contextual risk analysis. They are operating on the premise that they know their customers better than anyone and understand exactly when they are good for the funds.

For merchants, this is a massive opportunity. By aligning their own payment processing logic with the intelligence of modern issuers, utilizing clean data, embracing tokenization, and deploying smart recovery strategies when things go wrong, they can ride the wave of these improvements. The businesses that understand and adapt to this shift will naturally see fewer friction points, stronger customer retention, and a more resilient revenue stream. Ultimately, when the systems that hold the money and the systems that request the money finally speak the same language, the entire ecosystem operates exactly as it should: quietly, seamlessly, and effectively.