The First 90 Days of Payment Management: How to Find Revenue Leaks and Improve Authorization Rates

March 8, 2026

![]() 11 min

11 min

The First 90 Days: Navigating the Chaos and Opportunity of Payment Management

Stepping into a new payment management role is rarely quiet. You inherit a system that is already running. Transactions are flowing. Revenue is moving. Yet beneath the surface, there is almost always friction. Legacy code dictates routing decisions made years ago. Gateways are returning errors that no one on the current team fully understands. It can feel like walking into a crowded control room where half the dials are labeled in a language you only partially recognize. But this initial chaos is actually your greatest advantage. The first 90 days are not just about keeping the lights on. They present a unique window to map the terrain, question long-held assumptions, and find the hidden revenue levers that others have normalized or ignored. If you want to meaningfully improve your approval rate, the work starts with dismantling the black box of your current setup.

The reality of payment operations is that nothing is entirely static. Issuers update their risk models, card networks introduce new mandates, and consumer spending habits shift. What worked a year ago might be slowly bleeding revenue today. In this environment, your mandate is to transition the payments function from a passive cost center into an active engine for growth. This requires a methodical approach to discovery, analysis, and execution.

The First Thirty Days: Mapping the Unseen Terrain

Your first month is primarily about taking inventory. It is tempting to jump straight into making changes, adjusting routing rules, or turning on new gateway features, but doing so without a clear map of your current architecture is a fast way to introduce new points of failure.

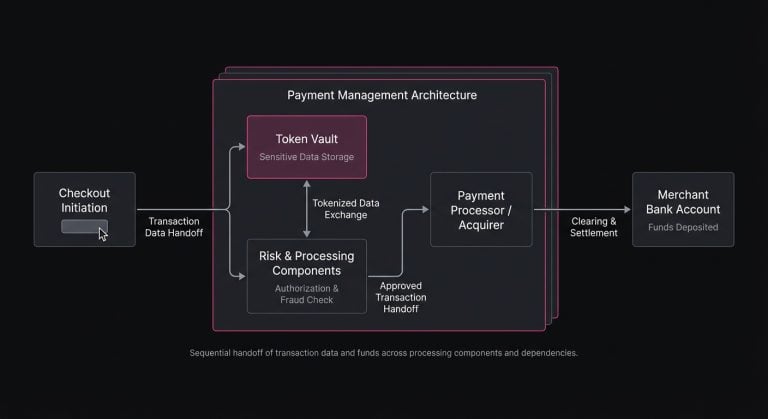

To start, you need to map the entire payment processing flow end-to-end. This means tracing the journey of a transaction from the moment a customer hits the checkout button to the final settlement in your merchant bank account. You will likely uncover a web of third-party dependencies, token vaults, fraud decisioning engines, and legacy integrations.

Establishing the Baseline

Before you can improve anything, you must establish a baseline. Many teams believe they know their approval rates, but these metrics are often skewed by how different platforms report data. Does your gateway calculate authorization rates based on gross attempts or unique orders? Does it include transactions blocked by your internal fraud filters, or only those that actually reached the issuing bank?

During this phase, experienced operators dig into the raw data. Look for patterns in the noise. Are you seeing authorization drops during specific times of the day? Do certain card networks perform significantly worse than others? Are international transactions failing at a disproportionate rate compared to domestic ones? Documenting these anomalies gives you a targeted hit list for the months ahead.

Identifying the Silent Leaks

Not all payment issues generate loud alarms. Some of the most costly inefficiencies are entirely silent. For instance, you might discover that a significant portion of your recurring transactions are being flagged as Initial rather than Subsequent, causing issuers to evaluate them with an unnecessarily high degree of scrutiny. You might find that your system is blindly passing poorly formatted billing addresses, triggering minor risk flags that cumulatively drag down your success rates. Mapping these quiet leaks is the foundation of your optimization strategy.

Decoding the Anatomy of a Decline

By your second month, the focus shifts from mapping the architecture to diagnosing the failures. In the world of payments, a transaction declined is rarely just a closed door; it is a highly specific diagnostic payload. How you interpret and react to this payload determines how much revenue you can ultimately recover.

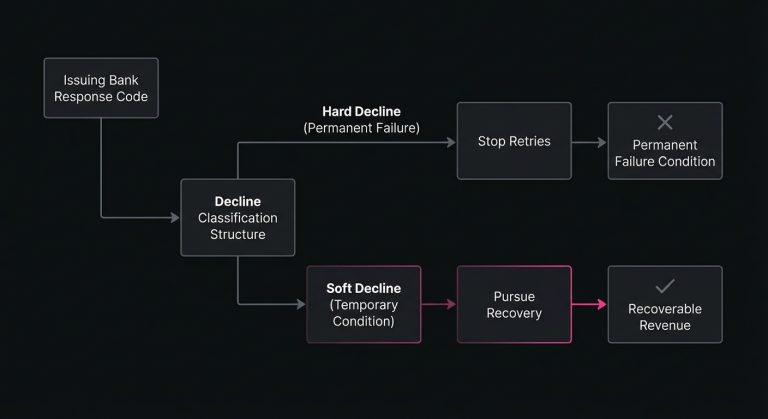

Every time an authorization request is denied, the issuing bank sends back a response code. Unfortunately, despite the existence of standard ISO messaging frameworks, different banks interpret and utilize these codes differently. Understanding the nuances of the payment decline codes response is a critical skill for any payment professional.

The Spectrum of Refusals

Declines generally fall into two broad categories: hard declines and soft declines. Hard declines represent a permanent barrier. The account is closed, the card is reported lost or stolen, or the cardholder is deceased. In these scenarios, the relationship with that specific payment credential is over. Retrying a hard decline is not just futile; it actively damages your merchant trust profile with the networks and can lead to unnecessary processing fees.

Soft declines, on the other hand, represent a temporary condition. The account might have insufficient funds at the exact moment the charge was attempted, the transaction might have tripped a temporary velocity limit, or the issuer’s internal systems might simply be experiencing a momentary timeout. When you see a card declined for a soft reason, you are looking at recoverable revenue.

The Mystery of Generic Declines

The most frustrating code you will encounter is the generic “decline code” response. Issuers frequently use this as a catch-all category when they decline a transaction based on their internal, proprietary fraud models but do not want to expose the exact reason. It tells you nothing about what actually went wrong.

Was the transaction unusually large? Did the geolocation of the IP address mismatch the billing zip code? Is the issuer overly sensitive to the specific merchant category codes you are operating under? Unpacking generic declines requires looking at the surrounding context. By cross-referencing these failures against time of day, average order value, and card type (debit, credit, prepaid, corporate), you can begin to reverse-engineer the issuer’s logic and adjust your transaction payload accordingly.

Days 31 to 60: Moving from Observation to Optimization

Armed with a clear map of your system and a deep understanding of your decline code taxonomy, the middle of your first 90 days is where you begin to actively intervene. This is the era of payment optimization, where small, calculated adjustments to the data you send can yield massive returns in authorized revenue.

Enhancing the Transaction Payload

Issuers are fundamentally risk-averse algorithms. Their primary goal is to protect their account holders and their own liability. Your goal is to make your transaction look as safe, legitimate, and predictable as possible.

Often, you can significantly reduce payment declines simply by cleaning up the data you send in the authorization request. This includes ensuring that Address Verification System (AVS) checks and Card Verification Values (CVV) are handled correctly. But optimization goes far beyond basic data hygiene.

The Shift to Network Tokenization

One of the most powerful levers for improving authorization rates today is the adoption of network tokenization. Unlike traditional gateway tokens, which are proprietary to your specific payment service provider, network tokens are issued directly by the card schemes (Visa, Mastercard, etc.).

When you process a transaction using a network token, the issuer inherently trusts the request more because the token is linked directly to the underlying account at the network level. Network tokens also update automatically when a cardholder receives a new physical card, bridging the gap that often causes recurring billing failures. Transitioning a portion of your vaulted cards to network tokens requires engineering effort, but it is one of the highest-yield projects a payment team can undertake, especially as tokenization reached 50% of digital transactions in 2025 (Source).

Balancing Friction and Conversion

Optimization is a delicate balancing act. It is entirely possible to achieve a near-perfect approval rate by implementing draconian fraud filters and mandating 3D Secure challenges on every single checkout. However, doing so introduces immense friction for the customer, resulting in abandoned carts and a net loss in overall revenue.

The art of optimization lies in applying the right amount of friction to the right transactions. Utilizing exemptions for low-risk transactions or routing specific high-risk profiles through step-up authentication allows you to satisfy issuer risk requirements without punishing your legitimate customers, even as 3D Secure adoption in US e-commerce is projected to surpass 50% by Q4 2026.

The Mechanics of Intelligent Retries

No matter how refined your authorization strategy becomes, failures are inevitable. A perfectly formatted, entirely legitimate transaction will still fail if the cardholder hasn’t been paid yet and their debit account is empty. This brings us to the critical phase of payment recovery: figuring out what to do after the initial “no.”

For a long time, the industry standard for handling failures was brute force. Systems were programmed to automatically try the card again the next day, often at midnight, and repeat the process until the payment went through or the customer churned.

Why Brute Force Fails

Today, aggressive, automated retries are a liability. Card networks actively monitor the frequency and volume of retries. If you hammer an issuer with repeated requests for an insufficient funds decline, you incur scheme fees for excessive authorization attempts. More importantly, the issuer’s risk engine will flag your merchant ID as reckless, potentially lowering your baseline approval rate across all transactions. You cannot bully an issuer into approving a payment.

Crafting a Strategic Recovery Flow

To successfully retry failed payments, you must transition from a schedule-based approach to an intelligence-based approach. The timing of a retry should be dictated by the specific context of the decline.

If a transaction fails due to insufficient funds on a Wednesday, immediately retrying it on Thursday morning is unlikely to yield a different result. However, retrying it on Friday morning-when bi-weekly payrolls typically clear-dramatically increases the probability of success. Similarly, a temporary network timeout might warrant an immediate retry within a few hours, while a suspected fraud decline might require the customer to actively intervene and verify their identity.

Platforms like SmartRetry focus on payment optimization and intelligent retries of declined payment transactions, helping merchants navigate these probabilistic variables to recover revenue and improve transaction authorization rates. By leveraging data around issuer behavior, decline codes, and optimal time windows, these systems replace guesswork with calculated, high-probability recovery flows, ensuring that you recapture lost revenue without alienating the issuing banks or incurring penalty fees.

Days 61 to 90 and Beyond: Operationalizing the Revenue Engine

As you enter the final month of your initial 90-day sprint, the foundational work is largely in place. You have mapped the architecture, diagnosed the decline data, optimized the frontend payload, and implemented intelligent recovery mechanisms. The challenge now is to operationalize these strategies so they run continuously, adapt to new variables, and provide clear visibility to the rest of the business.

Tackling Recurring Revenue Leaks

If your business operates on a recurring revenue model, managing subscription payment issues will be a constant operational focus. Involuntary churn-where a customer loses access to your service simply because their payment method failed-is one of the most frustrating forms of revenue leakage.

Addressing this requires tight coordination between your payment retry logic and your customer-facing dunning strategies. A soft decline should trigger an invisible, backend retry schedule, buying time to resolve the issue without alarming the customer. However, if the system identifies a hard decline, or if the intelligent retries exhaust their optimal windows, the process must gracefully hand off to an email or SMS sequence, prompting the user to update their billing information.

Building the Feedback Loop

Payment management is not a set-it-and-forget-it discipline. The global financial ecosystem shifts constantly. A change in a major issuer’s fraud algorithm can cause a sudden, unannounced dip in your approval rates. A new scheme mandate from Visa or Mastercard can alter how specific transaction flags are treated.

To stay ahead, you need to build robust monitoring and alerting systems. Create dashboards that track approval rates not just in aggregate, but segmented by gateway, country, card type, and specific decline code. Set threshold alerts so your team is notified the moment a specific routing path experiences a spike in generic declines or gateway timeouts.

Fostering a Culture of Curiosity

Perhaps the most important outcome of your first 90 days is the cultural shift you create within your organization. Payments should no longer be viewed merely as the plumbing that connects the checkout button to the bank. It is a highly dynamic, strategic lever that directly impacts the bottom line.

When you sit down with product managers, marketing teams, and finance leaders, you can now articulate exactly how payment friction impacts customer acquisition costs, or how saving a percentage of failed transactions compounds over the lifetime value of a cohort.

By the end of your first quarter, the initial chaos will have settled into clarity. The opaque systems you inherited will now have mapped pathways, monitored metrics, and intentional strategies guiding them. The work of optimization is never truly finished, but the foundation you build in these first 90 days transforms payment management from a reactive exercise in putting out fires into a proactive, sustained mechanism for driving business growth.

Still letting failed transactions slip through?

SmartRetry turns declines into approvals - automatically, intelligently, and without changing your payment provider.

Frequently asked questions about this topic

Share this article

Author

Roi Lagziel

Roi Lagziel is a payments engineer specializing in authorization optimization, retry strategies, and issuer-level behavior. His work focuses on building practical, data-driven systems that help payment teams reduce false declines and recover lost revenue.

Read all articles >More in Payment Approval Optimization:

April 16, 2026

Why Transaction Approval Rate Is Misleading and What Payment Teams Should Measure Instead

This article explains why blended approval rate can distort payment decisions and how teams can use recovery, cohort, and retry metrics to protect revenue and reduce false declines.

March 8, 2026

Why Virtual Card Payments Fail in Travel and How Payment Teams Improve Approval Rates

This article explains why travel virtual cards fail at hotels and what operators can do to recover approvals, cut manual intervention, and protect margins across issuing and acquiring.

March 8, 2026

The Invisible Logic of 3D Secure: How Payment Teams Balance Fraud, Friction, and Revenue

This article explains how payment teams can use 3D Secure, exemptions, and soft-decline handling to cut false declines, protect conversion, and improve recurring revenue performance.