The Boomerang Effect: Why Brute-Force Retries Cost More Than They Recover

March 8, 2026

![]() 12 min

12 min

The Boomerang Effect: Why Brute-Force Retries Cost More Than They Recover

It happens every second of every day. A legitimate customer finally clicks the buy button. The system hums for a moment. Then, the payment is declined. For merchants, this is an incredibly frustrating reality. You did the hard work. You built a great product. You successfully acquired the customer. Yet, right at the finish line, a vague error code stops all the momentum. The most natural human reaction is to simply try again. After all, maybe it was just a temporary network glitch. Maybe the customer just transferred funds into their account while the page was loading. If the transaction declined the first time, hitting the retry button feels like the simplest, most obvious fix. But this instinct often creates far more problems than it actually solves.

In the fast-paced world of digital commerce, persistence is generally considered a virtue. We are taught to follow up, to keep pushing, and to never leave money on the table. However, when we apply this brute-force logic to the payment processing flow, the results can be quietly disastrous. Systems that automatically and aggressively retry failed payments without context or strategy don’t just fail to recover revenue-they actively damage the merchant’s standing within the financial ecosystem.

Understanding why this happens requires stepping away from the merchant dashboard and looking at the payment ecosystem through the eyes of the issuernetworks and issuing banks. When we understand the mechanics of how a transaction is evaluated, it becomes clear why pacing, patience, and intelligence are far more profitable than sheer repetition.

The Illusion of the Temporary Glitch

When a merchant encounters checkout issues or a sudden spike in failed transactions, the immediate assumption is often that something, somewhere, is simply broken. The internet is a noisy place, and timeouts happen. Because of this, it has historically been common practice for engineering and operations teams to build basic retry logic loops into their billing engines.

The logic is straightforward: if an attempt fails, wait a little while and ask again. If it fails again, wait a bit longer. From a purely technical standpoint, this makes sense for resolving standard network errors. If an API endpoint is briefly unresponsive, a quick subsequent attempt usually resolves the issue.

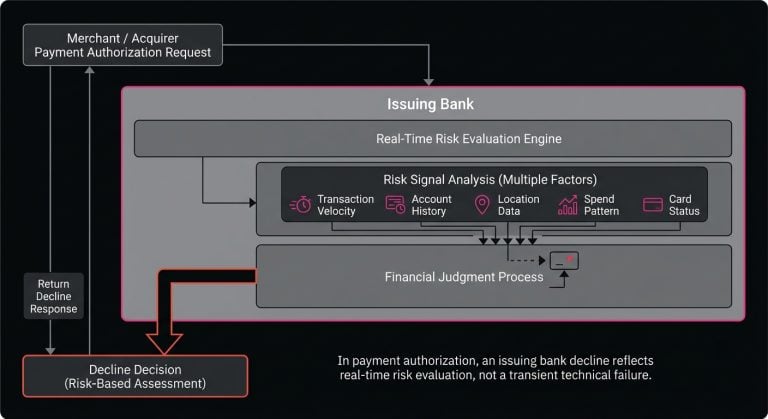

The problem is that a payment authorization is not a simple technical ping. It is a complex, high-stakes conversation between multiple financial institutions. When an issuing bank evaluates a transaction, they are looking at dozens of risk signals in real time. They check the available balance, the velocity of recent purchases, the merchant category, the geographical location of the request, and historical fraud patterns.

When they issue a decline, it is rarely a technical accident. It is a deliberate, probabilistic decision based on the data they have at that exact millisecond. Treating a deliberate financial decision as a mere technical glitch is the first misstep in a flawed payment recovery strategy.

The Financial Toll of Blind Persistence

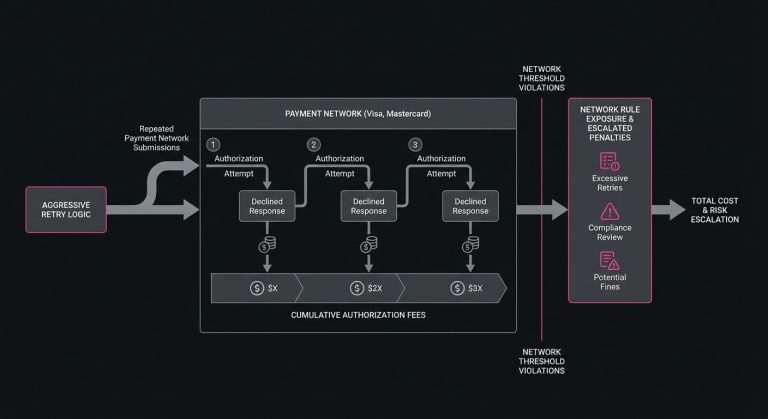

The most immediate and tangible consequence of aggressive retry logic is the direct financial cost. Every single time a merchant sends a request through the payment network, it carries a cost. It doesn’t matter if the transaction is approved or declined; the infrastructure was still utilized, and the toll must be paid.

Standard authorization fees might seem negligible on an individual basis-often just a few pennies per attempt. However, when a poorly configured automated system begins hammering a declined card dozens of times over a billing cycle, those pennies compound rapidly. If you have a significant volume of payment failures, you can easily end up spending a staggering amount of money just to be repeatedly told “no.”

Beyond the standard authorization fees, the major card networks have become increasingly strict about how merchants handle retries. Networks like Visa and Mastercard have implemented specific rules and penalty fee structures designed specifically to discourage merchants from endlessly submitting the same doomed transaction. Visa, for example, allows up to 15 retry attempts in 30 days for the same transaction (Source).

If a merchant violates network thresholds for retry attempts, they aren’t just wasting standard authorization fees; they are actively inviting expensive non-compliance fines. Every attempt past 15 retries in 30 days can incur an approximately $0.10 penalty per retry domestically. The networks operate on efficiency, and they view excessive retry traffic as a strain on their system. Consequently, they pass the cost of that strain directly back to the merchant.

Decoding the Nuance of a Decline

To understand when aggressive retries backfire, we have to recognize that not all payment issues are created equal. Issuing banks communicate their decisions through specific response codes, and treating all of these codes the same way is a recipe for operational headaches.

Broadly speaking, declines fall into two categories: hard declines and soft declines.

The Finality of Hard Declines

A hard decline is an absolute, non-negotiable rejection from the issuing bank. This includes codes indicating that the card is lost, the card is stolen, the account has been closed, or the card number is simply invalid.

Retrying a hard decline is entirely futile. It is the equivalent of knocking repeatedly on the door of a house that has already been demolished. If the bank says the account no longer exists, trying again four hours later is not going to yield a sudden, miraculous reopening. Continuing to retry hard declines is not only a waste of money, but it is also one of the clearest signals to the network that a merchant is either acting carelessly or utilizing fraudulent tactics.

For example, merchants should immediately stop retries on stolen cards, as explained in Issuer Response Code 43: Why Merchants Must Stop Retries on Stolen Cards.

The Opportunity in Soft Declines

Soft declines, on the other hand, represent temporary conditions. The most common example is insufficient funds, but soft declines can also occur due to temporary limits being exceeded, or unexpected out-of-pattern spending that triggers a temporary risk hold.

These are the transactions that are actually worth recovering. Optimized retry logic can recover 15-30% of initially failed payments Decline Code 51: The Soft Decline Recovery Strategy That Recovers Lost Revenue. However, even with soft declines, aggressive repetition backfires. If a customer does not have the funds in their account at 9:00 AM on a Tuesday, they are highly unlikely to have those funds at 2:00 PM on the same Tuesday. Asking the bank repeatedly throughout the day doesn’t change the customer’s bank balance; it only changes the bank’s perception of the merchant.

Payment teams can learn how to recover soft declines with smarter retry timing in How to Recover 05 Do Not Honor Declines With Smarter Payment Retries.

Issuer Memory and the Erosion of Trust

The most expensive cost of an aggressive retry strategy isn’t the direct network fees-it’s the invisible damage done to the merchant’s reputation with issuing banks.

Issuers employ incredibly sophisticated, machine-learning-driven risk models to protect their cardholders. These models are constantly learning and adapting based on merchant behavior. When a bank observes a merchant rapidly and blindly submitting the exact same failed transaction over and over, their algorithms take note. To a bank’s security model, a merchant indiscriminately firing authorization requests looks virtually indistinguishable from a malicious actor running a botnet to test stolen credit card numbers.

Over time, this behavior degrades the merchant’s trust score with that specific issuer. As the issuer’s confidence in the merchant drops, the bank becomes inherently more conservative when evaluating future transactions from that merchant.

This creates a devastating ripple effect. A merchant might be aggressively retrying to recover a few lost dollars today, but in doing so, they are inadvertently teaching the bank to decline perfectly legitimate, first-time purchases tomorrow. When a merchant’s overall transaction approval rate begins to mysteriously decay across the board, aggressive past retry behavior is frequently a hidden culprit.

The Unique Challenge of Recurring Billing

The temptation to forcefully retry failed transactions is perhaps strongest for subscription and Software-as-a-Service (SaaS) businesses. Unlike traditional e-commerce where the customer is actively checking out and can simply pull a different card out of their wallet, subscription renewals happen invisibly in the background.

When subscription payment issues arise, the merchant faces a difficult dilemma. If they cannot successfully charge the card, they eventually have to suspend the user’s access to the software or halt the shipment of a physical product. This creates an intense internal pressure to recover the payment as quickly as possible to prevent involuntary churn.

Consequently, subscription platforms often default to rigid, high-frequency retry schedules. They might attempt the charge every 24 hours for a week, hoping to catch the moment the customer deposits a check.

But this ignores the reality of how consumers manage their money. People generally do not receive income on random Tuesdays. They are paid on specific, predictable schedules-typically the 1st and 15th of the month, or on Fridays. An aggressive daily retry schedule burns through network allowances and racks up fees on days when a successful authorization is statistically improbable. A patient, strategically spaced approach aligned with natural cash-flow cycles is vastly more effective.

Shifting from Brute Force to Payment Optimization

If brute-force persistence is harmful, the logical alternative is intelligent intentionality. Moving away from aggressive retries requires a fundamental shift in perspective. Instead of asking, “How many times can we try to run this card before we give up?” the better question is, “When is the statistically optimal moment to ask the issuer again?”

This is the core premise of true payment optimization. It involves treating every decline not as a failure to be hammered away, but as a data point to be interpreted.

A thoughtful approach starts with parsing the exact issuer response. If the response indicates a hard decline, the system should immediately halt all future attempts and automatically trigger a customer outreach workflow, prompting them to update their billing details. There is no optimization to be found in retrying a closed account; the only optimization is knowing when to stop trying.

For soft declines, optimization means pacing. It means looking at the historical success rates of retries and recognizing patterns. If data shows that retrying an “insufficient funds” decline has the highest probability of success on a Friday afternoon, then the system should intentionally hold that transaction in a queued state until Friday afternoon, regardless of how many days away that might be.

Designing an Intelligent Recovery Workflow

Building a sustainable strategy to reduce payment declines requires orchestrating several different mechanisms in harmony. It is rarely as simple as just changing the timing of a retry loop.

Leveraging Network Tools

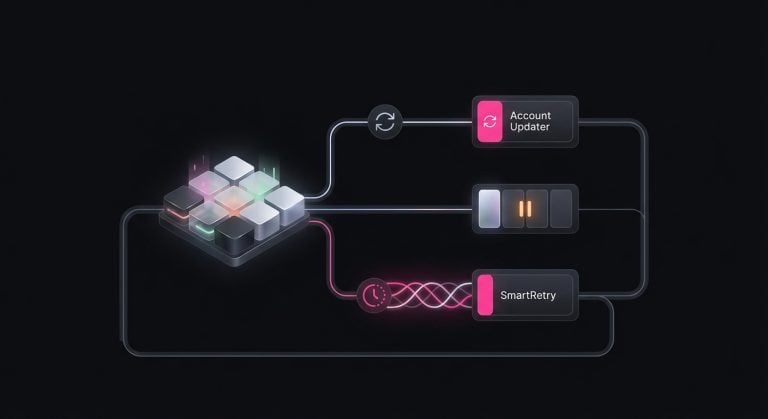

Before a transaction is ever retried, modern workflows utilize Account Updater services provided by the card networks. Often, a card declined message is simply the result of an expired expiration date or a re-issued card following a lost wallet. By checking with the network for updated credentials before initiating the next retry, merchants can bypass the decline entirely and process the payment with the new, valid information.

Applying Contextual Pacing

Pacing must also account for the time of day. If a customer originally purchased a subscription at 8:00 PM on a Sunday, retrying a failed renewal at 3:00 AM on a Wednesday is often suboptimal. The bank’s risk models frequently prefer to see recurring transactions align roughly with the historical purchasing patterns of the cardholder.

Utilizing Specialized Infrastructure

Navigating these granular variables manually at scale is virtually impossible for most internal engineering teams. When addressing these complexities, modern merchants increasingly rely on specialized infrastructure. More than 90% of merchants employ at least one tool to boost authorization rates like automated retries Why Card Declines Happen and How Intelligent Recovery Protects Revenue. Platforms like The Boomerang Effect: Why Brute-Force Retries Cost More Than They Recover serve as a natural example here, focused on payment optimization and intelligent retries of declined payment transactions. By analyzing issuer behavior and dynamically adjusting based on specific decline codes, these tools help merchants recover revenue and improve transaction approval rates without blindly hammering the network or jeopardizing their standing with banks.

The Broader Impact on Overall Health

When a merchant successfully transitions away from an aggressive, high-frequency retry model to a patient, data-informed strategy, the benefits extend far beyond simply saving money on network fees.

The most profound impact is often observed in the merchant’s baseline transaction approval rate. As the merchant stops submitting doomed transactions and begins respecting the issuer’s hard declines, their ratio of successful authorizations to total attempts naturally improves.

Issuing banks monitor this ratio closely. A merchant that maintains a clean, highly successful authorization stream is viewed as a low-risk partner. When a merchant proves that they operate intelligently and respect the boundaries of the network, issuing banks become far more lenient when evaluating borderline transactions in the future.

By strategically choosing not to retry certain payments, merchants actively improve their chances of getting subsequent, higher-value transactions approved on the first attempt. It is a classic scenario where doing less actually yields significantly more.

Redefining Persistence in Payments

The instinct to continuously try to push a failed transaction through is entirely understandable. In almost every other aspect of business, persistence is rewarded. But the payment ecosystem operates under a different set of rules, governed by risk models, compliance thresholds, and intricate network fees.

In this environment, aggressive repetition is not persistence; it is friction. It aggravates the issuing banks, frustrates the card networks, and quietly drains the merchant’s profit margins.

True persistence in the realm of payment recovery does not mean asking the same question over and over until you get a different answer. It means taking the time to understand exactly why the door was closed in the first place, waiting for the optimal moment, and using the right key to open it smoothly. By replacing blind force with strategic intelligence, merchants can protect their margins, build trust with the networks, and ultimately recover far more revenue over the long term.

Still letting failed transactions slip through?

SmartRetry turns declines into approvals - automatically, intelligently, and without changing your payment provider.

Frequently asked questions about this topic

Share this article

Author

Roi Lagziel

Roi Lagziel is a payments engineer specializing in authorization optimization, retry strategies, and issuer-level behavior. His work focuses on building practical, data-driven systems that help payment teams reduce false declines and recover lost revenue.

Read all articles >More in Smart Payment Retry Strategies:

March 8, 2026

Decoding Hard and Soft Declines: A Practical Guide to Smarter Payment Recovery

This guide explains how to classify payment declines, respond with the right retry strategy, and reduce unnecessary churn, fees, and approval-rate drag across checkout and recurring billing.

March 8, 2026

The Art of the Second Chance: Decoding Soft vs. Hard Declines

This article explains how to separate recoverable declines from permanent failures, optimize retry logic, and reduce involuntary churn to protect revenue and improve approval performance.

March 8, 2026

How to Recover 05 Do Not Honor Declines With Smarter Payment Retries

This article explains why 05 Do Not Honor is usually a soft decline and how operators can recover revenue through better retry timing, routing, and data enrichment to reduce false declines and churn.