Why Virtual Card Payments Fail in Travel and How Payment Teams Improve Approval Rates

March 8, 2026

![]() 12 min

12 min

The global travel industry moves trillions of dollars every year, but much of that money changes hands quietly behind the scenes. When a traveler books a room through an online travel agency or a corporate booking tool, they pay the agency directly. The agency must then route those funds to the hotel or airline.

This is where the industry’s underlying complexity really begins. Instead of passing the traveler’s physical credit card details to the front desk, the agency typically generates a single-use virtual credit card. It sounds like a remarkably elegant and secure solution, as the virtual card is loaded with the exact cost of the reservation, securely transmitted to the hotel’s property management system, and charged when the guest checks out.

In a perfectly sterile environment, this system prevents fraud, automates reconciliation, and makes accounting practically effortless. In the real world, however, payment issues surface constantly and unpredictably. The exact moment a virtual card is declined at the front desk, a quiet administrative discrepancy morphs into a cascading operational problem.

The Invisible Engine of Global Travel

To understand why paying a hotel for a booked room is so complicated, you have to look at the card network that supports the travel ecosystem. In the early days of online travel, agencies and travel management companies relied on direct billing, rolling credit lines, and cumbersome monthly invoices to settle up with properties. This created a reconciliation nightmare, as trying to match a massive monthly wire transfer to thousands of individual guest stays across multiple global properties required armies of accountants.

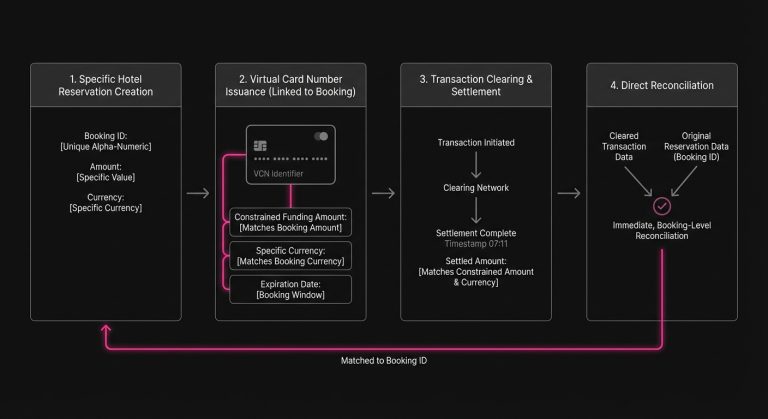

Virtual Card Numbers changed the paradigm entirely. A VCN is essentially a standard 16-digit primary account number generated on the fly for a singular purpose. It is tied to a specific booking, loaded with a precise monetary amount, locked to a specific currency, and set to expire within a tight timeframe.

Because each VCN maps directly to a single reservation, the reconciliation process becomes instantaneous. Once the transaction clears, the agency knows exactly which booking has been paid. By running these transactions over standard card networks, travel companies can earn interchange rebates, turning the payment process from a massive cost center into a revenue-generating asset. But the very features that make virtual cards so secure and precise are exactly what make them so fragile in the wild.

Where the Payment Processing Flow Breaks Down

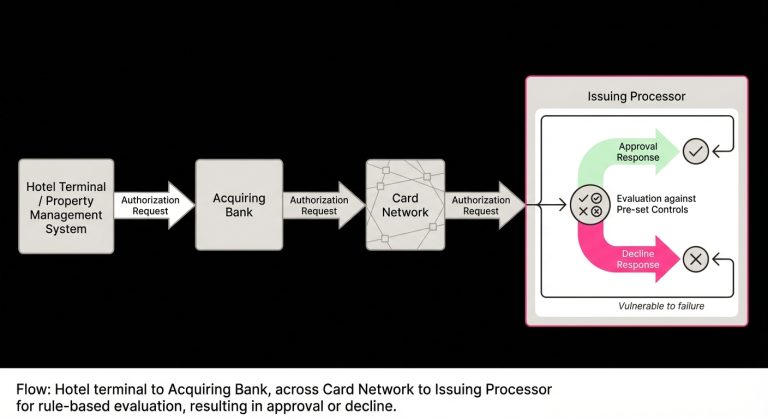

The paradox of virtual card issuing is that the tighter you control the authorization parameters, the more payment failures you will inevitably experience. When a virtual card is swiped or keyed into a property management system, the authorization request travels from the hotel’s point-of-sale terminal, through their acquirer, across the card network, and finally lands at the agency’s issuing processor.

The issuer then evaluates the request against the strict rules established when the card was generated. The transaction is approved if the request matches perfectly, but if anything deviates, the issuer returns a decline. While this binary logic is excellent for preventing fraud, it routinely collides with the messy reality of the hospitality industry.

The Exact Amount Dilemma

The most common reason a VCN encounters a declined status is an amount mismatch. When an agency generates a virtual card for a two-night stay, they fund it based on the exact negotiated rate and the anticipated taxes provided in the booking feed.

However, local municipalities frequently update city taxes, or a hotel might add an unforeseen daily resort fee at the property level. If the virtual card is funded for exactly $400.00 and the hotel attempts to authorize $404.50 to cover a newly implemented local tax, the card network sees an overcharge attempt. The issuer immediately blocks the transaction because it looks like fraud, even though to the hotel, it just seems like a bad card.

The Merchant Category Code Trap

MCC to ensure the funds are only spent on the intended travel service. A VCN issued for a hotel stay, for example, will typically be restricted to MCC 7011 for lodging.

However, hotel infrastructure is rarely uniform. A property might process front desk payments through a terminal correctly registered as lodging. If the night auditor attempts to process the virtual card through a terminal located at the hotel’s restaurant or an attached conference center, that specific terminal might be registered as dining or generic retail. When this happens, the MCC on the authorization payload fails to match the restriction on the VCN. The result is an immediate decline, even though the charge is entirely legitimate and the amount is perfectly accurate.

Currency Fluctuations and Cross-Border Complexities

Travel is inherently global, which means cross-border payments are the default state. An agency based in London might issue a virtual card in GBP to pay a hotel in Tokyo charging in JPY.

By the time the guest actually checks out and the hotel processes the charge, the foreign exchange rate may have drifted from the time the booking was initially made. If the agency funded the VCN based on the exchange rate from three months prior, the converted amount requested by the hotel’s acquirer might exceed the funded limit.

Some hotel acquirers also utilize Dynamic Currency Conversion, attempting to capture the foreign exchange markup by converting the charge into the card’s native currency at the point of sale. This inevitably skews the math, altering the final requested amount by a few percentage points and causing an automatic failure at the issuing level.

Interpreting the Issuer Response

When these failures happen, the operations team at the travel agency or travel management company is left to piece together the puzzle. Unfortunately, the card networks were designed decades ago for consumer retail, not complex B2B programmatic issuing.

When a hotel processes a VCN and it fails, the issuer response sent back to the terminal is often incredibly generic. The hotel might see codes such as 05 Do Not Honor or 51 Insufficient Funds.

In a consumer context, an insufficient funds error means the cardholder’s bank account is empty. In a B2B virtual card context, it simply means the hotel tried to charge more than the micro-limit placed on that specific VCN. The front desk agent looking at the screen doesn’t know this, however. They just know the payment failed. This leads to a frantic chain of manual interventions, phone calls to the agency’s support desk, and a disrupted guest experience.

The Operational Toll of a Card Declined

In consumer payments, a declined transaction usually means an abandoned online shopping cart, but in B2B travel, the stakes are considerably higher. The traveler is often standing right there in the hotel lobby with their luggage, trying to check out and catch a flight.

When the agency’s virtual card fails, the hotel still needs to get paid. If they cannot reach the agency’s support desk immediately, they will turn to the guest and ask them to provide a personal credit card to cover the balance. For a corporate traveler whose company supposedly pre-paid for the room, or a vacationer who saved up for a comprehensive package deal, being asked to pay again is a brand-destroying experience.

Behind the scenes, the agency faces a massive operational headache. They are left with an unused virtual card holding funds, a frustrated customer requesting a reimbursement for the out-of-pocket expense, and a broken reconciliation loop. An analyst must manually intervene, figure out why the charge failed, issue a refund, and balance the books. The sheer cost of this manual payment recovery heavily eats into the thin margins of the travel booking.

Straight-Through Processing and Modern Infrastructure

To mitigate the friction of manual hotel terminals, the industry has steadily moved toward Straight-Through Processing. In this model, the travel agency or management company doesn’t rely on the hotel to manually type the card number into a physical terminal. Instead, the payment is pushed directly via API integration to the hotel’s acquiring partner or property management system.

This fundamentally shifts the power dynamic. Instead of waiting for a hotel to initiate the charge and hoping it works, the travel company pushes the payment and receives the authorization response directly in their own system. If a payment push encounters a declined status, the travel company’s software knows immediately and can take automated action.

This is where the concept of intelligent recovery transitions from a theoretical idea into a highly functional reality. Because the software controls the initiation of the charge, it can read the underlying network data, understand the nature of the failure, and adapt instantly.

Strategic Payment Optimization and Intelligent Retries

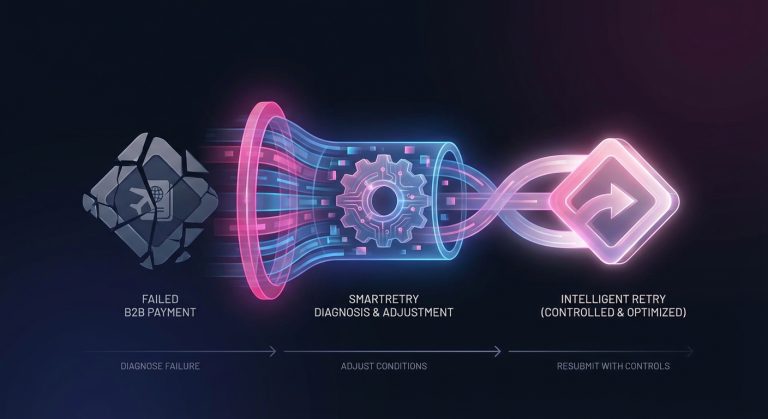

When a transaction fails due to a rigid parameter on a virtual card, the traditional response was to have a human agent log into the issuing platform, manually adjust the VCN limit by a few dollars, and ask the hotel to try again. Today, intelligent systems handle this programmatically.

If an authorization request fails because the amount is exactly 1.5% higher than the funded limit, an optimized payment system can recognize this as a likely municipal tax discrepancy based on historical data from that specific property. The system can automatically adjust the authorization controls on the VCN, increasing the limit to accommodate the slight overage without opening the card up to massive fraud, and clear the path for a successful charge.

When a B2B push payment or a corporate billing cycle hits a snag, relying on manual follow-up is a losing battle. This is where automated payment infrastructure changes the game. Platforms like SmartRetry act as a natural extension of a company’s financial stack, focusing entirely on payment optimization and intelligent retries of declined transactions. By programmatically evaluating why a transaction failed and adapting the next attempt based on historical data, these systems help merchants recover revenue and improve transaction approval rates without requiring an army of analysts to intervene.

In an STP environment, the ability to automatically retry failed payments with an adjusted payload or during a different network window is a massive operational advantage. A transient network timeout, a temporary gateway error on the hotel’s side, or a misconfigured MCC can often be resolved simply by routing the transaction differently or applying a targeted retry strategy.

Balancing Margins with the Transaction Approval Rate

The primary goal of optimizing these flows is to achieve a higher transaction approval rate without sacrificing margin protection. It is relatively easy to achieve a 100% approval rate by removing all restrictions from virtual cards to let hotels charge whatever they want, but doing so would instantly destroy a travel agency’s profitability through unchecked overcharges and resort fees. One industry benchmark has put virtual card approval rates at 99.1% versus 85% for consumer cards (Source).

The true art of payment optimization in B2B travel lies in dynamic tolerances. Experienced payment teams analyze vast amounts of historical authorization data to create probabilistic rules. If a specific airline is known to batch process their virtual cards at strange times resulting in network timeouts, the system will anticipate this and automatically trigger a retry strategy tailored to that airline’s gateway behavior. If a specific chain of hotels in Europe consistently applies an unpredictable cross-border conversion fee, the system can apply a dynamic 2% tolerance strictly to VCNs issued to that specific merchant group.

By applying tolerances surgically rather than broadly, companies maintain their financial security while drastically reducing the volume of manual support tickets.

The Overlooked Engine: Front-End Acquiring

While the complexities of virtual card issuing dictate the back-end payment to the supplier, it is impossible to ignore the front-end of the ecosystem. To fund those virtual cards, the travel agency or travel management company must successfully acquire funds from the traveler or the corporate client.

If a corporate travel platform operates on a retainer model and experiences subscription payment issues with a major client, or an online travel agency experiences checkout issues when a consumer tries to book a flight, the entire chain halts. You cannot issue a virtual card to pay a supplier if you haven’t successfully captured the funds on the front end.

The strategies used to optimize the acquiring side are heavily tied to the same principles of intelligent routing and automated recovery. When a traveler’s card is declined at checkout, utilizing network tokens, updating account credentials automatically, and employing intelligent recovery can often salvage the booking before the customer abandons the site. A resilient B2B payment architecture views the front-end capture and the back-end VCN issuance as one continuous, unified flow of revenue.

Moving Toward Fluid Payment Architecture

The days of treating B2B travel payments as a static, pass-or-fail administrative task are ending. The sheer volume of transactions moving through global travel networks requires a much more nuanced approach. Virtual card transactions in the travel sector are projected to increase to 740.7 million by 2028 from 189.9 million in 2023 (Source). As properties adopt fragmented property management systems and local jurisdictions continue to complicate tax structures, the gap between what a travel company expects to pay and what a property actually attempts to authorize will only widen.

Building a resilient infrastructure means accepting that declines are a natural byproduct of the ecosystem, not necessarily a fundamental failure. The goal is no longer to prevent every single discrepancy from happening, but to design systems that absorb the discrepancies, interpret the network responses accurately, and adjust the issuing parameters in real time.

When payment logic shifts from rigid rules to dynamic, probabilistic systems, the friction at the front desk disappears. The travel agency protects its margins, the hotel gets paid without hassle, and the traveler simply checks out and heads to the airport, completely unaware of the complex digital orchestration that made their trip possible.

Still letting failed transactions slip through?

SmartRetry turns declines into approvals - automatically, intelligently, and without changing your payment provider.

Frequently asked questions about this topic

Share this article

Author

Roi Lagziel

Roi Lagziel is a payments engineer specializing in authorization optimization, retry strategies, and issuer-level behavior. His work focuses on building practical, data-driven systems that help payment teams reduce false declines and recover lost revenue.

Read all articles >More in Payment Approval Optimization:

April 16, 2026

Why Transaction Approval Rate Is Misleading and What Payment Teams Should Measure Instead

This article explains why blended approval rate can distort payment decisions and how teams can use recovery, cohort, and retry metrics to protect revenue and reduce false declines.

March 8, 2026

The Invisible Logic of 3D Secure: How Payment Teams Balance Fraud, Friction, and Revenue

This article explains how payment teams can use 3D Secure, exemptions, and soft-decline handling to cut false declines, protect conversion, and improve recurring revenue performance.

March 8, 2026

Beyond the Monolith: Why Global Scale Demands a Multi-Acquirer Mindset

This article explains how multi-acquirer setups, local routing, and smarter retries help payments operators lift approvals, cut false declines, and protect revenue as global volume grows.