The Art of the Second Chance: Decoding Soft vs. Hard Declines

March 8, 2026

![]() 12 min

12 min

The Art of the Second Chance: Decoding Soft vs. Hard Declines

A payment fails. A customer sighs. Revenue slips away. For most businesses, a declined transaction feels like a definitive end to the buyer journey. You did the hard work of acquiring the user, guiding them through the funnel, and securing their intent to purchase. Then, you hit an invisible wall at the final step. When you see a card declined at checkout, it is easy to assume the door is permanently closed. In reality, the modern payment processing flow is a highly nuanced, probabilistic ecosystem. A rejection often means “not right now” rather than “never.” Unlocking the revenue trapped behind these payment issues requires moving beyond simple frustration. It demands a sophisticated understanding of why transactions fail and how to efficiently recover them. This is the realm of The Art of the Second Chance: Decoding Soft vs. Hard Declines, a discipline where parsing the exact nature of an issuer response can mean the difference between losing a customer and securing long-term revenue.

The Taxonomy of a Decline

To the untrained eye, a decline is simply a failed transaction. The money did not move, the goods cannot be shipped, or the software access must be revoked. But behind the scenes, every time an authorization request is sent through the card networks, it returns with a specific response code. These codes act as a diagnostic language, offering clues about the health of the transaction and the disposition of the cardholder’s account.

Experienced payment professionals generally divide these responses into two broad categories: hard declines and soft declines. Understanding the distinction between the two is the foundational step in building any meaningful transaction recovery strategy. Treating all declines equally is a quick way to inflate your processing costs, frustrate your customers, and inadvertently trigger the wrath of the card networks.

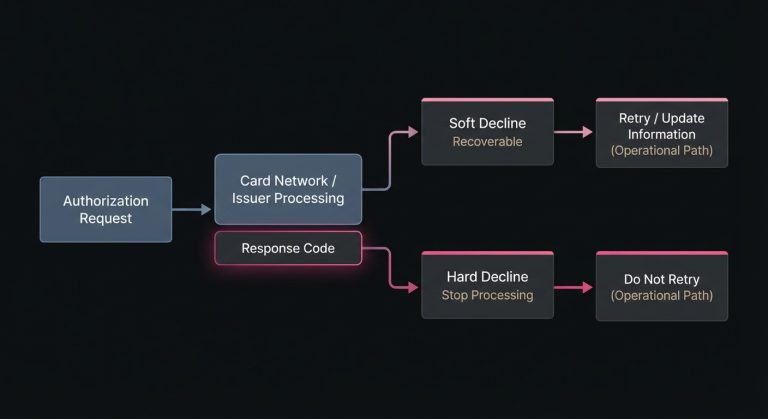

A decline is fundamentally a conversation between the acquiring bank (representing the merchant) and the issuing bank (representing the cardholder). The issuer is evaluating a complex matrix of risk, available credit, account status, and behavioral history in a matter of milliseconds. When they return a decline, they are communicating a specific boundary condition. The merchant’s job is to figure out whether that boundary is a temporary hurdle or a permanent brick wall.

When No Truly Means No: Anatomy of a Hard Decline

A hard decline occurs when the issuing bank rejects a transaction for a systemic, unresolvable reason. These are the brick walls of the payment ecosystem. The account might be closed, the card might be reported lost or stolen, or the account number provided might simply be invalid.

Common response codes that fall into this category include 04 (Pick Up Card), 41 (Authorization Code 41), 43 (Stolen Card), and 14 (Invalid Card Number). When an issuer returns one of these codes, they are sending a clear and unambiguous message: this specific payment method is dead. No amount of waiting, hoping, or retrying will magically resurrect a closed bank account or validate a compromised card.

The operational rule for hard declines is straightforward but often ignored: stop. Attempting to process these cards again is not just an exercise in futility; it is an active operational hazard. Card networks monitor merchant retry behavior closely. If you repeatedly hammer the network with authorization requests for cards that have already been flagged as lost or stolen, you signal to the ecosystem that your payment operations are either negligent or potentially fraudulent. This can lead to authorization abuse fees, degraded trust with issuers, and ultimately, a lower overall transaction approval rate across your entire merchant account.

The Gray Area: Unpacking Soft Declines

If hard declines are brick walls, soft declines are traffic jams. They represent temporary environmental or circumstantial friction rather than a permanent failure. A soft decline indicates that the card is valid and the account is open, but the transaction cannot be completed under the current conditions.

The most recognized soft decline is Code 51 (Decline Code 51). This simply means the cardholder does not currently have the available balance or credit to cover the transaction amount. Other common soft declines relate to velocity or environmental limits, such as Code 61 (Exceeds Withdrawal Limit) or Code 65 (Exceeds Frequency Limit). These often happen when a customer makes an unusually high number of purchases in a short window, triggering a temporary lock by the issuer’s risk model.

Soft declines are the prime real estate for payment recovery. Because the underlying payment instrument is theoretically sound, a well-timed subsequent attempt has a reasonable probability of success. Around 80% to 90% of all declines are soft declines (Source). A customer who lacks funds on a Tuesday might get paid on a Friday. A velocity limit that blocks a transaction at 11:00 PM might reset at midnight. Navigating these temporal nuances is where payment operations teams earn their keep.

The Mystery of “Do Not Honor”

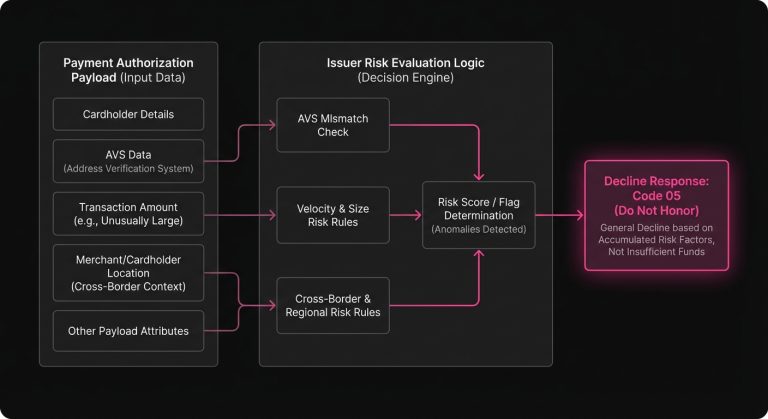

No discussion of soft declines is complete without addressing the infamous Code 05 (How to Recover 05 Do Not Honor Declines With Smarter Payment Retries). It is the catch-all response, the polite shrug of the payment world. Issuers typically use Code 05 when a transaction violates a risk parameter or internal business rule, but they either cannot or choose not to pass a more specific reason back through the network.

Treating a Do Not Honor code like a simple lack of funds is a bit like treating a check engine light by just adding more gas. It requires a more nuanced touch. Often, a Code 05 is triggered by an anomaly in the payment authorization payload-perhaps a mismatch in the Address Verification System (AVS), an unusually large transaction size for that specific cardholder, or a cross-border transaction that trips a geographic fraud filter. While Code 05 is generally treated as a soft decline, blindly retrying it without altering the context of the transaction often yields diminishing returns.

Decoding the Issuer’s Black Box

To effectively reduce payment declines, it helps to look at the transaction through the eyes of the issuing bank. Issuers are inherently risk-averse. Every time they approve an authorization, they are effectively extending a micro-loan to the cardholder and assuming liability for the transaction. If the transaction turns out to be fraudulent, or if the customer defaults, the issuer often bears a financial burden.

Consequently, issuers employ highly sophisticated, machine-learning-driven risk models that evaluate dozens of data points in real time. They look at the merchant’s category code (MCC), the time of day, the IP distance from the cardholder’s billing zip code, and the historical purchasing behavior of the user. If an issuer’s model senses too much risk, or if the transaction simply looks anomalous, they will default to a decline.

Understanding this dynamic explains why some perfectly legitimate transactions fail. It also highlights the importance of data hygiene. The cleaner and more comprehensive the data payload you send during the initial payment authorization, the more comfortable the issuer feels approving it. Simple hygiene practices, like passing accurate CVV and AVS data, or ensuring your merchant descriptors are clear and recognizable to the cardholder, can noticeably reduce friction and improve approval probabilities.

Retry Strategies: Brute Force vs. Precision

When faced with a soft decline, the natural instinct is to simply try the card again. Historically, many merchants employed a “brute force” approach, automatically attempting to charge a failed card every 24 hours until the payment went through or the billing cycle ended.

Today, this naive approach is not only ineffective; it is actively penalized. Card networks like Visa and Mastercard have strict mandates regarding how and when merchants can retry failed payments. For instance, attempting to retry a single transaction more than a specified number of times within a 30-day window can trigger significant authorization abuse fines. Furthermore, issuers track merchant retry behavior. If they see a merchant frantically retrying the same declined card day after day, their risk models may begin to automatically suppress approvals for that merchant out of an abundance of caution.

A modern retry strategy must replace brute force with precision. It requires categorizing the exact issuer response and applying a tailored logic to the subsequent attempt. This means dynamically adjusting the cadence, timing, and conditions of the retry based on the specific context of the failure.

Timing is Everything: The Anatomy of a Smart Retry

Intelligent retries are built on the premise that timing and context dictate success. If a transaction fails due to insufficient funds, retrying it 12 hours later is generally a waste of time and authorization fees. Instead, savvy payment teams map their retries to common behavioral and economic cycles.

For example, scheduling a retry for a Friday-the most common payday-or the 1st and 15th of the month tends to yield much higher recovery rates for insufficient fund declines. Retry success rates above 25% are a common target for retried soft declines (Source). Similarly, understanding the time zones of your customers can prevent you from triggering a fraud filter by attempting a retry at 3:00 AM local time.

This level of precision is especially critical when dealing with subscription payment issues. In a recurring billing model, a failed payment does not just mean a lost sale; it means involuntary churn and the loss of all future customer lifetime value. By carefully spacing out retries and aligning them with periods of high liquidity, subscription businesses can passively recover a significant portion of their recurring revenue without ever needing to contact the customer.

Proactive Measures: Fixing the Leak Before It Happens

While optimizing the retry cadence is vital, the most effective way to handle a decline is to prevent it from occurring in the first place. The payments industry has developed several powerful tools designed to maintain the health of stored payment credentials proactively.

Account Updater services (offered by the major card networks) allow merchants to query the network for updated card details before processing a recurring charge. If a customer’s card has expired, or if they were issued a new card due to a lost wallet, the Account Updater service can seamlessly swap the old PAN (Primary Account Number) and expiration date for the new ones behind the scenes.

Similarly, the adoption of Network Tokens is fundamentally changing how recurring payments are handled. Unlike a standard primary account number, a network token is a unique digital identifier tied specifically to the merchant and the device. Because these tokens are managed directly by the card networks and the issuers, they are inherently more trusted and automatically update when the underlying card details change. Transactions processed via network tokens generally experience fewer checkout issues and enjoy a noticeable uplift in authorization rates compared to standard PAN transactions.

Orchestrating the Recovery Flow

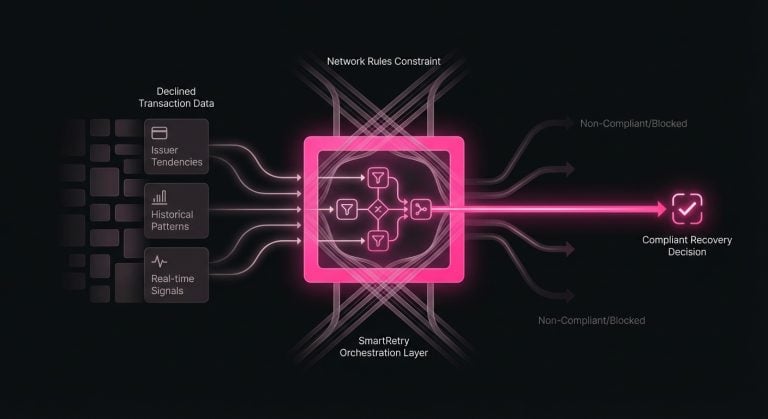

Managing this intricate web of response codes, network rules, account updaters, and dynamic retry schedules requires a level of operational orchestration that is difficult to build from scratch. This is exactly where specialized platforms come into the picture. SmartRetry, for example, functions as an intelligent layer that evaluates the nuanced data of a declined transaction to orchestrate the most effective recovery path. By focusing on The Art of the Second Chance: Decoding Soft vs. Hard Declines and intelligent retries, platforms like this help merchants recover revenue and improve transaction approval rates without running afoul of network rules. Instead of guessing when a customer might have funds available, the system relies on historical patterns, issuer tendencies, and real-time signals to turn a probable failure into a seamless success.

The Hidden Economics of Payment Recovery

To fully appreciate the value of decoding soft and hard declines, one must look at the math underlying the customer lifecycle. In many organizations, a failed payment is viewed purely as a payment operations problem. In reality, it is a customer acquisition and growth problem in disguise.

Consider the cost of acquiring a new customer (CAC). Marketing teams spend heavily on advertising, funnel optimization, and sales efforts to bring a user to the point of purchase. If that user churns involuntarily due to a poorly handled soft decline, the business has not only lost that specific transaction but has also wasted the entire acquisition cost.

The economics become even more profound in subscription models. A slight improvement in the transaction approval rate compounds over time. If you can recover an additional 2% of failed subscription renewals through intelligent retries, that 2% continues to pay you every subsequent month they remain active. Over the course of a year, the compounding effect of saving those customer relationships can drastically improve the overall lifetime value (LTV) of the cohort and add significant margin to the bottom line. Payment recovery is rarely just about saving the immediate dollar; it is about preserving the downstream revenue that the customer represents. Businesses worldwide lose an estimated $4.6 trillion in potential revenue every year due to failed payment transactions (Source).

Moving from Friction to Flow

The payments landscape is shifting from a reactive model to a proactive, data-driven discipline. The days of treating all declines as permanent rejections or relying on simplistic daily retries are fading. Modern merchants recognize that the space between an initial decline and a final failure is rich with opportunity.

By taking the time to decode the difference between hard and soft declines, respecting the risk models of the issuing banks, and applying intelligent, context-aware recovery strategies, businesses can reclaim a substantial portion of their revenue. It requires a blend of technical understanding, operational discipline, and a willingness to view payment failures not as dead ends, but as valuable data points guiding the way toward a second chance. Ultimately, mastering this dynamic turns the checkout experience from a point of friction into a resilient engine for sustainable growth.

Still letting failed transactions slip through?

SmartRetry turns declines into approvals - automatically, intelligently, and without changing your payment provider.

Frequently asked questions about this topic

Share this article

Author

Roi Lagziel

Roi Lagziel is a payments engineer specializing in authorization optimization, retry strategies, and issuer-level behavior. His work focuses on building practical, data-driven systems that help payment teams reduce false declines and recover lost revenue.

Read all articles >More in Smart Payment Retry Strategies:

March 8, 2026

Decoding Hard and Soft Declines: A Practical Guide to Smarter Payment Recovery

This guide explains how to classify payment declines, respond with the right retry strategy, and reduce unnecessary churn, fees, and approval-rate drag across checkout and recurring billing.

March 8, 2026

The Boomerang Effect: Why Brute-Force Retries Cost More Than They Recover

This article explains why blind payment retries erode issuer trust, add network costs, and hurt future approvals, and how smarter decline management can improve recovery and authorization performance.

March 8, 2026

How to Recover 05 Do Not Honor Declines With Smarter Payment Retries

This article explains why 05 Do Not Honor is usually a soft decline and how operators can recover revenue through better retry timing, routing, and data enrichment to reduce false declines and churn.