Decoding Hard and Soft Declines: A Practical Guide to Smarter Payment Recovery

March 8, 2026

![]() 12 min

12 min

Decoding the Hidden Language of Network Responses: A Practical Guide to Hard and Soft Declines

Every time a customer hits the buy button, an invisible apparatus springs into action. Data flies across the globe as servers talk to servers and algorithms assess risk in milliseconds. Usually, it works beautifully. But often enough, the process stops cold. You get a notification that a transaction declined, frustrating the customer and taking a minor hit to your revenue. Left staring at a vague two-digit code, you wonder what actually went wrong. Understanding payment failures is rarely straightforward.

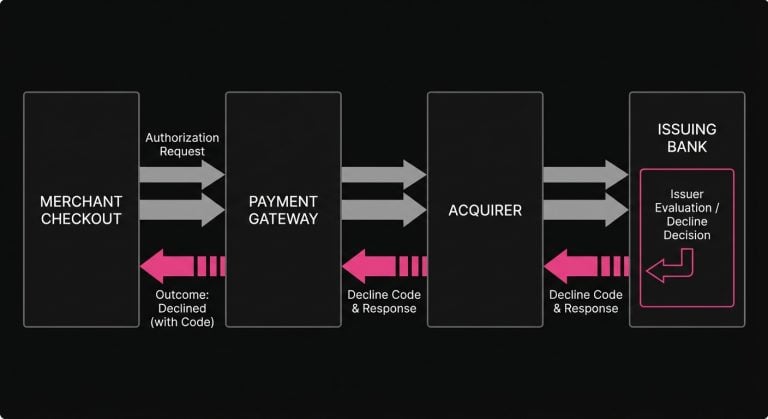

An authorization request is not merely a financial transaction. It is a request for permission that travels from your checkout page through a gateway, to an acquirer, across a major card network, and finally lands at an issuing bank. The issuer evaluates the data alongside the cardholder’s account and makes a decision. A yes means business moves forward. A no leaves you with a decline code.

But not all rejections are created equal. In the payments industry, we generally categorize them into two distinct buckets: hard declines and soft declines. Knowing the difference between an absolute refusal and a temporary roadblock is the foundational step in turning lost sales into captured revenue.

The Anatomy of the Payment Processing Flow

To fully grasp why declines happen, it helps to understand the conversational nature of the payment processing flow. When a customer attempts a purchase, your system sends a highly structured message through the financial networks. This message contains the card details, the transaction amount, your merchant category code, and various contextual data points like the time of day and the customer’s IP address.

The issuing bank evaluates this package against a matrix of rules. They check if the numbers match, if the account is active, and whether the customer has sufficient funds. They also assess if the transaction fits typical spending behavior.

If any of these checks trigger a concern, the issuer sends back a decline code. Historically, these codes were designed for bank tellers and early point-of-sale terminal operators rather than modern e-commerce engines. Because of this legacy architecture, the responses can sometimes feel cryptic. However, they almost always fall into one of two strategic categories, each demanding a completely different operational response.

Hard Declines: The Immutable Disapproval

A hard decline occurs when the issuing bank determines that the transaction cannot be completed, and more importantly, that it will never be completed under the current circumstances. The issuer is effectively stating that the fundamental properties of the payment method are invalid.

Common triggers for a hard decline include situations where a card has been reported lost or stolen, the account has been permanently closed, or the card number itself is simply invalid. In these scenarios, the underlying state of the account has changed in a permanent way.

When you encounter a hard decline, the rule of thumb is simple: stop asking. Attempting to process the same transaction with the same card details an hour later, a day later, or a week later will not yield a different result. An account that was closed on Tuesday will still be closed on Wednesday.

Continuing to push against a hard decline is not just futile, as it actively works against your business. Major card networks closely monitor merchant authorization traffic. If your system continuously hammers away at closed accounts or stolen cards, it sends a signal to the networks that your payment operations are either unsophisticated or potentially fraudulent. This can lead to increased network fees, scheme penalties, and a degradation of your overall transaction approval rate. The most professional response to a hard decline is to immediately halt billing attempts, notify the customer to update their payment method, and gracefully close the loop. Read more about Issuer Response Code 43.

Soft Declines: The Situational Roadblock

If a hard decline is a locked door, a soft decline is a temporary traffic jam. A soft decline indicates that the payment method is generally valid, the account is open, and the card is fundamentally in good standing. However, due to a specific, often temporary circumstance at the exact moment the authorization was attempted, the transaction cannot go through.

The most common example of a soft decline is insufficient funds. The customer simply does not have enough available balance or credit at the precise millisecond your system requested the funds. Other common triggers include temporary network outages at the issuing bank, suspected fraud triggers based on unusual velocity, or the cardholder temporarily hitting a daily spending limit.

The defining characteristic of a soft decline is its fluidity. A customer lacking funds on a Thursday morning might receive a direct deposit the next day. Similarly, a bank undergoing core maintenance at 2:00 AM is often perfectly operational just a few hours later.

Because the underlying context is subject to change, soft declines present a massive opportunity for revenue recovery. Treating a soft decline like a hard decline means leaving perfectly good money on the table and risking involuntary customer churn. Instead, these are the scenarios where a thoughtful, strategically timed follow-up attempt often results in a successful charge. Learn the Decline Code 51: The Soft Decline Recovery Strategy That Recovers Lost Revenue.

The Gray Zone: Decoding the Ambiguous Responses

In a perfect world, the dividing line between hard and soft declines would be mathematically precise. In reality, payment networks operate with a fair amount of ambiguity. The most notorious example is the generic decline, often categorized under response code 05 and commonly known as Do Not Honor.

Code 05 is essentially the banking equivalent of a polite but unhelpful shrug. It means the issuer is rejecting the transaction without specifying exactly why. An issuer might use this code when they suspect fraud but prefer not to explicitly flag the card. Alternatively, internal risk systems might have flagged a purchase as slightly anomalous, or the bank simply defaulted to this response when a more specific error code was unavailable.

This ambiguity creates a challenge for payment teams determining whether a Do Not Honor response is a hard or soft decline. The answer tends to be probabilistic rather than deterministic. Often, an initial generic decline can successfully clear if retried a few days later, suggesting it was a situational issue. If the decline persists across multiple carefully timed attempts, however, it effectively hardens into a permanent failure.

Experienced payment professionals know that navigating this gray zone requires stepping away from rigid, one-size-fits-all rules and moving toward intelligent, data-informed strategies that weigh the context of the initial failure against the statistical likelihood of future success. See our article on How to Recover 05 Do Not Honor Declines With Smarter Payment Retries.

The Impact on Recurring Revenue and Subscriptions

The distinction between hard and soft declines becomes exponentially more critical when operating a recurring billing model. Checkout issues with one-off e-commerce purchases are immediate. The customer is actively engaged at the screen, sees the declined card, and can quickly reach into their wallet for an alternative. The friction is high, but the communication loop is tight.

Subscription payment issues operate differently since recurring billing typically happens asynchronously in the background. If a renewal payment fails, the customer is not there to instantly correct it. Should the merchant’s system fail to elegantly handle the decline, the subscription is canceled and the business suffers involuntary churn. The customer never actively chose to leave. The payment machinery simply gave up on them.

In recurring models, the approach to soft declines dictates the health of the customer base. Automatically canceling a subscription after a single insufficient funds response is an overly aggressive posture that damages lifetime value. Conversely, retrying the card every single day for a month without adjusting the strategy annoys the customer, racks up transaction fees, and degrades issuer trust. Finding the middle path is where the art and science of payment optimization intersect.

Building an Intelligent Payment Recovery Strategy

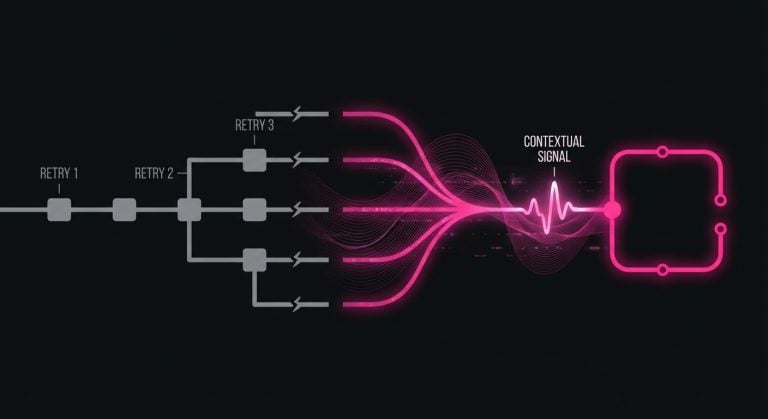

Moving from a reactive stance to a proactive recovery strategy requires changing how your systems respond to failure. The goal is not simply to retry failed payments as often as the network allows, but to retry them at the exact moment they are most likely to succeed.

Naive retry logic operates on a static schedule, perhaps retrying exactly 24 hours after the initial failure and then 48 hours later. While this is better than nothing, it ignores the behavioral realities of personal finance. If a transaction fails due to insufficient funds at 3:00 PM on a Tuesday, retrying at 3:00 PM on a Wednesday rarely changes the outcome.

An intelligent strategy incorporates metadata and real-world context. For instance, it might evaluate the time of the month, recognizing that consumer liquidity tends to be highest around common payroll dates like the 1st and the 15th. It also factors in the time of day, perhaps delaying retries until after morning banking batch processes clear. Varying this timing rather than rigidly adhering to a 24-hour cycle often yields a much higher rate of success.

Determining the precise timing and cadence for these follow-up attempts requires analyzing vast amounts of historical authorization data to identify patterns human operators might miss. This is the operational reality addressed by purpose-built platforms like SmartRetry. These systems provide tools focused on payment optimization and intelligent retries, helping merchants recover revenue and improve transaction approval rates without running afoul of network rules.

The Role of Upstream Optimization

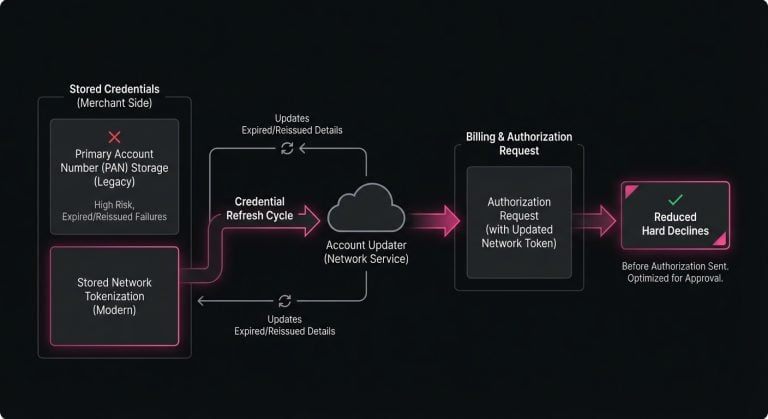

While optimizing retries is a powerful lever for dealing with soft declines, the most sophisticated payment operations also focus on reducing the volume of hard declines before they even occur. This is typically achieved through upstream technologies that keep payment credentials fresh and valid.

One of the most effective methods for reducing hard declines is implementing network tokenization. Rather than storing the raw primary account number, or PAN, the merchant stores a cryptographic token issued directly by the card network. Because the network maintains the mapping between the token and the underlying card, lifecycle events such as a card expiring or being reissued after a loss are automatically updated in the background.

Similarly, Account Updater services proactively poll the networks for updated card details just before a billing cycle runs. When these tools are utilized effectively, a significant portion of hard declines related to expired or reissued cards simply vanishes from the payment processing flow.

Interestingly, as a merchant successfully implements these upstream optimizations, their overall decline ratio will shift. Because the preventable hard declines are being caught and resolved before the authorization request is even sent, the remaining declines will heavily skew toward soft declines and legitimate fraud blocks. This is a sign of a healthy, maturing payment stack.

The Cost of Getting It Wrong

Handling declines poorly carries compounding costs that extend far beyond the immediate lost sale. On one end of the spectrum is the cost of under-retrying. Every valid customer who is turned away due to a mishandled soft decline represents not just lost immediate revenue, but lost future value. The marketing dollars spent to acquire that customer are wasted, and the business must spend even more to replace them.

On the other end of the spectrum is the cost of over-retrying. Card networks operate on trust and predictability. Issuers dynamically adjust their fraud algorithms based on the quality of traffic a merchant sends them. If a merchant gains a reputation for blindly hammering the network with repeated requests for previously declined transactions, issuers will begin to view all of that merchant’s traffic with heightened suspicion.

When issuer trust degrades, the merchant’s transaction approval rate drops across the board. Even pristine, perfectly valid transactions from new customers might start getting caught in the crossfire of tightened issuer risk filters. Furthermore, acquirers and processors pass along network fees for excessive retry attempts, turning a revenue recovery effort into a margin-draining expense. The balance lies in respecting the issuer’s hard boundaries while thoughtfully exploring the soft ones.

Balancing Persistence with Precision

In the end, effectively managing hard and soft declines is about establishing a more sophisticated dialogue with the financial networks. It requires recognizing that a decline is not the end of a transaction, but rather a data point that informs what should happen next.

When encountering the immutable refusal of a hard decline, the best course of action is to cleanly close the technical loop and prompt the user for a new payment method. You protect your network standing by refusing to process dead credentials.

A soft decline, on the other hand, is a situational roadblock that pushes you into the realm of strategy. Leveraging timing, data, and behavioral understanding gives the transaction the best possible chance of clearing on a subsequent attempt. This approach trades blind persistence for calculated precision.

Payment systems will always be inherently probabilistic. There is no silver bullet guaranteeing every valid transaction will clear on the first attempt. However, by understanding the hidden language of network responses, separating permanent failures from temporary roadblocks, and systematically optimizing how you respond to both, merchants can dramatically reduce friction in their checkout flows. The ultimate objective is ensuring you never lose a customer to a mechanical misunderstanding, reserving declines only for transactions that truly cannot, and should not, be processed.

Still letting failed transactions slip through?

SmartRetry turns declines into approvals - automatically, intelligently, and without changing your payment provider.

Frequently asked questions about this topic

Share this article

Author

Roi Lagziel

Roi Lagziel is a payments engineer specializing in authorization optimization, retry strategies, and issuer-level behavior. His work focuses on building practical, data-driven systems that help payment teams reduce false declines and recover lost revenue.

Read all articles >More in Smart Payment Retry Strategies:

March 8, 2026

The Boomerang Effect: Why Brute-Force Retries Cost More Than They Recover

This article explains why blind payment retries erode issuer trust, add network costs, and hurt future approvals, and how smarter decline management can improve recovery and authorization performance.

March 8, 2026

The Art of the Second Chance: Decoding Soft vs. Hard Declines

This article explains how to separate recoverable declines from permanent failures, optimize retry logic, and reduce involuntary churn to protect revenue and improve approval performance.

March 8, 2026

How to Recover 05 Do Not Honor Declines With Smarter Payment Retries

This article explains why 05 Do Not Honor is usually a soft decline and how operators can recover revenue through better retry timing, routing, and data enrichment to reduce false declines and churn.