Beyond the Monolith: Why Global Scale Demands a Multi-Acquirer Mindset

March 8, 2026

![]() 12 min

12 min

Beyond the Monolith: Why Global Scale Demands a Multi-Acquirer Mindset

Launching a business often begins with a beautifully simple payment stack. You pick a highly capable payment partner. You integrate their API. You go live. For a while, everything just works. Revenue flows in smoothly. Operations teams sleep soundly at night. But scale inevitably changes the equation. As your customer base expands across borders, this monolithic approach starts showing natural stress fractures. You might notice an unexpected uptick in checkout issues. You see a frustrating number of payment failures in specific geographic regions. The realization slowly dawns that relying on a single connection to the financial world has practical limitations. Scaling a global revenue engine requires a more diversified, intelligent infrastructure.

At its core, payment processing is a probabilistic exercise rather than a deterministic one. Sending a payment request through the global financial plumbing does not guarantee a successful outcome, even if the customer has sufficient funds and good intentions. Every single step in the payment processing flow introduces a new set of risk checks, latency variables, and nuanced routing decisions. When you route everything through a single acquiring partner, you are fundamentally tying your entire global operation to one specific set of risk algorithms, one localized network of banking relationships, and one point of infrastructure dependency.

Moving beyond the monolith is not about abandoning your primary payment partner. Rather, it is about evolving your infrastructure to match the complexity of your customer base. It requires adopting a multi-acquirer mindset, where routing decisions are made dynamically, redundancies are built in by design, and payment optimization becomes a continuous, automated process.

The Illusion of the Universal Payment Partner

The appeal of the single-acquirer setup is obvious and entirely justified for many businesses. It offers unified reporting, a single integration point, and simplified reconciliation for your finance team. When you are processing transactions primarily within a single domestic market, a robust acquiring partner will typically deliver excellent approval rates.

However, the concept of a single universal acquirer that performs equally well in every global market is largely an operational myth. Payment networks are highly regionalized, and issuing banks-the institutions that ultimately decide whether to approve or decline a transaction-rely heavily on local context when evaluating risk.

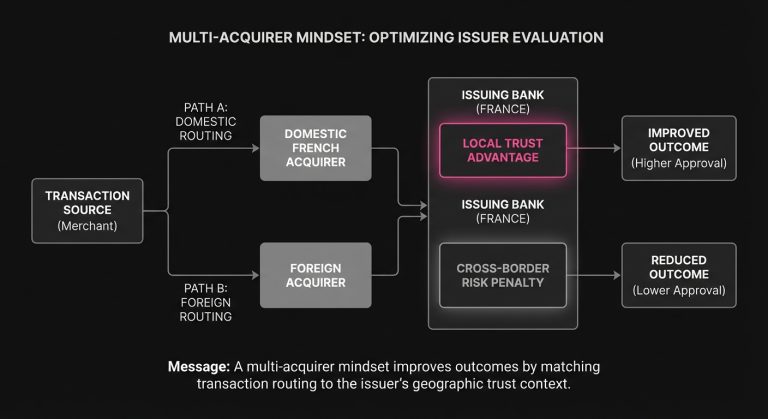

When an issuing bank evaluates a transaction, it looks at dozens of data points in milliseconds. It assesses the BIN, the transaction value, the velocity of recent purchases, and crucially, the geographic origin of the acquiring bank. If a bank in France receives an authorization request from a domestic French acquirer, the transaction benefits from a baseline level of institutional trust. The local networks are familiar, the risk profiles are well understood, and the transaction is generally viewed as lower risk.

Conversely, if that same French issuer receives a request from a foreign acquirer-even if the transaction is presented in Euros-the bank’s automated fraud systems often view the cross-border routing with mild suspicion. The lack of familiar domestic data signals can artificially lower the transaction approval rate. In many cases, a card declined under these circumstances has nothing to do with the cardholder’s available balance, but rather the issuer’s localized risk thresholds reacting to unfamiliar routing.

The Geography of Approvals

To understand why global scale demands multiple acquirers, it is helpful to look closely at how geographic relationships impact the payment ecosystem. The fundamental rule of global payments is that local volume tends to perform best on local rails.

When a merchant establishes a multi-acquirer setup, they gain the ability to route transactions based on the BIN of the customer’s card. The BIN identifies the specific issuing bank and its location. With a dynamic routing layer in place, a merchant can systematically direct European transactions to a European acquirer, North American transactions to a US-based acquirer, and Latin American transactions to an acquirer with deep connectivity in that specific region.

This localized approach to acquiring achieves several crucial objectives simultaneously. First, it aligns the transaction with the issuer’s preferred geographic profile, leading to more favorable risk scoring and fewer false positives. Second, it frequently reduces processing costs. Cross-border interchange rates and scheme fees are generally higher than domestic rates. By ensuring transactions are settled locally wherever possible, merchants can meaningfully reduce their overarching cost of payment acceptance while simultaneously improving conversion; in one study, nearly two-thirds of merchants reported cost reductions of at least 2% (Source).

The operational reality is that no single provider possesses tier-one, direct acquiring relationships in every single country on earth. Providers naturally have stronger banking relationships, better data sharing agreements, and more optimized authorization messaging in their home regions. Embracing a multi-acquirer strategy simply allows a merchant to leverage the specific regional strengths of different partners.

Deciphering the Issuer Response

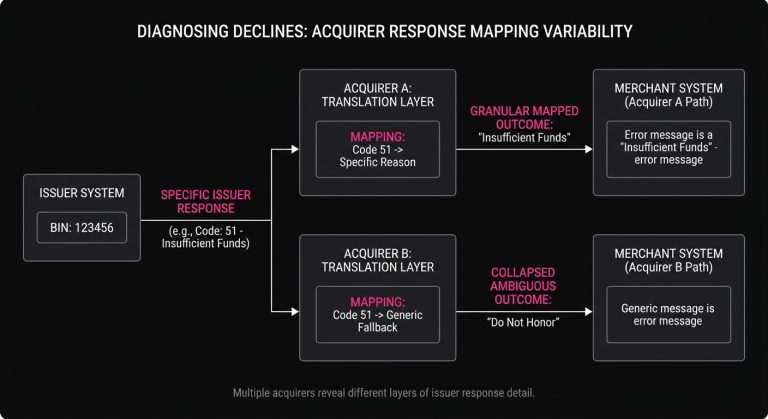

One of the most complex challenges in payment optimization is interpreting the feedback provided when a transaction does not succeed. When a payment declined message comes back through the gateway, it is rarely accompanied by a perfectly clear, actionable explanation.

Instead, merchants are often presented with cryptic, generalized codes. The most infamous of these is “Do Not Honor” (often represented as code 05). This generic issuer response acts as a catch-all bucket for everything from suspected fraud and mismatched billing addresses to temporary network timeouts and overly aggressive risk filters. It tells the merchant almost nothing about the actual root cause of the failure.

The complexity deepens when you realize that different acquirers map and translate these issuer responses differently. An issuer might send a specific granular decline code back through the card network, but Acquirer A’s legacy gateway infrastructure might roll that specific code up into a generic “System Error” message. Acquirer B, using more modernized schema mapping, might pass the granular code through accurately, revealing that the issue is simply an expired card.

Having access to multiple acquirers allows sophisticated merchants to test and observe how different processing paths interpret the same BIN behavior. If a specific subset of transactions is consistently experiencing high decline rates with one acquirer, routing a portion of that traffic to a secondary acquirer can quickly reveal whether the issue is systemic to the cards themselves, or a quirk of the first acquirer’s specific risk configuration.

Dynamic Routing and the Art of the Retry

Adding new acquiring partners to your payment stack is only the first step. The true value of a multi-acquirer setup is unlocked through the orchestration layer-the logic that determines exactly where each transaction should go, and more importantly, what should happen when a transaction fails.

In a monolithic setup, when a payment fails, the standard approach is often a simplistic, rules-based retry logic. The merchant might wait 24 hours and simply ping the exact same gateway again. This static approach frequently yields diminishing returns. If the issuing bank declined the transaction because of the specific way the acquirer formatted the payment authorization message, repeating the exact same request will likely result in the exact same failure.

Dynamic routing shifts this paradigm completely. An intelligent orchestration layer evaluates the specifics of a failed transaction and makes contextual decisions about how to retry failed payments. If a transaction fails due to a suspected network timeout or an acquirer-side gateway error, the system can instantly reroute the transaction to a secondary, healthy acquirer before the customer even notices a delay at checkout.

This is where specialized technology becomes incredibly valuable. Platforms focused on payment optimization, like SmartRetry, help merchants navigate this complexity by leveraging data-driven algorithms to orchestrate intelligent retries of declined transactions. Instead of blindly submitting the same request, these systems analyze the initial issuer response and adjust routing parameters-whether shifting to a local acquirer, changing the network route, adjusting data payloads, or optimizing the exact time of the retry. This approach helps merchants systematically recover revenue and improve transaction authorization rates without requiring an internal team of dedicated payment engineers to manually monitor routing tables. Four in 10 respondents experienced an average acceptance rate lift of approximately 1%.

By treating the retry as a fundamentally new authorization attempt with different variables, merchants can salvage significant portions of otherwise lost revenue. The goal is to present the transaction to the issuer in a slightly different, highly optimized light, increasing the probability of a positive outcome.

The Nuance of Subscription Payment Issues

The challenges of the monolith become particularly pronounced for businesses that rely on recurring revenue models. Managing subscription payment issues introduces a unique set of variables because the customer is rarely present during the transaction.

In a standard e-commerce flow, if a card is declined, the customer is sitting at their screen. The merchant can immediately prompt them to try a different card, double-check their billing zip code, or authenticate the purchase through a 3D Secure prompt. In a recurring billing scenario, the transaction happens asynchronously in the background. If the payment fails, the merchant is forced to initiate a dunning process, risking involuntary churn.

Recurring payments are highly sensitive to processing patterns. Issuing banks closely monitor the cadence and consistency of subscription authorizations. If a merchant suddenly shifts all their recurring volume from a well-established local acquirer to a new, cross-border acquirer, issuers may flag the sudden change in processing behavior and decline the recurring charges, even if the customer’s card is perfectly valid.

A multi-acquirer setup provides the flexibility to manage this volume strategically. A merchant can choose to keep legacy, grandfathered subscriptions on the original acquirer where the recurring token is established and trusted by the issuer, while routing net-new subscriber acquisitions through a more cost-effective regional partner. Furthermore, intelligent retry logic is vital for recovering soft declines-such as insufficient funds-by timing the retry to align with common payroll cycles or typical banking deposit windows in the customer’s specific locale.

Redundancy and the Cost of Downtime

Beyond optimization and conversion, a multi-acquirer strategy is fundamentally an exercise in risk management and operational continuity. The payment processing industry is built on incredibly robust infrastructure, but it is not infallible.

Gateways experience latency. Acquirers schedule routine maintenance windows that unexpectedly run long. Sub-networks experience localized outages. In a single-acquirer environment, any degradation in your partner’s performance translates directly into an immediate loss of revenue. If your sole processor goes offline for twenty minutes during a peak promotional event, the resulting payment issues can have a material impact on quarterly targets.

When multiple processors are integrated, an intelligent routing layer functions as a vital safety net. Modern orchestration systems constantly monitor the health and response times of underlying acquiring connections. If the primary routing path begins returning an unusual spike in gateway errors, or if authorization times stretch from hundreds of milliseconds to multiple seconds, the system can automatically trip a circuit breaker.

This circuit breaker temporarily shunts transaction volume away from the struggling acquirer and pushes it to the secondary partner. Once the primary connection stabilizes and health checks return to normal, the volume can be smoothly rerouted back. This level of active redundancy ensures that temporary infrastructure hiccups remain invisible to the end consumer, protecting the user experience and safeguarding the bottom line.

The Hidden Complexities of Going Multi

While the benefits of diversifying acquiring partners are substantial, it is important to acknowledge that the transition introduces new layers of operational complexity. Managing a multi-acquirer setup is not as simple as flipping a switch; it requires thoughtful architectural decisions, particularly concerning data ownership and reconciliation.

When you process exclusively with one partner, that partner typically handles the tokenization of your customers’ credit cards. They store the sensitive raw PAN (Primary Account Number) in their secure vault and provide you with a proprietary token. The limitation of this model is that the proprietary token can only be deciphered by the processor that issued it.

If you want to route a returning customer’s transaction to a different acquirer to improve the authorization rate or reduce costs, you cannot simply send the proprietary token from Acquirer A to Acquirer B. Acquirer B will not recognize it.

To achieve true routing freedom, merchants must typically decouple their tokenization strategy from their processing strategy. This often involves utilizing a third-party PCI-compliant vault or adopting Network Tokenization. Network tokens are generated directly by the card schemes (Visa, Mastercard) rather than the acquirer. Because they are universally recognized across the payment ecosystem, a merchant can vault a network token once and dynamically route it to whichever acquiring partner offers the best processing condition for that specific transaction.

Reconciliation is another area that requires careful planning. Moving from one unified settlement report to multiple payout schedules, varying reserve requirements, and different fee structures across multiple partners can create significant manual work for finance teams. Implementing a multi-acquirer strategy almost always requires simultaneously upgrading your data ingestion and financial reconciliation tools to ensure you maintain clear visibility into cash flow and processing costs.

Aligning Payment Strategy with Business Growth

The evolution from a single processor to a multi-acquirer environment represents a fundamental shift in how a business views its payment operations. In the early stages of growth, payments are often treated simply as a functional utility-a necessary mechanism for moving funds from the customer to the merchant’s bank account. The primary goal is finding the path of least resistance.

As a company scales globally, this utility mindset becomes a bottleneck. Marginal inefficiencies that were negligible at a smaller scale-a two percent lower approval rate in a specific country, a slightly elevated cross-border fee, a higher rate of unrecovered recurring declines-compound into massive revenue leaks.

Adopting a multi-acquirer mindset transforms payment operations from a passive cost center into an active lever for revenue generation. It empowers teams to treat every region, every issuing bank, and every transaction profile as a unique variable that can be optimized. It acknowledges the inherent complexity of the global financial system and builds an architecture specifically designed to navigate it. Nearly 97% of enterprise merchants operate with multiple acquirers.

The initial single-acquirer monolith is often the perfect tool for getting a business off the ground. It provides the speed and simplicity necessary to launch and find product-market fit. But as the geography of your customer base expands and the volume of transactions grows, clinging to a single processing path inevitably limits potential. Embracing redundancy, localized routing, and intelligent retry strategies ensures that your infrastructure is as robust, dynamic, and globally capable as the business it supports.

Still letting failed transactions slip through?

SmartRetry turns declines into approvals - automatically, intelligently, and without changing your payment provider.

Frequently asked questions about this topic

Share this article

Author

Roi Lagziel

Roi Lagziel is a payments engineer specializing in authorization optimization, retry strategies, and issuer-level behavior. His work focuses on building practical, data-driven systems that help payment teams reduce false declines and recover lost revenue.

Read all articles >More in Payment Approval Optimization:

April 16, 2026

Why Transaction Approval Rate Is Misleading and What Payment Teams Should Measure Instead

This article explains why blended approval rate can distort payment decisions and how teams can use recovery, cohort, and retry metrics to protect revenue and reduce false declines.

March 8, 2026

Why Virtual Card Payments Fail in Travel and How Payment Teams Improve Approval Rates

This article explains why travel virtual cards fail at hotels and what operators can do to recover approvals, cut manual intervention, and protect margins across issuing and acquiring.

March 8, 2026

The Invisible Logic of 3D Secure: How Payment Teams Balance Fraud, Friction, and Revenue

This article explains how payment teams can use 3D Secure, exemptions, and soft-decline handling to cut false declines, protect conversion, and improve recurring revenue performance.