Decline Code 51: The Soft Decline Recovery Strategy That Recovers Lost Revenue

March 8, 2026

![]() 16 min

16 min

Decline Code 51: The Soft Decline Recovery Strategy That Recovers Lost Revenue

Every merchant knows the sting of payment issues. A customer decides to buy. They enter their card details. They click the final button. Then, the system halts. The screen flashes a transaction declined message. The momentum vanishes instantly. For many businesses, this moment feels like a permanently closed door. But seasoned payments professionals view this differently. They know that not all declines are created equal. Code 51 is a perfect example of a misunderstood error. It signals insufficient funds. On the surface, it looks like a dead end. In reality, it is a temporary roadblock. Money flows in highly predictable cycles. Account balances change constantly throughout the week. If you deeply understand the mechanics behind this specific issuer response, you can build a formidable recovery engine. This engine does not just manage failure. It actively reclaims revenue that belongs to you. Let’s explore exactly how to turn this common hurdle into a predictable, optimized growth lever.

Decoding the Mechanics of a Code 51 Decline

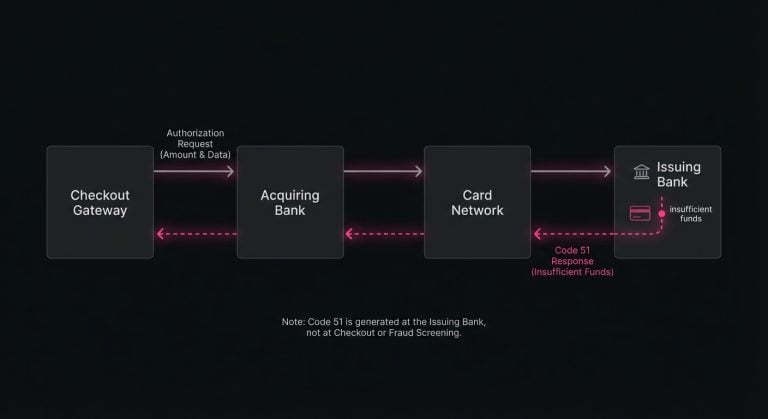

When a customer initiates a purchase, a complex digital conversation happens in milliseconds. Your checkout gateway formats the request. The acquiring bank forwards it through the card network. Finally, the issuing bank receives the payload and evaluates it against the cardholder’s account. This payment processing flow is highly standardized across the globe, yet the outcomes are beautifully nuanced and rich with data.

When the issuer responds with Code 51, they are communicating a very specific state of affairs. They are telling you that the card is valid, the account is open, and there are no fraud holds in place. The only issue is that the available balance at this precise millisecond cannot cover the requested authorization amount.

To a risk team or a payment operations manager, this is fundamentally encouraging news. The hardest parts of the transaction have already succeeded. You have acquired a real customer. They have provided legitimate payment credentials. The transaction is not being blocked by a rigid fraud filter, and the card has not been reported lost or stolen. The only missing ingredient is liquidity.

Understanding this distinction is the bedrock of payment optimization. Many organizations mistakenly lump Code 51 into a generalized bucket of failures, treating it with the same finality as a closed account or an invalid card number. This is a costly operational oversight. A closed account is a hard decline; it will never succeed, no matter how many times you attempt to process it. An insufficient funds response, however, is an inherently soft decline. By recognizing the fluid nature of account balances, merchants can shift their approach from passive acceptance to active, intelligent recovery.

The Temporal Nature of Soft Declines

To master the recovery of a Code 51, we first have to agree on what a soft decline actually represents in the wild. In the broader payment ecosystem, a soft decline implies that the transaction might be successful if attempted again under slightly different circumstances. Sometimes those circumstances involve passing additional data elements, like an updated expiration date or a clearer billing descriptor. But with Code 51, the changing circumstance is strictly temporal. It is entirely about the clock and the calendar.

Think about how modern consumer banking works in practice. Direct deposits hit checking accounts at two in the morning on a Friday. Peer-to-peer transfers clear on a Tuesday afternoon. Auto-pay utility bills deduct funds randomly throughout the week, often catching consumers off guard. A consumer’s debit card balance is not a static number carved in stone; it is a highly volatile data point that breathes in and out with the rhythm of their daily financial life.

When a card declined event occurs due to insufficient funds, it simply means you caught the account on an exhale. The money is not there right now, but experience and data show that it is highly likely to return. This is especially true for subscription payment issues, where recurring charges often hit exactly when a customer’s account is at its absolute lowest point, which is typically the day right before payday. Insufficient funds represents 44% of all declines (Source).

If a merchant throws away a Code 51 decline without a strategy to re-engage, they are effectively leaving perfectly good money on the table. The customer still wants the product or service. They still have an active relationship with your business. The only thing standing between the decline and a successful capture is timing.

The Danger of the Brute-Force Retry Trap

Once teams realize that Code 51 is temporary, the natural instinct is often to try again immediately. And then try again a few hours later. And perhaps try again the next morning. This brute-force approach to retry failed payments is one of the most common, and most damaging, pitfalls in payment operations.

It seems logical on the surface: if the problem is a temporary lack of funds, just keep knocking on the door until the funds arrive. However, the payment networks and issuing banks do not look kindly upon endless, unoptimized pings. Every time you send an authorization request, it costs fractions of a cent in processing fees. More importantly, it consumes network bandwidth and forces the issuer’s infrastructure to process a redundant request.

If a merchant aggressively retries a declined card without a thoughtful cadence, they run the very real risk of tripping issuer velocity limits. Banks employ sophisticated risk models that monitor exactly how often a specific merchant attempts to authorize a specific card. If you repeatedly hammer an account that is legitimately empty, the issuer’s algorithm may begin to view your merchant ID as a nuisance. It is the digital equivalent of a telemarketer calling during dinner; eventually, they are going to block your number.

This aggressive behavior can lead to a boomerang effect. A bank might stop returning a soft Code 51 and instead issue a hard decline, essentially walling off the transaction to protect their system resources and their cardholder. Suddenly, a recoverable soft decline has been permanently shut down due to poor retry etiquette.

Furthermore, major card networks continually update their rules and thresholds around authorization attempts. Excessive retries on a known insufficient funds decline can incur network penalties, driving up the overall cost of your payment operations. The strategic goal is never to retry the card as many times as possible. The goal is to retry it at the exact moment it is statistically most likely to succeed.

The Science of Financial Timing and Pay Cycles

To intelligently recover a Code 51, payment operators have to think less like software engineers and more like behavioral economists. If the success of the transaction depends entirely on the cardholder having money, the foundational question becomes quite simple: when do people actually have money?

In most major economies, liquidity follows highly predictable, cyclical patterns. The most obvious examples are traditional paydays. The first and fifteenth of the month are massive influx days for consumer bank accounts. Similarly, Fridays act as weekly liquidity spikes for hourly workers or those on bi-weekly payroll schedules.

Imagine a recurring subscription attempts to bill on a Wednesday the twelfth and receives a Code 51. Immediately retrying that transaction on Thursday the thirteenth is mathematically suboptimal. The cardholder’s financial state is highly unlikely to have improved within that twenty-four-hour window. However, waiting to retry that exact same transaction on Friday the fourteenth, or Saturday the fifteenth, dramatically increases the probability of a successful authorization.

Beyond macro pay cycles, the time of day matters immensely. Many automated clearing house batches and direct deposits settle in the early hours of the morning. Retrying a previously declined transaction at four in the morning, local time for the issuing bank, often yields higher success rates than attempting it at four in the afternoon. You are catching the account immediately after a deposit clears, before the cardholder has had a chance to spend the funds on their daily expenses like coffee, gas, or lunch.

Understanding these temporal nuances allows payment teams to map out intelligent retry schedules. It shifts the entire operation from a blind guessing game to a strategic execution of probability.

Constructing an Intelligent Recovery Engine

Moving from basic, fixed-schedule retries to a dynamic recovery engine requires a fundamental shift in how you handle transaction data. An intelligent system does not treat every single Code 51 identically. Instead, it evaluates the surrounding context of the decline to determine the optimal next step.

One of the most valuable data points at your disposal is the BIN. The first six to eight digits of a credit or debit card reveal vital information about the card type and the issuing institution. For instance, is this a prepaid debit card, a standard checking debit card, or a premium credit card?

A Code 51 on a standard debit card typically indicates that the checking account lacks available funds at that moment. The recovery strategy here relies heavily on those payday and time-of-day cycles discussed earlier. Conversely, a Code 51 on a credit card usually means the cardholder has hit their credit limit. Credit limits do not magically replenish on paydays; they replenish when the cardholder logs into their banking app and makes a payment to clear their balance. That behavioral cycle is entirely different, often dictating a slightly longer waiting period before a retry is attempted.

This is where leveraging specialized technology becomes a profound operational advantage. Platforms like SmartRetry are built specifically to navigate these complex variables, using historical data and algorithmic logic to optimize the timing of each authorization attempt. By evaluating variables such as BIN data, issuer habits, and transaction contexts, merchants can systematically orchestrate retries at their point of highest probability, steadily recovering revenue that would otherwise be lost to the void. In a global study across 500+ merchants and $1B processed, optimized recovery on insufficient-funds declines drove an additional recovery uplift of 17.6%-26.2% over the last 14 months (Source).

Building or integrating this level of intelligence ensures that you are treating the issuer’s ecosystem with respect. It keeps your merchant account well within network velocity limits, preserves your margin by reducing unnecessary gateway fees, and maximizes the operational yield of your payment teams.

Issuer Logic and the Authorization Window

To truly master the art of the retry, it helps to understand how different issuing banks govern their own internal authorization logic. Not every bank handles an insufficient funds scenario exactly the same way, and expecting uniform behavior across thousands of global issuers is a recipe for frustration.

When you submit an authorization request, you are asking the bank to place a temporary hold on the funds. If the funds are available, the bank approves the request, deducts the amount from the cardholder’s available balance, and waits for you to capture and clear the transaction within a few days.

However, when an account is hovering near zero, the mechanics get interesting. Some modern digital banks might approve a transaction that slightly overdraws the account if the customer has an active overdraft protection setting enabled. Traditional legacy banks might have strict, hard stops precisely at zero. Furthermore, some issuers might instinctively decline a large transaction to protect the account but would readily approve a smaller one.

While merchants cannot legally or technically know a customer’s exact account balance or their personal overdraft settings, they can monitor historical issuer responses. If a specific bank historically shows a high recovery rate on day three of a retry cycle across your portfolio, that data pattern should feed directly into your optimization rules.

Additionally, you must consider the authorization window itself. If a transaction is highly time-sensitive, such as a next-day grocery delivery or a limited-time digital asset, you may only have a twenty-four-hour window to secure the funds before the order must be canceled. In these cases, your retry strategy must be aggressively compressed. For digital goods or software subscriptions where the service can simply be temporarily paused, you have the luxury of stretching the retry schedule over several weeks, patiently waiting for the optimal moment to strike.

Managing the Subtleties of Card Data Decay

When implementing a prolonged retry strategy for soft declines, there is a hidden variable that often catches payment teams off guard: card data decay. If you decide that the best time to retry a Code 51 is twelve days after the initial failure, you are introducing a new risk into the equation. In those twelve days, the physical card might expire, or the customer might report it lost, causing the issuer to cancel the PAN and issue a new one.

If you blindly retry the saved card twelve days later, you might no longer receive a Code 51. Instead, you might receive a hard decline for an invalid or expired card. You waited patiently for the funds to arrive, only to fail on a completely different data point.

To mitigate this, sophisticated recovery strategies often work in tandem with Account Updater services provided by the card networks. Before executing a delayed retry on a high-value transaction, the system silently checks to ensure the card credentials are still valid. If the network indicates that a new card has been issued, the system updates the tokenized PAN in the background and then attempts the authorization against the newly funded account.

This dual-layered approach ensures that you are not just optimizing for time, but also optimizing for data integrity. It prevents a recoverable soft decline from mutating into an unrecoverable hard decline simply because the calendar flipped over.

Measuring Success and Tracking the Right Metrics

You cannot systematically improve what you do not accurately measure. A sophisticated soft decline recovery strategy requires equally sophisticated analytics. Simply looking at your overall, top-level transaction approval rate is not granular enough to tell you if your Code 51 logic is actually working.

To accurately gauge success, payment teams need to isolate the initial decline events from the subsequent recovery attempts. The baseline metric to watch is the first-pass authorization rate. This answers the question: how many transactions succeed on the very first try? Everything that fails on that first pass falls into the recovery funnel.

Within that funnel, you need to track the recovery rate specifically for Code 51 declines. If you experienced one thousand insufficient funds declines in a given month, how many of those specific transactions eventually settled successfully due to your retry logic?

It is equally vital to measure the cost of that recovery. How many retry attempts did it take, on average, to secure an approval? If you are recovering a high percentage of transactions but it takes an average of nine attempts per success, your strategy is likely too aggressive. You are bleeding margin through network processing fees and risking velocity penalties. A highly optimized system should aim to recover the maximum amount of revenue with the absolute minimum number of touches.

Finally, monitor secondary metrics like customer support tickets and involuntary churn. A seamless recovery process should be virtually invisible to the consumer. If they are completely unaware that their payment initially failed because your system intelligently recovered it the next morning, that is a flawless operational execution. If your retry logic results in confused customers calling your support desk because they see odd pending charges, the strategy needs refinement.

The Role of Customer Communication in Recovery

While silent, automated retries are the gold standard for recovering a Code 51, there is a parallel track that involves the cardholder directly. Automation handles the probability of funds, but communication handles the ongoing customer relationship.

Deciding when to notify a customer about checkout issues is a delicate balancing act. If you send an automated email to a customer the exact millisecond a Code 51 occurs, you risk creating unnecessary friction. As we have established, the decline might just be a brief timing issue that your system can resolve automatically in twelve hours. Alerting them too early essentially outsources a solvable problem to the buyer.

The most effective operations teams employ a strategic grace period. They allow their intelligent retry logic to make one or two highly calculated attempts before surfacing the issue to the user. If the automated payment recovery fails after the highest-probability windows have passed, it is then appropriate to trigger a dunning email or an in-app notification.

When you do communicate, the tone should be entirely service-oriented and constructive. Avoid using harsh banking terminology like “insufficient funds,” which can feel accusatory, jarring, or embarrassing to the reader. Instead, frame the message around updating payment details or ensuring uninterrupted access to their service. A gentle prompt that says, “We had trouble processing your recent payment, please update your billing preferences to maintain your account,” is far more effective than a sterile, red-text notification.

By combining automated, data-driven retries with perfectly timed, empathetic customer communication, merchants create a comprehensive safety net. This net catches revenue in the background whenever possible, and gracefully invites the customer to help only when absolutely necessary. Recurly reports that 72% of at-risk subscribers are saved through recovery events (Source).

The Shift from Loss to Active Revenue Generation

Ultimately, mastering the Code 51 decline is about a fundamental shift in perspective. It requires moving away from the outdated idea that a declined card is the end of the road. In the modern financial ecosystem, a decline is merely a data point. It is a brief snapshot of a customer’s liquidity at one specific moment in time, nothing more.

When payment teams internalize this reality, their entire approach to payment optimization transforms. They stop relying on naive, aggressive retry loops that anger issuers and rack up gateway fees. They begin to study the cyclical nature of human finance. They respect the cadence of paydays, the nuances of debit versus credit behaviors, and the varying logic of issuing banks around the globe.

This level of operational maturity is what separates standard maintenance from true revenue generation. Every single transaction recovered from a soft decline goes straight to the top line. It is revenue that was already earned, from a customer who already converted, simply waiting patiently to be securely captured. 60-70% of all declines are potentially recoverable.

The analytical tools, the network data, and the processing methodologies exist to make this happen gracefully. By embracing a thoughtful, temporally aware recovery strategy, businesses can transform one of the most frustrating friction points in commerce into a quiet, relentless engine for growth. The money is out there; you just have to know exactly when to ask for it.

Still letting failed transactions slip through?

SmartRetry turns declines into approvals - automatically, intelligently, and without changing your payment provider.

Frequently asked questions about this topic

Share this article

Author

Roi Lagziel

Roi Lagziel is a payments engineer specializing in authorization optimization, retry strategies, and issuer-level behavior. His work focuses on building practical, data-driven systems that help payment teams reduce false declines and recover lost revenue.

Read all articles >More in Smart Payment Retry Strategies:

March 8, 2026

Decoding Hard and Soft Declines: A Practical Guide to Smarter Payment Recovery

This guide explains how to classify payment declines, respond with the right retry strategy, and reduce unnecessary churn, fees, and approval-rate drag across checkout and recurring billing.

March 8, 2026

The Boomerang Effect: Why Brute-Force Retries Cost More Than They Recover

This article explains why blind payment retries erode issuer trust, add network costs, and hurt future approvals, and how smarter decline management can improve recovery and authorization performance.

March 8, 2026

The Art of the Second Chance: Decoding Soft vs. Hard Declines

This article explains how to separate recoverable declines from permanent failures, optimize retry logic, and reduce involuntary churn to protect revenue and improve approval performance.