The Expensive Silence Between ‘Approved’ and ‘Paid’: Why Auth and Capture Aren’t the Same Thing

March 8, 2026

![]() 13 min

13 min

The Expensive Silence Between ‘Approved’ and ‘Paid’: Why Auth and Capture Aren’t the Same Thing

There is a moment of relief in every transaction. The screen loads. The green checkmark appears. The system returns an ‘authorization’ status. In that split second, it feels like the money has successfully moved from the customer’s account to yours. But experienced payments professionals know this is just an illusion. A successful payment authorization is simply a promise. The actual movement of funds does not happen until the capture phase. And between those two distinct events lies a quiet, highly consequential window where things can, and often do, drift off course.

Understanding the mechanics of this silent gap is a fundamental part of payment optimization. Many merchants operate under the assumption that an authorization equates to guaranteed revenue, only to discover discrepancies during reconciliation. Exploring the nuances of this process reveals why authorizations expire, how partial captures complicate operations, and why bridging the gap thoughtfully is necessary for protecting a company’s bottom line.

The Mechanics of a Promise

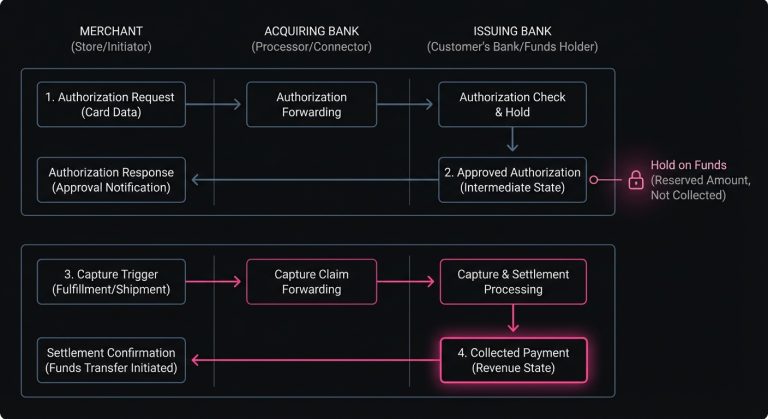

When a customer checks out, the initial request sent through the payment processing flow is usually an authorization. The acquiring bank asks the issuing bank a simple question: Does this cardholder have the funds or credit available for this specific amount, and is the account in good standing?

If the issuer response is positive, they place a hold on those funds. The customer’s available balance decreases, but the money has not actually left the bank. The issuer is essentially setting the money aside on a virtual shelf, waiting for the merchant to return and claim it.

This two-step dance was originally designed for the physical world. A hotel needs to ensure a guest can cover room charges and potential damages before handing over the keys, but the final bill isn’t known until checkout. A restaurant authorizes a card for the meal’s cost but needs to leave room for a tip to be added later.

In the digital economy, this separation remains incredibly useful. It allows merchants to verify funds before picking and packing physical goods, or fraud teams to conduct asynchronous reviews without holding up the checkout experience. However, the flexibility of separating these two actions also introduces a time delay, and time is often the enemy of a seamless transaction.

The Expiration Clock on Authorized Funds

An authorization is not an indefinite reservation. Issuers have strict timelines for how long they will hold funds on a customer’s behalf before releasing them back into the available balance.

For most major card networks, a standard credit card authorization remains valid for a few days, typically ranging from three to seven, depending on the card network and the specific network rules. Debit cards, which tie directly to a consumer’s liquid cash, often have even shorter authorization windows.

If a merchant waits too long to capture the funds, the authorization simply evaporates. The money goes back into the customer’s account, and the merchant is left holding an empty promise. If the merchant still needs to be paid-perhaps because a physical item was delayed in the warehouse and is only now shipping-they must initiate a new transaction.

This late attempt can easily result in a soft decline scenario. By the time the merchant tries to run the charge again, the customer might have spent those funds elsewhere, reached their credit limit, or lost their card. What was once a highly probable sale becomes an unexpected revenue leak, simply because the timing between the two stages was mismanaged.

When Fulfillment Outpaces the Hold

Delays in fulfillment are one of the most common reasons merchants stumble over authorization timelines. Supply chain hiccups, customized products that take weeks to manufacture, or pre-orders for items releasing months in the future all stretch the limits of standard payment processing rules.

To handle extended timelines, merchants often have to adjust their capture strategies. Some choose to capture funds immediately at checkout, even if the item won’t ship for weeks. While this secures the revenue and eliminates the risk of an expired authorization, it introduces other operational considerations. Consumers generally prefer not to pay for things they haven’t received, which can lead to higher customer support inquiries and an increase in chargebacks.

Alternatively, a merchant might choose to perform a nominal authorization-perhaps for zero or one dollar-just to verify the card is active, waiting to authorize the full amount when the item actually ships. While friendlier to the consumer, this approach introduces payment issues later in the cycle. When the time comes to authorize the full amount, the transaction may fail, leaving the merchant with ready-to-ship inventory and no secure way to collect payment.

The Complexity of Partial Captures

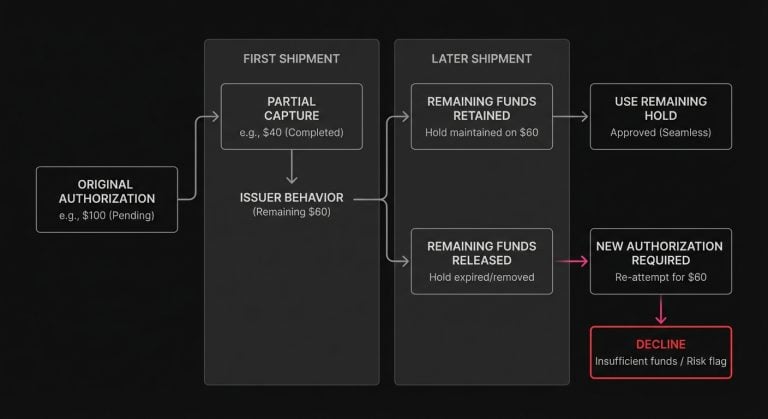

The operational reality becomes even more intricate when a single order is split across multiple shipments. Imagine a customer orders a laptop, a carrying case, and a specialized cable. The total authorization covers all three items. The carrying case and cable ship immediately, but the laptop is backordered.

When the first two items ship, the merchant issues a partial capture against the original authorization. This sounds straightforward, but different issuers handle partial captures differently. Some issuers interpret a partial capture as the conclusion of the entire transaction and immediately release the remaining held funds. Others will maintain the hold for the remaining balance until the expiration clock runs out.

If the issuer releases the remaining funds upon the first partial capture, the merchant no longer has a hold on the funds needed for the laptop. When the backordered laptop finally ships a week later, the merchant must secure a new authorization. If that second attempt results in a payment declined status, the merchant is forced into a difficult customer service interaction to secure an alternative payment method.

The Hidden Cost of Orphaned Authorizations

Not all payment failures stem from the inability to capture. Sometimes, the problem lies in capturing funds but leaving lingering authorizations unresolved. This phenomenon, often called an orphaned authorization, occurs when an authorization is successfully obtained, but the transaction is canceled or abandoned before the capture phase, and the merchant’s system fails to notify the issuer.

From the merchant’s side, an abandoned cart or a canceled order might seem like a closed loop. But from the issuer’s perspective, the funds are still actively being held for the merchant.

This creates measurable friction for the cardholder. Their available credit is reduced, or their checking account balance is artificially lowered, tying up funds they might need for other purchases. If a customer tries to buy groceries and finds their account depleted because of an unreleased hold from an online retailer they decided not to buy from, it creates an understandably poor brand experience.

Beyond customer dissatisfaction, orphaned authorizations can also attract scrutiny from card networks. Networks monitor authorization-to-capture ratios. If a merchant consistently generates high volumes of authorizations without corresponding captures or explicit reversals, it signals inefficiency and can sometimes trigger network fees for the misuse of the authorization system.

Authorization Reversals: A Tool for Payment Optimization

A highly effective way to address the orphaned authorization problem is the systemic use of authorization reversals. When an order is canceled, or when a final capture amount is lower than the initial authorized amount (like when an item is removed from an order before shipping), sending a reversal message to the network explicitly tells the issuer to drop the hold.

Implementing automated reversals demonstrates a high level of operational maturity. It requires tight synchronization between the order management system and the payment gateway, ensuring that any change in order status instantly cascades down to the payment layer.

Merchants who prioritize reversals often observe subtle but meaningful improvements in their overall payment ecosystem. By proactively clearing out unused holds, they reduce the likelihood of inadvertently causing checkout issues for their customers elsewhere, fostering long-term goodwill. Furthermore, keeping authorization-to-capture ratios healthy aligns operations smoothly with network expectations.

Exploring Estimated and Final Authorizations

The gap between approval and payment becomes even more layered in industries where the final cost is inherently variable. The tipping model in hospitality is the classic example, but modern delivery and grocery applications have introduced this dynamic to digital checkouts.

When a customer orders groceries for delivery, the initial authorization is an estimate. Items might be out of stock, substitutions might be required, or weighed items like produce might slightly alter the final total.

Merchants in these spaces often utilize specific network indicators to signal that the initial authorization is an estimate. When the final total is calculated, they submit the capture. If the final amount is slightly higher than the estimate, network rules typically allow the capture to proceed within a certain tolerance threshold.

However, if the final amount exceeds that threshold, the original authorization is no longer sufficient. The merchant must initiate an incremental authorization to cover the difference, or reverse the original and authorize the new, higher total. Each of these extra steps is another trip through the payment network, and another opportunity for a transaction declined response.

Managing these variable amounts requires sophisticated payment logic. The system must constantly weigh the potential for network fees against the risk of uncollected revenue, deciding whether an incremental authorization is the right path or if a slight over-authorization at the start is a safer operational choice.

What Happens When Capture Fails?

It is a common misconception that once an authorization is secured, the capture will seamlessly follow without issue. While it is highly probable that a capture will succeed if submitted within the correct timeframe, industry benchmarks for online card-not-present acceptance typically sit around 85-92% approval rate, and edge cases certainly exist where a capture attempt is rejected.

An account could be closed or frozen by the issuer due to suspected fraud between the time of authorization and capture. In certain instances, a system timeout or a formatting error in the capture request can cause the network to reject the message entirely.

When this happens, the merchant finds themselves in a complex position. They have likely already shipped the goods or provided the service based on the initial ‘Approved’ message. Recovering this revenue requires careful handling. Automatically attempting to force the capture without understanding why it failed can lead to further rejections and potential processing penalties.

Navigating the Retry Landscape

Encountering unexpected failures during the capture or re-authorization phase highlights the necessity of having a clear strategy for handling exceptions. When an initial attempt fails, merchants must decide if, when, and how to try again.

Blindly submitting the same transaction over and over is rarely effective. Issuers use sophisticated logic to detect and block what they perceive as erratic retry logic. Instead, thoughtful recovery strategies involve analyzing the specific decline codes, understanding whether a failure is a hard decline (like a closed account) or a soft decline (like a temporary system timeout), and timing subsequent attempts accordingly.

For example, addressing subscription payment issues often requires a highly nuanced approach to retries. If a recurring billing authorization fails on a Friday night, attempting it again immediately might yield the identical result. Waiting until Monday morning, or aligning the retry with common payroll cycles, can noticeably shift the outcome.

When navigating these complexities, platforms like SmartRetry provide a valuable layer of payment optimization by systematically handling intelligent retry logic of declined payment transactions. By analyzing issuer responses and network patterns, these tools help merchants recover revenue and improve transaction approval rates; some vendors claim authorization-rate boosts of up to 3% (Source) without requiring deep, in-house infrastructure overhauls.

Using contextual data to guide retry logic shifts the operational approach from hopeful persistence to calculated recovery, protecting the merchant’s relationship with both the issuer and the cardholder.

Aligning Operations, Product, and Finance

Addressing the silent gap between authorization and capture is not solely a technical exercise; it requires cross-functional alignment. Decisions made by the product team regarding user experience directly impact the payment flow. The way fulfillment centers operate dictates the timing of capture requests. And finance teams ultimately bear the burden of reconciling the discrepancies when authorizations and captures do not perfectly match up.

For a payment strategy to perform at its peak, these different departments must communicate effectively. Product managers designing a pre-order flow need to understand the limitations of authorization lifespans. Operations teams implementing split shipments must ensure those events sync with payment systems in real-time to trigger accurate partial captures.

When these systems operate in silos, the gap between approval and payment widens. A delayed shipment subtly turns into an expired authorization. A canceled order silently becomes a locked customer balance. By fostering a shared understanding of how funds actually move–and the delicate timing required to move them securely–organizations can build far more resilient revenue streams.

The Technical Nuance of Settlement

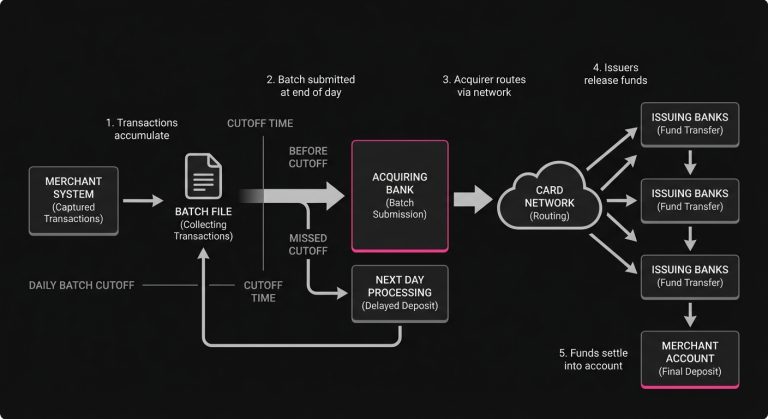

To fully appreciate the space between authorization and capture, it is helpful to look slightly beyond the capture itself, toward the settlement phase. When a merchant captures an authorization, they are not instantly receiving cash in their bank account. They are adding that specific transaction to a batch file.

At the end of the day, or at a predetermined interval, the merchant’s systems close this batch and send it to their acquiring bank. The acquirer then routes these captured transactions through the respective card network to the issuing banks. Only then does the actual transfer of funds begin, culminating in a deposit to the merchant’s corporate account.

This batching process adds another layer of timing complexity to the equation. If a capture request is submitted but misses the daily batch cutoff, settlement is delayed by another full processing cycle. For businesses managing tight cash flow, understanding the specific cutoff times of their payment processors and acquirers is a vital component of treasury management.

The capture is the trigger, but the batch settlement is the actual delivery vehicle. Mismanaging the timing of captures not only risks losing the original authorization but can also create cascading delays in working capital availability.

Moving From Approval to Actual Revenue

The architecture of modern payments is built on a series of handoffs, each with its own set of rules, timelines, and potential failure points. The separation of authorization and capture serves as a flexible framework designed to accommodate a complex commercial landscape.

However, that flexibility requires active, informed management. Treating an authorization as a final, immovable sale ignores the reality of how card networks operate. It leaves potential revenue vulnerable to expiring holds, unexpected fulfillment delays, and the subtle friction introduced by partial captures.

By deeply understanding the mechanics of this intermediate phase, merchants can implement more sophisticated payment flows. Utilizing targeted reversals, timing captures to align perfectly with fulfillment realities, and employing intelligent logic to retry failed payments all contribute to a tighter, more predictable revenue cycle.

The goal is to eliminate the costly assumptions that occur quietly in the background of a checkout. A green checkmark is a great start, but true payment optimization is about ensuring that every initial promise is smoothly, securely, and reliably translated into realized revenue.

Related

Still letting failed transactions slip through?

SmartRetry turns declines into approvals - automatically, intelligently, and without changing your payment provider.

Frequently asked questions about this topic

Share this article

Author

Roi Lagziel

Roi Lagziel is a payments engineer specializing in authorization optimization, retry strategies, and issuer-level behavior. His work focuses on building practical, data-driven systems that help payment teams reduce false declines and recover lost revenue.

Read all articles >More in Payment Approval Optimization:

April 16, 2026

Why Transaction Approval Rate Is Misleading and What Payment Teams Should Measure Instead

This article explains why blended approval rate can distort payment decisions and how teams can use recovery, cohort, and retry metrics to protect revenue and reduce false declines.

March 8, 2026

Why Virtual Card Payments Fail in Travel and How Payment Teams Improve Approval Rates

This article explains why travel virtual cards fail at hotels and what operators can do to recover approvals, cut manual intervention, and protect margins across issuing and acquiring.

March 8, 2026

The Invisible Logic of 3D Secure: How Payment Teams Balance Fraud, Friction, and Revenue

This article explains how payment teams can use 3D Secure, exemptions, and soft-decline handling to cut false declines, protect conversion, and improve recurring revenue performance.