The Mechanics of High-Yield Revenue Recovery in Modern Payments

The numbers sound slightly fictional at first glance: thirty-five to fifty percent. When teams first hear these figures, skepticism is a natural reaction because most standard recovery schedules max out around the ten to fifteen percent mark. Hitting the fifty percent threshold feels less like optimization and more like algorithmic alchemy. There is no magic behind these numbers, however. Instead, it requires a methodical, deeply informed approach to navigating the differences between hard and soft declines. It comes down to understanding exactly why an authorization failed and knowing the precise moment to ask for it again. For merchants operating at scale, moving past basic dunning to intelligent recovery is one of the most effective ways to protect top-line revenue and extend customer lifetime value.

The Default State of Decline Recovery

To understand how high-performing teams capture such a significant portion of lost revenue, it helps to look at the baseline. For years, the standard approach to payment failures was largely passive. A recurring charge would fail, and the system would wait a predetermined number of days, usually three, five, or seven, before trying again. If the card declined a second or third time, the customer was moved into a dunning sequence and received automated emails asking them to update their billing information.

This static, rules-based approach was built for a simpler era of digital commerce. It assumes all declines are created equal and that time is the only variable worth adjusting. But the reality of modern payment networks is vastly more complex. Every authorization request passes through a gauntlet of risk checks, velocity filters, and fraud models at both the network level and within the issuing bank. When an issuer denies a request, they communicate specific, albeit sometimes obscured, information about the state of the account or the nature of the transaction.

High-performing recovery programs operate on the premise that a decline is not a definitive end state but rather a data point in an ongoing conversation with the issuer. By treating declines as probabilistic rather than absolute, payment operations teams can deploy nuanced strategies that align with the specific reason for the failure. This dramatically improves the chances of an eventual approval, and Stripe reports an average recovery rate of 57% for failed recurring payments using its recovery tools (Source).

Decoding the Ambiguity of Issuer Responses

The foundation of any sophisticated attempt to reduce payment declines is a granular understanding of decline codes. When an authorization is attempted, the issuing bank returns a two-digit code indicating the result. Some of these are hard declines, such as stolen cards, closed accounts, or invalid primary account numbers, known as PANs. In these scenarios, retrying the transaction is not only futile but actively detrimental. Card networks heavily penalize merchants who repeatedly attempt to charge dead credentials.

The real opportunity lies in soft declines. These are temporary states involving insufficient funds, network timeouts, or suspected fraud triggers. A soft decline indicates that the credential is valid, but the current context of the transaction is unacceptable to the issuer. The challenge is that issuers are notoriously opaque in their communication. A significant percentage of soft declines fall under generic catch-all codes, leaving the merchant to guess the underlying issue.

The Catch-All Enigma

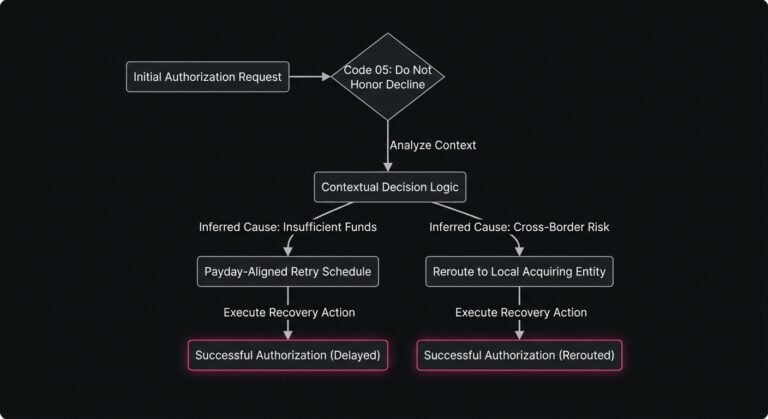

The most infamous of these is code 05, Do Not Honor. Historically, issuers used this code for a wide variety of reasons ranging from a lack of funds to a tripped velocity filter. While card networks have recently mandated better categorization and introduced more specific decline codes, generic responses still represent a massive portion of checkout issues.

High-level recovery programs do not take a Do Not Honor response at face value. Instead, they use contextual data to infer the probable cause. If the transaction was attempted on the 28th of the month and the customer has a history of successful payments, the system might infer an insufficient funds situation and schedule a retry for the first of the following month. Alternatively, if the transaction was flagged during a suspected fraud trigger, the system might route the subsequent retry through a local acquiring entity to lower the perceived risk score.

The Architecture of an Intelligent Retry

Once the nature of the decline is understood, the next variable is timing. The blunt-force approach of static intervals ignores the behavioral and systemic realities of how money moves. Strategic retry logic looks at a multitude of factors, including the day of the week, the time of day, and the specific habits of the customer base.

For many consumer-facing businesses, the concept of the payday cycle is critical. Consumers in many regions are paid on the 1st and 15th of the month, or on specific days like alternating Fridays. Attempting to retry failed payments associated with insufficient funds on a Tuesday afternoon mid-month is statistically unlikely to succeed. High-performing systems map retry attempts to these natural liquidity events, which significantly boosts the likelihood that funds will be available.

Timing must also account for the issuer’s internal batch processing schedules. Many traditional banks process deposits and clear holds in batches overnight. A retry executed at 11:00 PM might fail, while the exact same request submitted at 3:00 AM the following morning succeeds effortlessly. Synchronizing recovery efforts with these banking rhythms is a hallmark of an optimized payment flow.

Network Rules and the Cost of Aggression

There is a delicate balance to strike between persistence and penalty. Card networks like Visa and Mastercard enforce strict rules regarding how often and under what circumstances a declined transaction can be resubmitted. Overly aggressive retry strategies, often referred to as hammering the network, can trigger severe financial penalties and damage the merchant’s standing with issuers.

When an issuing bank observes a merchant repeatedly submitting the same doomed transaction, the merchant’s overall trust score drops. This degradation in trust can cause a ripple effect that lowers the transaction approval rate for otherwise healthy, legitimate authorizations across the entire account. Intelligent recovery programs are acutely aware of these network limits. They utilize logic that pauses or entirely halts retries before approaching the threshold of network penalties. The ultimate goal is maximum recovery with minimal network noise.

Pre-Authorization Mechanics and Credential Health

Before a transaction ever reaches the authorization stage, significant work must be done to ensure the credential is in its best possible state. A vast number of subscription payment issues stem from the natural lifecycle of credit and debit cards. Cards expire, get lost, or are replaced due to fraud. When this happens, the credential sitting in the merchant’s vault becomes obsolete and guarantees a hard decline on the next billing cycle.

Historically, merchants relied solely on the customer to update this information. Sophisticated programs now utilize network-level tools to preemptively heal credentials. Account Updater services provided by the major card networks allow merchants to ping the network before an authorization attempt, checking to see if a newer PAN or expiration date exists for a specific token.

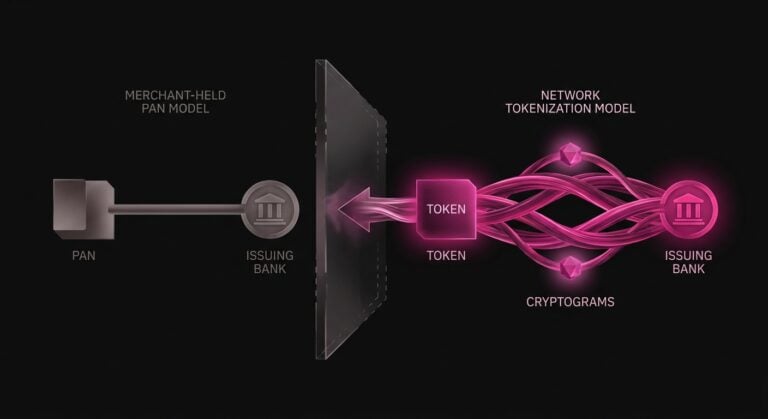

The Role of Network Tokenization

Taking this a step further, the adoption of network tokenization has fundamentally altered the payment recovery landscape. Unlike traditional merchant tokens, which are simply database references to a PAN stored in a gateway vault, network tokens are issued directly by the card brands. Because they are tied directly to the issuing bank, they update automatically when the underlying card changes.

Network tokens also carry domain-specific cryptograms for each transaction, signaling to the issuer that the transaction is highly secure. Issuers tend to trust these tokens more than raw PANs, often granting them higher base approval rates and fewer soft declines. By converting stored cards into network tokens, merchants solve a significant portion of payment issues before they ever manifest as a decline. This clears the runway for recovery logic to focus exclusively on temporary, circumstantial failures. American Express, Visa, Mastercard, and Discover in the United States (Source).

Orchestrating the Recovery Stack

Managing this matrix of decline codes, routing rules, network limits, and tokenization protocols is not a task suited for manual intervention on a per-transaction basis because the permutations are simply too vast. This reality has driven the shift toward dynamic, machine-learning-driven recovery models. Rather than relying on rigid conditional rulesets, optimized payment stacks utilize algorithms that ingest millions of data points to determine the best next action for any given decline.

These systems analyze the Bank Identification Number, or BIN, along with the time of day, the specific acquiring channel, the transaction amount, and historical issuer behavior to score the probability of a successful retry. If the probability is high, the system executes the retry. When the probability is low, the system might delay the attempt or shift the transaction into a customer-facing dunning flow to request alternative payment methods.

This is where dedicated optimization layers become highly valuable within a merchant’s technology stack. Platforms like SmartRetry focus specifically on payment optimization and intelligent retries, helping merchants analyze these complex variables in real time. By abstracting the heavy lifting of machine learning and network compliance, these systems allow merchants to recover revenue and improve transaction approval rates without needing an entire in-house team of payment data scientists to build and maintain the infrastructure. In one case study, improving Stripe recovery from 39% to 62% was associated with a $320k annual recurring revenue increase (Source).

Churn, LTV, and the Compounding Value of Recovery

To fully appreciate why a 35 to 50 percent recovery rate is so highly sought after, operators must look beyond the immediate transaction value. In the context of recurring revenue models and digital subscriptions, a payment failure is not just the loss of a single month’s fee. It is the potential loss of that customer’s entire remaining lifetime value, or LTV.

This phenomenon is known as involuntary churn. It occurs when a customer who fully intends to continue using a service is canceled simply because the payment infrastructure failed to capture the funds. If a subscription business has an average customer lifespan of twenty-four months and a payment fails in month six, the business isn’t just losing month six’s revenue. It is forfeiting the remaining eighteen months of predictable cash flow.

When a high-performing recovery program steps in and salvages that transaction, it effectively reactivates that future revenue stream. The compounding mathematical effect is staggering. A business that improves its recovery rate from fifteen percent to forty percent will see a disproportionately large impact on its valuation and growth metrics over a multi-year period, simply by retaining the customers it already spent acquisition dollars to acquire.

Redefining Success Metrics in Payment Operations

As organizations mature in their approach to payment optimization, the metrics they use to define success must also evolve. Historically, the primary KPI for payment health was the initial authorization rate, which is the percentage of transactions approved on the very first attempt. While this remains a crucial metric of overall checkout health, it only tells part of the story.

A hyper-focus on first-pass authorization can sometimes lead to overly conservative risk settings. In these cases, legitimate but slightly complex transactions are preemptively blocked just to keep the approval ratio artificially high. High-performing teams look at a dual metric instead, tracking the first-pass approval rate alongside the ultimate recovery rate.

The true measure of a resilient payment ecosystem is how much total intended revenue is captured by the end of a given billing cycle. This acknowledges that the payment network is a noisy, probabilistic environment where initial friction is inevitable. By tracking the percentage of soft declines that are ultimately converted into settled funds, growth leaders gain a much clearer picture of the actual operational efficiency of their payment stack. Approval rate is defined as the percentage of subscription payment volume successfully recovered by any means after a failure (Source).

Moving from a passive acceptance of declined transactions to an active, intelligent recovery posture requires a shift in perspective. Merchants must view their payment flows not as a static utility, but as a dynamic and optimizable engine. The tools, data, and methodologies already exist to reclaim up to half of the revenue typically written off as a cost of doing business. For teams willing to dig into the mechanics of issuer behavior, credential health, and temporal logic, the financial returns are both immediate and enduring.