Why Card Declines Happen and How Intelligent Recovery Protects Revenue

March 8, 2026

![]() 13 min

13 min

You spend months fine-tuning your acquisition strategy. You optimize the ad spend. You tweak the landing pages. You remove friction from the cart. Finally, the customer hits the buy button. Then, the transaction fails. It happens in milliseconds. A silent drop-off at the very bottom of your funnel. Most teams treat these payment issues as an unavoidable cost of doing business. They accept a certain percentage of failed payments as the weather. It becomes something you plan for but cannot change. But this perspective leaves a tremendous amount of revenue on the table. The reality of modern digital commerce is that payment declines are not always the end of the road. Often, they are just a miscommunication between complex systems. Understanding why they happen, and how to recover them, is one of the most effective levers for revenue growth. This isn’t just about saving a single sale. It is about preserving customer lifetime value, improving transaction approval rates, and fundamentally changing how your business handles the final inch of the checkout process. Let’s explore what actually happens when a card is declined and why fixing this leak matters far more than you might think.

The Mechanics Behind the Final Click

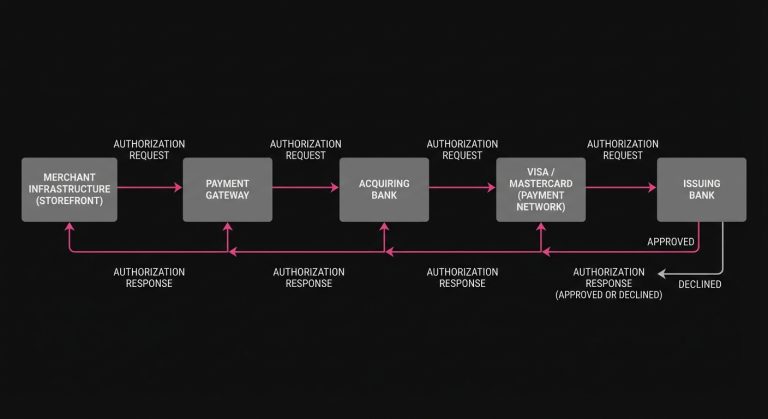

To understand why a transaction fails, it helps to map out the journey of a digital payment. When a customer clicks the checkout button, they set off a relay race that spans multiple global networks in the blink of an eye. The merchant’s platform packages the payment details and hands them off to a payment service provider or payment gateway. This gateway forwards the request to an acquiring bank, which then routes it through a major card network like Visa or Mastercard. Finally, the request lands at the issuer-the institution that actually gave the customer their credit or debit card.

At this final destination, the issuing bank must make a split-second decision. It evaluates the payment authorization request against a complex matrix of variables. Does the account have sufficient funds? Is the card reported lost or stolen? Does this purchase fit the cardholder’s historical spending patterns? Is the merchant operating in a high-risk category or geography?

If the issuer’s algorithms are satisfied, they send back an approval code, and the relay race reverses course to confirm the sale on the merchant’s screen. However, if any variable triggers a red flag, the issuer responds with a decline.

While this payment processing flow appears seamless to the consumer, it is actually highly fragmented. Each hop in the chain operates on different technology stacks, risk models, and legacy infrastructures. Because the entire process must complete in a fraction of a second, issuing banks often lean toward caution. When in doubt, their automated systems are programmed to decline the transaction to prevent potential fraud or liability. This structural bias toward caution is the root cause of many checkout issues, leaving merchants to bear the brunt of lost sales that otherwise should have been approved.

The Asymmetrical Risk of False Negatives

When an issuer evaluates a transaction, they are playing a game of risk management. If they approve a fraudulent transaction, they often absorb the financial liability and the operational headache of managing a chargeback. If they decline a legitimate transaction, they face very little immediate consequence. The merchant, however, loses the sale, the cost of acquiring that customer, and potentially the customer’s long-term loyalty.

This dynamic creates an asymmetrical risk environment. Issuers are naturally incentivized to tighten their risk filters, leading to a high volume of false negatives-valid transactions from good customers that are rejected by overly sensitive algorithms. Some estimates suggest 20-25% of transactions are flagged as fraud, even if legitimate, causing false declines.

The true cost of a transaction declined under these circumstances extends far beyond the immediate cart value. Consider the unit economics of a typical digital business. If your customer acquisition cost is fifty dollars and the initial product purchase is sixty dollars, a single lost sale might seem like a minor setback. But if that customer’s lifetime value is realistically closer to five hundred dollars, a false negative represents a significant compounding loss.

Furthermore, when a card declined message flashes on the screen, the customer rarely blames their bank. They tend to blame the merchant. The friction introduced by a failed checkout creates a moment of hesitation. Even if the customer has sufficient funds, being told their card was rejected feels frustrating and occasionally embarrassing. Many will simply close the tab and take their business to a competitor whose checkout process happens to route through an acquirer with a better relationship with that specific issuer. In fact, 40% of customers abandon purchases after a decline event.

Decoding the Issuer Response

When a payment authorization fails, the issuing bank does not send back a detailed explanation. Instead, it returns a cryptic, two-digit decline code. Understanding these codes is the first step toward building a mature payment recovery strategy, because treating all declines equally is a remarkably inefficient way to run a payment operation. See our Payment Decline Codes page for reference.

Declines generally fall into two distinct categories: hard declines and soft declines.

A hard decline indicates a permanent, unresolvable issue with the payment method. Examples include codes indicating a lost or stolen card, a closed account, or a fraudulent transaction. In these scenarios, the relationship with that specific card number is effectively dead. Attempting to retry a hard decline is not just a waste of time; it actively damages your merchant standing with the card networks.

Soft declines, on the other hand, represent temporary conditions. The account is valid, the card is active, but something about the specific context of the transaction caused the issuer to reject it. The most common soft decline is “Insufficient Funds.” 47% of declines worldwide are due to insufficient funds. Another frequent, yet frustrating, issuer response is Code 05: “Do Not Honor.”

“Do Not Honor” is the ultimate black box of payment processing. Because many issuing banks operate on legacy mainframes built decades ago, they often lack the granular codes needed to describe modern digital risk triggers. When their system encounters a scenario it doesn’t quite understand-perhaps a sudden cross-border purchase, an unusual velocity of transactions, or simply a temporary timeout in a downstream database-it defaults to a generic “Do Not Honor” code.

For the merchant, a soft decline is an opportunity. Because the issue is temporary, the transaction has a high probability of succeeding if it is handled correctly. However, how a merchant chooses to handle that temporary failure makes all the difference.

The Hidden Dangers of the Brute Force Approach

Historically, merchants who understood that soft declines were temporary adopted a very straightforward strategy: if a payment fails, just try it again. If it fails a second time, try it again tomorrow.

This brute force approach to retry failed payments used to be a common industry practice, largely because it required very little engineering effort. You simply wrote a script to loop the transaction until it went through or the customer canceled. Today, this approach is not only ineffective, but it is also actively penalized by the payment networks.

Card networks like Visa and Mastercard maintain strict rules governing how and when merchants can retry a declined card. They monitor the ratio of successful authorizations to failed authorizations. If a merchant blindly hammers the network with repeated retry attempts for transactions that have already been declined, the networks take notice.

Excessive retries clog the network infrastructure and incur unnecessary processing costs. To combat this, networks have introduced complex retry frameworks and Merchant Advice Codes that dictate whether a transaction can be retried and how many days a merchant must wait before attempting it again. Violating these rules can result in escalating per-transaction fines.

More importantly, aggressive retries degrade the merchant’s overall authorization rate. When an issuing bank sees a merchant repeatedly submitting the same failed transaction, it interprets that behavior as a sign of an unsophisticated or potentially malicious operation. The issuer’s risk engine begins to associate the merchant’s identifier with high-risk activity. Consequently, the issuer may start declining even perfectly valid, first-time transactions from that merchant out of an abundance of caution.

In short, trying to recover revenue through blind repetition often ends up causing more payment failures across the board. The brute force approach sacrifices long-term infrastructure health for short-term, low-probability gains.

Shifting Toward Intelligent Payment Optimization

If ignoring declines leaves money on the table, and blindly retrying them damages your merchant reputation, the only sustainable path forward is to introduce logic and context into the recovery process. This is the essence of payment optimization.

Intelligent recovery involves treating each failed transaction as a unique data puzzle. Instead of asking, “Should we retry this?”, the better question is, “When and how should we retry this to maximize the probability of an approval?”

The variables that influence an issuer’s decision to approve a soft decline are numerous and constantly shifting. Timing is one of the most critical factors. A card that returns an “Insufficient Funds” code on a Tuesday afternoon is highly unlikely to be approved if retried on Wednesday morning. However, if that same transaction is held and strategically retried in the early hours of Friday morning-aligning with typical global payroll cycles when direct deposits clear-the likelihood of a successful payment authorization increases dramatically.

Time of day matters just as much as the day of the week. Many large banks run their batch processing and system maintenance in the middle of the night. A transaction that is declined at 2:00 AM due to a generic system timeout may easily pass if retried at 10:00 AM.

Beyond timing, the specific characteristics of the card itself provide valuable context. The first six to eight digits of a credit card, known as the BIN, can identify not just the issuing bank, but the specific type of card-whether it is a premium rewards credit card, a corporate purchasing card, or a prepaid debit card. Each of these card types behaves differently and is subject to different risk thresholds.

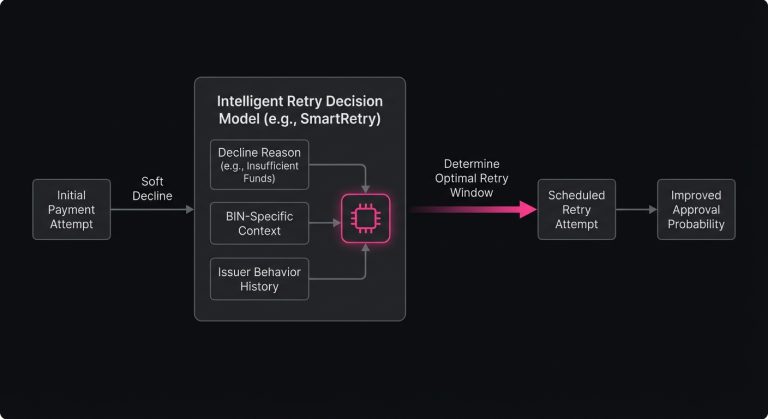

Managing these variables manually is nearly impossible at scale. This is why many growing businesses rely on automated solutions. A platform focused on payment optimization and intelligent retries of declined payment transactions, such as SmartRetry, can help merchants recover revenue and improve transaction approval rates by applying data-driven logic to these decisions. By analyzing historical authorization patterns across thousands of different issuers and BINs, these systems can predict the exact optimal window to attempt a retry, keeping network compliance high while maximizing recovery. On average, 60-70% of card declines are recoverable through follow-up or retries, and automatic payment retries can recover 70% of failed payments.

The Compounding Math of Subscription Recovery

While optimizing the checkout experience is crucial for e-commerce and one-time purchases, the stakes are arguably much higher for recurring revenue models. For SaaS companies, media streaming platforms, and subscription box services, subscription payment issues represent a unique existential threat.

In a subscription model, customer retention is the entire foundation of profitability. When a recurring charge fails, it is rarely because the customer actively decided to cancel their service. Often, they simply received a new card in the mail, their old card expired, or they temporarily hit a credit limit. This scenario is known as involuntary churn.

Involuntary churn is particularly insidious because it quietly erodes the compounding nature of subscription revenue. Imagine a software company with a seemingly manageable involuntary churn rate of two percent per month due to failed payments. In a single month, losing two percent of the user base might not trigger alarm bells in the boardroom. But over the course of a year, that two percent monthly leak compounds. By year-end, the company has effectively lost a massive segment of its active customer base-not because the product was lacking, but because the payment plumbing failed.

Addressing these specific payment failures requires a nuanced approach to payment recovery. Because you are dealing with an existing customer relationship rather than a first-time buyer, you have more leeway and more data to work with. Network tools like Account Updater services can automatically fetch new expiration dates or updated card numbers directly from the issuers before a charge is even attempted, circumventing the decline entirely.

When a decline does happen, intelligent retry logic becomes the silent retention engine of the business. By carefully managing the cadence of retries over a billing cycle, and coupling those retries with well-timed, polite customer outreach (dunning campaigns), businesses can salvage a significant portion of these accounts. Recovering a subscription does not just secure that month’s revenue; it secures the revenue for every subsequent month that the customer remains active.

Moving Beyond Operational Plumbing

For a long time, the mechanics of routing transactions and handling decline codes were viewed strictly as back-office operational tasks. It was considered the plumbing of the internet-necessary, deeply unglamorous, and rarely discussed in strategic growth meetings. Payment teams were tasked primarily with keeping processing fees low and ensuring the gateway didn’t go down.

But as digital markets have matured and customer acquisition costs have climbed across almost every industry, the perspective on payments has shifted. Growth leaders now recognize that optimizing the bottom of the funnel is often more cost-effective than pouring more money into the top.

Every percentage point increase in your transaction approval rate is pure, unadulterated top-line revenue that flows almost entirely to the bottom line. You have already paid for the marketing, you have already built the product, and the customer has already decided they want to buy it. The only thing standing between your business and recognized revenue is a better conversation with an issuing bank.

To reduce payment declines requires moving away from a passive acceptance of failure. It demands a proactive stance. It requires understanding that an issuer’s response is not a final judgment, but a data point in an ongoing negotiation. It involves respecting network rules, leveraging contextual data, and applying intelligent sequencing to every single transaction that falls out of the happy path.

Building a Resilient Revenue Strategy

Ultimately, the goal of optimizing your payment flows is to build resilience into your revenue engine. The digital economy is probabilistic. Systems will experience downtime. Issuing banks will adjust their risk models in response to global fraud trends. Customers will occasionally forget to transfer funds to their checking accounts before their subscription renews.

You cannot control the weather, but you can build a better roof.

By treating payment issues not as frustrating anomalies, but as predictable, manageable events, you change the financial trajectory of your business. You stop punishing good customers for the rigidities of legacy banking infrastructure. You protect your merchant reputation with the card networks, ensuring that your first-time authorizations remain smooth and unobstructed.

The leak in your funnel is real, and the silent drop-off of failed transactions costs far more than the sum of the lost carts. It costs you growth, momentum, and the hard-won trust of your user base. Fixing that leak does not require reinventing your product or overhauling your marketing strategy. It simply requires a commitment to intelligent, deliberate payment optimization-ensuring that when your customer is ready to pay, your infrastructure is smart enough to listen, adapt, and successfully capture the value you’ve worked so hard to create.

Still letting failed transactions slip through?

SmartRetry turns declines into approvals - automatically, intelligently, and without changing your payment provider.

Frequently asked questions about this topic

Share this article

Author

Roi Lagziel

Roi Lagziel is a payments engineer specializing in authorization optimization, retry strategies, and issuer-level behavior. His work focuses on building practical, data-driven systems that help payment teams reduce false declines and recover lost revenue.

Read all articles >More in Smart Payment Retry Strategies:

March 8, 2026

Decoding Hard and Soft Declines: A Practical Guide to Smarter Payment Recovery

This guide explains how to classify payment declines, respond with the right retry strategy, and reduce unnecessary churn, fees, and approval-rate drag across checkout and recurring billing.

March 8, 2026

The Boomerang Effect: Why Brute-Force Retries Cost More Than They Recover

This article explains why blind payment retries erode issuer trust, add network costs, and hurt future approvals, and how smarter decline management can improve recovery and authorization performance.

March 8, 2026

The Art of the Second Chance: Decoding Soft vs. Hard Declines

This article explains how to separate recoverable declines from permanent failures, optimize retry logic, and reduce involuntary churn to protect revenue and improve approval performance.