How to Recover 05 Do Not Honor Declines With Smarter Payment Retries

March 8, 2026

![]() 12 min

12 min

You stare at the dashboard. A transaction flashes across the screen. It is a perfectly valid customer. They have money in the bank. They want to buy your product. Yet, the system throws up a wall. The message reads “05 Do Not Honor.” It feels like a door slamming in your face. But seasoned payment professionals know a secret. That vague, frustrating code is rarely a hard stop. It is merely the opening line of a negotiation.

In the complex ecosystem of global commerce, payment issues are an inevitable reality. When a transaction fails, it is easy to assume the buyer simply lacks the funds or that the card is invalid. However, the architecture of modern payment processing is far more nuanced. Behind every decline is a probabilistic risk model, a fragmented network of legacy mainframes, and an issuing bank making a split-second judgment call.

Understanding why these judgments happen-and more importantly, how to thoughtfully respond to them-is the line that separates average merchants from top-tier revenue optimizers. The “Do Not Honor” response is the ultimate test of a merchant’s payment infrastructure. It demands curiosity, operational maturity, and a strategic approach to recovering revenue.

The Enigma of the “Do Not Honor” Response

To understand the nature of a generic decline, one must first understand the language of payment networks. When a merchant submits a charge, the request travels through a complex web of intermediaries, eventually landing at the issuing bank. The issuer evaluates the request and sends back a two-digit response code based on the Decline Code, a protocol that dates back to the 1980s.

Among these codes, “05 Do Not Honor” is the most notorious. Originally designed as a catch-all category, it essentially means the bank is refusing the transaction but declines to specify exactly why. Unlike a code 51 (Decline Code 51) or a code 14 (Invalid Card Number), which offer clear diagnoses, code 05 is deliberately opaque. It can account for 10-60% of all payment declines depending on geography and card network (Source).

Issuers rely heavily on this code for a few practical reasons. First, risk engines are incredibly complex. An issuer might decline a transaction because the user’s velocity of purchases over the last hour looks suspicious, combined with a mismatch in the expected geolocation, combined with a merchant category code (MCC) that historically carries higher risk. Because legacy communication protocols lack the bandwidth to transmit a detailed paragraph explaining this multivariate decision, the issuer simply returns a 05.

Second, ambiguity serves as a defense mechanism against fraud. If an issuer explicitly tells a fraudster that a transaction failed due to an incorrect CVV, the fraudster learns exactly which piece of data they need to acquire next. By returning a generic “Do Not Honor,” the issuer keeps bad actors in the dark. Unfortunately, this protective measure also keeps legitimate merchants in the dark, leading to widespread payment failures that require strategic unpacking.

Deconstructing the Payment Processing Flow

To systematically unpack a generic decline, it helps to slow down the 100-millisecond journey of a transaction and observe the variables at play.

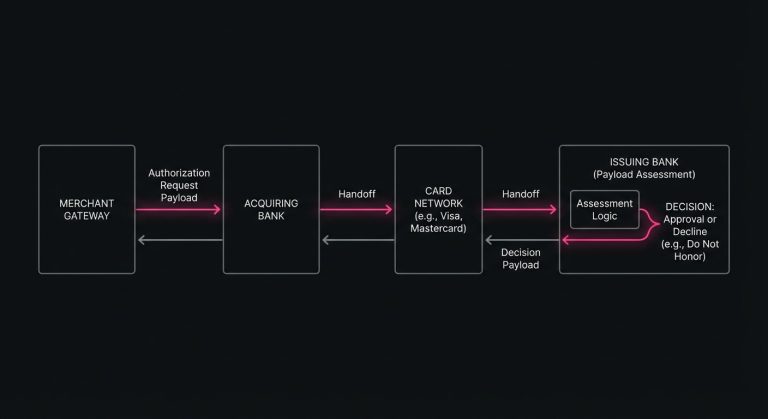

When a customer clicks the buy button, the payment processing flow begins. The merchant’s gateway formats the payment details and sends them to the acquiring bank. The acquirer then routes the request through the respective card network (Visa, Mastercard, American Express) to the issuing bank. At the final destination, the issuer’s authorization system ingests the data payload and runs it against hundreds of rules.

This payload contains much more than just a card number and an amount. It includes the time of day, the currency, the merchant’s location, the network token cryptogram (if applicable), the 3D Secure authentication status, and various risk indicators. If any combination of these data points triggers the issuer’s internal risk threshold, the transaction is rejected.

The Role of Context in Issuer Decisions

Because the issuer is evaluating a holistic data payload, context is everything. A transaction declined at 2:00 AM might be approved at 2:00 PM simply because the issuer’s risk model flags late-night cross-border purchases as highly anomalous. Similarly, a $100 charge might be flagged while a $20 charge goes through without friction.

Understanding this fluidity is crucial. A generic decline is not a permanent verdict on the validity of the cardholder’s account; it is a point-in-time assessment of the specific data payload presented in that exact moment. Change the moment, change the data, or change the context, and you fundamentally alter the probability of an approval.

Soft Declines vs. Hard Declines

A foundational concept in revenue recovery is the distinction between soft and hard declines. Categorizing these responses correctly is the first step toward building an intelligent retry logic.

Hard declines represent permanent, unresolvable issues. If an issuer returns a code indicating a stolen card, a closed account, or an invalid primary account number (PAN), the conversation is over. Retrying a hard decline is not only futile, but it also actively harms a merchant’s standing with the card networks. Card network rules strictly prohibit repeatedly pinging invalid accounts, and doing so can result in authorization fines and damaged trust with issuing banks.

Soft declines, on the other hand, are temporary roadblocks. They indicate that the account is valid, but something about the current request is unacceptable. Insufficient funds, processor timeouts, and generic risk flags fall into this category. “Do Not Honor” is almost exclusively a soft decline. The card is real, the account is open, but the issuer is saying “not right now” or “not exactly like this.”

Recognizing “Do Not Honor” as a soft decline shifts the operational mindset. It moves the merchant away from passively accepting a lost sale and toward proactively engineering a successful subsequent attempt.

The Hidden Cost of Unoptimized Checkout Issues

Accepting soft declines at face value creates a silent, compounding revenue leak. In standard e-commerce environments, unexpected checkout issues frustrate customers who may simply abandon their carts and move to a competitor. The friction of having to dig out a different card or call their bank is often enough to kill the impulse to purchase.

The stakes are even higher in the recurring revenue space. Subscription payment issues are particularly damaging because a single failed renewal does not just cost the merchant one month of revenue; it potentially severs the entire future lifetime value (LTV) of that customer. Involuntary churn-where a customer loses access to a service simply because their perfectly valid card was hit with a generic decline-is one of the most frustrating challenges a growth team can face.

If a merchant has a recurring billing base of 100,000 subscribers, and 5% of those encounter a “Do Not Honor” decline each month, the financial impact is staggering. Optimizing the recovery of those transactions is not merely a backend operational task; it is a primary driver of top-line growth and customer retention. Recurring payments face a 15% average decline rate, while standard one-time purchases see only 4.5-5% decline rates.

Timing is Everything in Payment Recovery

Once a merchant accepts that a soft decline warrants another attempt, the immediate instinct is often to retry the card right away. This brute-force approach is exactly what issuers hate, and it is almost guaranteed to fail.

When an issuer declines a transaction for suspected risk or velocity limits, hitting their servers again three seconds later with the exact same data payload only confirms their suspicion that something automated and potentially malicious is happening. The issuer will simply return another “Do Not Honor,” and if the merchant continues to loop, the issuer may place a temporary block on the card entirely.

Intelligent payment recovery requires patience and a deep understanding of cardholder behavior and banking cycles.

The Science of Spacing and Scheduling

Timing a subsequent attempt involves analyzing several operational rhythms. For example, if a decline is secretly masking an insufficient funds issue-a very common reality behind the 05 code-retrying the next day might yield a success if the customer’s paycheck clears. Many successful recovery strategies align their attempts with typical bi-weekly payroll dates, such as the 1st or 15th of the month.

Time zones also play a critical role. If a merchant based in the United States attempts to renew a European subscriber’s account at 3:00 AM local European time, the European issuing bank might decline it due to off-hours risk parameters. Waiting to retry failed payments until the cardholder’s local business hours can dramatically shift the risk scoring algorithm in the merchant’s favor.

Furthermore, some legacy banking systems undergo maintenance windows during the early hours of Sunday morning. Transactions attempted during these windows often result in generic declines simply because the main authorization system is offline and the secondary system defaults to a conservative risk posture. Waiting 24 hours to retry circumvents this infrastructure limitation entirely.

Modifying the Variables for the Next Attempt

Changing the timing is powerful, but altering the data payload of the transaction itself is where true optimization happens. If the issuer did not like the way the transaction looked the first time, presenting it slightly differently on the second attempt can bypass the friction points.

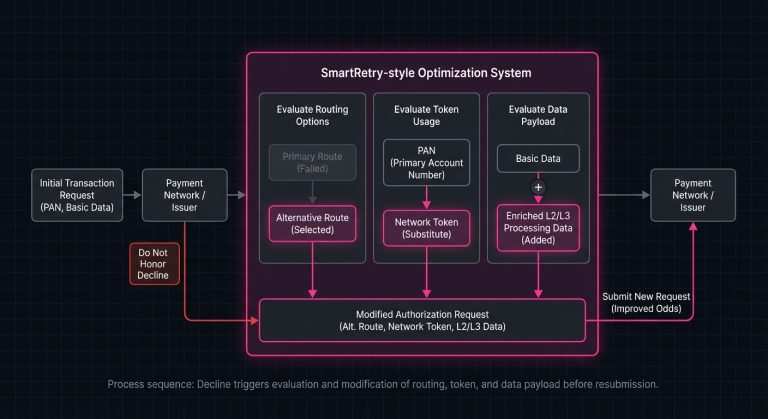

One highly effective variable modification is dynamic routing. Large merchants often utilize multiple acquiring banks. If Acquirer A submits a transaction and receives a “Do Not Honor,” the merchant might route the retry through Acquirer B. Acquirer B might have a domestic acquiring BIN in the cardholder’s country, converting what was initially perceived as a risky cross-border transaction into a safe, domestic one. The issuer sees the new domestic request and approves it without hesitation.

Another crucial variable is the presence of network tokens. Traditional PANs are increasingly viewed with scrutiny by issuers, especially in card-not-present environments. By swapping the raw card number for a network token on the retry attempt, the merchant signals to the issuer that the payment credential was securely provisioned by the network itself. This elevated trust level frequently flips a generic decline into an approval.

Data enrichment also plays a role. If the initial attempt was sent as a bare-bones request, the retry might include Level 2 or Level 3 processing data, passing along specific line-item details, tax amounts, and enhanced customer information. Providing this granular transparency lowers the issuer’s perceived risk, addressing the root cause of the initial hesitation.

Building an Intelligent Optimization Strategy

Executing these strategies manually or relying on static, hard-coded rules (“retry every 3 days”) is no longer sufficient in a modern processing environment. The rules of authorization change constantly, varying by region, by card network, and by the individual issuing bank’s ever-shifting risk appetite.

To systematically reduce payment declines, merchants must adopt dynamic, data-driven strategies. This involves collecting vast amounts of telemetry on how specific issuers respond to specific transaction shapes at specific times. Over time, patterns emerge. An optimization engine might learn that a particular credit union in the Midwest consistently throws a “Do Not Honor” on Friday nights but approves the exact same transaction on Saturday mornings.

This is where specialized technology becomes invaluable. Platforms like SmartRetry naturally fit into this ecosystem, focusing on payment optimization and intelligent retries of declined payment transactions, helping merchants recover revenue and improve transaction approval rates without the need for manual guesswork. By leveraging historical authorization data and dynamic routing logic, these systems understand the invisible thresholds of individual issuers, adapting the timing and payload of every retry to maximize the probability of success.

By offloading the complexity of retry logic to intelligent systems, merchants can focus on their core product while their backend infrastructure works quietly to salvage revenue that would otherwise be lost to the void of legacy error codes.

Empathy for the Issuer: Why False Positives Happen

As frustrating as generic declines are, it is highly beneficial for merchants to view the ecosystem with a degree of empathy for the issuing banks. Issuers are not arbitrarily declining transactions to annoy merchants; they are operating under immense pressure.

In a card-not-present environment, the liability for fraudulent transactions frequently falls on the issuer. If they approve a charge that turns out to be fraudulent, they are the ones left making the cardholder whole. Additionally, issuers face strict regulatory scrutiny regarding anti-money laundering (AML) and financial compliance.

Faced with massive, coordinated bot attacks, credential stuffing, and sophisticated fraud rings, issuers rely heavily on their automated risk engines. These engines are tuned to prioritize the safety of the cardholder’s funds over the merchant’s conversion rate. False positives-legitimate transactions blocked by an overzealous risk model-are the unfortunate byproduct of this defensive posture.

When merchants understand this, the relationship shifts from adversarial to collaborative. By actively managing their authorization hygiene-keeping their chargeback ratios low, utilizing brute-force retry avoidance where appropriate, participating in Account Updater programs, and avoiding aggressive, rapid-fire retries-merchants build a reputation of trust with issuing banks.

A merchant with a history of clean, high-quality transaction requests will eventually find their overall authorization rates rising. Issuers dynamically adjust their risk thresholds based on the trust score of the merchant processing the volume. Good behavior is rewarded at the network level, turning a localized recovery strategy into a macro-level advantage.

Moving Beyond the Initial Decline

The anatomy of a generic decline reveals a payment ecosystem that is deeply interconnected, highly sensitive, and entirely probabilistic. It is a system built on decades of evolving technology, where modern machine learning models are layered on top of legacy mainframe protocols, all attempting to communicate complex risk assessments in fractions of a second.

A “Do Not Honor” code is not a rejection of the customer, nor is it a final verdict on the transaction. It is simply the issuing bank’s way of asking for more context, a better time, or a different approach.

By deconstructing the payment flow, distinguishing between hard and soft failures, timing retry attempts with precision, and dynamically altering the data payload, merchants can transform their approach to transaction recovery. The goal is no longer simply to accept the hand that is dealt by the payment networks, but to actively participate in the authorization process.

When viewed through the lens of continuous optimization, the moment a card is declined ceases to be the end of the customer journey. Instead, it becomes the exact moment where intelligent infrastructure takes over, navigating the complexities of the financial system to deliver the revenue you have rightfully earned.

Still letting failed transactions slip through?

SmartRetry turns declines into approvals - automatically, intelligently, and without changing your payment provider.

Frequently asked questions about this topic

Share this article

Author

Roi Lagziel

Roi Lagziel is a payments engineer specializing in authorization optimization, retry strategies, and issuer-level behavior. His work focuses on building practical, data-driven systems that help payment teams reduce false declines and recover lost revenue.

Read all articles >More in Smart Payment Retry Strategies:

March 8, 2026

Decoding Hard and Soft Declines: A Practical Guide to Smarter Payment Recovery

This guide explains how to classify payment declines, respond with the right retry strategy, and reduce unnecessary churn, fees, and approval-rate drag across checkout and recurring billing.

March 8, 2026

The Boomerang Effect: Why Brute-Force Retries Cost More Than They Recover

This article explains why blind payment retries erode issuer trust, add network costs, and hurt future approvals, and how smarter decline management can improve recovery and authorization performance.

March 8, 2026

The Art of the Second Chance: Decoding Soft vs. Hard Declines

This article explains how to separate recoverable declines from permanent failures, optimize retry logic, and reduce involuntary churn to protect revenue and improve approval performance.