Authorization Code 41: How Payment Teams Should Handle Lost Card Declines

March 8, 2026

![]() 13 min

13 min

The Phantom Plastic: Decoding Authorization Code 41 and the Logic of Lost Cards

Transactions fail, and it is a fundamental truth of digital commerce. Carts are abandoned, network connections time out, and payment gateways encounter sudden routing errors. But not all payment issues are created equal. Some failures are temporary hiccups born of a momentary network delay or a fleeting lack of funds, while others are definitive, final, and uncompromising. Enter Authorization Code 41. In the complex web of the payment processing flow, this specific issuer response carries a clear and undeniable message: the card is lost. It is gone, and it will not work tomorrow or next week. Understanding how to handle this specific signal separates sophisticated payment operations from the rest of the pack.

In a probabilistic ecosystem where merchants constantly try to discern why a transaction declined, Code 41 stands out as a moment of absolute clarity. It is a hard decline in its purest form. Yet, despite the definitive nature of this response, many payment systems and operational workflows treat it as just another error code, blindly throwing it back into the same retry logic loops used for temporary failures. This approach not only wastes resources but can actively damage a merchant’s standing with issuing banks.

To navigate the realities of lost cards, payment professionals must understand the mechanics of the decline, the hidden costs of ignoring network signals, and the strategic interventions required to bridge the gap between a lost piece of plastic and a newly issued account number.

The Anatomy of an Authorization Code 41

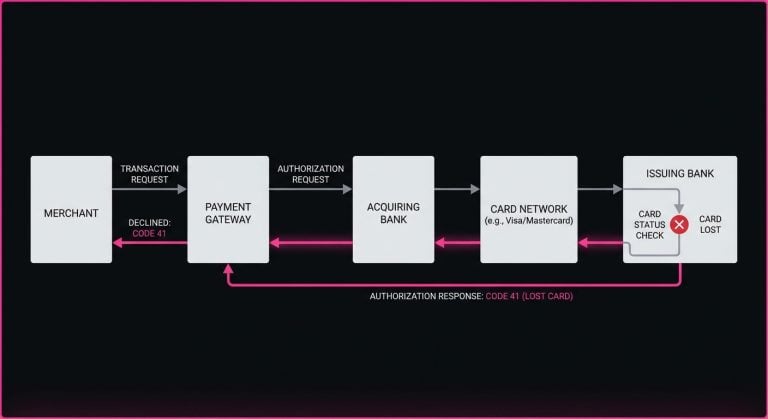

To understand a Code 41, it helps to look at the underlying architecture of global payments. When a customer initiates a transaction, the merchant’s system generates an authorization request. This request travels through a highly orchestrated payment processing flow. It moves from the merchant to the payment gateway, through the acquiring bank, across card networks like Visa or Mastercard, and finally arrives at the issuing bank.

The issuer’s core banking system evaluates the request against a massive array of variables like available balance, velocity rules, geographic location, and fraud risk scores. But before it checks any of that, it verifies the fundamental status of the Primary Account Number (PAN). It simply asks whether the account is open, active, and valid.

If the cardholder has reported their wallet missing or the bank has flagged the card as lost due to other security protocols, the issuer immediately halts the evaluation. The system then generates a specific standard response. Under the ISO 8583 messaging protocol, this is typically represented as Code 41.

This issuer response is vastly different from a soft decline. Soft declines, such as Code 51 or a generic Code 05 for do not honor, suggest that the transaction cannot be completed right now under the current circumstances. The underlying account is still valid, but a specific condition hasn’t been met. These responses leave the door open for future attempts.

A hard decline like Code 41 slams the door shut and locks it, with the bank explicitly stating that the presented credential is dead. It has been deactivated at the network level to prevent unauthorized use. No amount of time, varied transaction amounts, or altered billing details will resurrect it. The card is functionally obsolete.

Beyond the Couch Cushions: Why Cards Get Flagged

The obvious cause of a Code 41 is the literal loss of the physical card. A customer leaves their wallet in a taxi, panics, opens their banking app, and reports the card lost. The issuer instantly updates the PAN status, and any subsequent authorization attempts on that specific 16-digit number will return a 41.

However, cards frequently get lost without ever leaving the customer’s possession. Issuing banks rely on incredibly sophisticated card networks. If a major retailer suffers a data breach and credit card numbers are compromised, banks will often take preemptive action. They may identify thousands of cards that interacted with the breached merchant during the vulnerability window and proactively flag them as lost or compromised.

In these scenarios, the bank issues a replacement card and mails it to the customer, but the cardholder may be entirely unaware of the situation until the physical envelope arrives. They still have their original plastic card in their pocket and might even try to use it for an online purchase, only to find the payment declined.

This creates a unique friction point for merchants handling recurring billing or subscription payments. A customer who has happily paid for a service on the 15th of every month for three years suddenly triggers a Code 41. This happens not because they churned or lack funds, but because a data breach at an entirely unrelated company caused their bank to burn their existing PAN.

The Hidden Costs of Disrespecting the Network Signal

When faced with payment failures, the instinct of many merchants is to simply try again by putting a failed transaction in a queue to retry tomorrow, and perhaps again three days later. While aggressive retry logic can be highly effective for soft declines, applying this brute-force approach to a Code 41 is a profound operational mistake.

First, there is the direct financial cost. Every time a merchant sends an authorization request through the network, there is a micro-transaction fee. Whether the transaction is approved or declined, the payment gateway, the acquirer, and the network take their fraction of a cent or flat fee. Hammering the network with daily retries on a lost card is the digital equivalent of feeding coins into a broken vending machine because you are essentially paying for the privilege of being rejected.

More importantly, ignoring hard declines severely damages a merchant’s overall transaction approval rate. Issuing banks monitor merchant behavior meticulously, calculating approval ratios to determine how much risk a specific business poses to their network. If an issuer sees a merchant repeatedly attempting to authorize transactions on a card that was explicitly flagged as lost a week ago, the issuer’s risk models register that merchant as reckless, poorly optimized, or potentially fraudulent.

This deterioration in reputation has a blast radius. As a merchant’s standing with an issuer drops, the bank may begin applying stricter fraud filters to that merchant’s traffic. Suddenly, perfectly healthy transactions from legitimate customers start getting caught in the crossfire, leading to a rise in generic soft declines. By failing to respect the definitive signal of a Code 41, merchants inadvertently drag down the success rate of their entire payment volume.

Strategic Interventions: The Account Updater Lifeline

If a Code 41 means the current card is dead and retrying it is harmful, how does a merchant recover the revenue? The answer lies in the transition from the old PAN to the new one.

When an issuer flags a card as lost, they almost always generate a new PAN for the customer simultaneously. The challenge for the merchant is obtaining that new credential without introducing friction into the customer experience. This is where network-level Account Updater services become invaluable.

Programs like Visa Account Updater or Mastercard Automatic Billing Updater act as secure directories bridging the gap between old and new cards. Issuing banks continuously feed these directories with mapping data, indicating that the old PAN has been replaced by a new PAN with a new expiration date.

Sophisticated payment platforms query these updater services when they encounter a lost or expired card. Instead of attempting to authorize the dead card, the system asks the network if a replacement exists. If a match is found, the merchant’s payment vault is updated silently in the background, and the transaction is routed using the new, healthy credential.

However, there is a temporal challenge because database updates are not always instantaneous. There is often a window of latency between the moment a customer reports a card lost, the moment the bank issues the new card, and the moment the Account Updater network receives the new mapping. If a merchant’s billing cycle hits precisely within this gap, they will receive a Code 41, and an immediate check of the updater service might return a blank result.

Payment Optimization and Intelligent Decisioning

Navigating this timing gap requires a shift from static billing rules to intelligent, state-aware payment routing. Treating all declines equally is a symptom of legacy architecture. Instead, true payment optimization requires building logic that reads the specific decline code and dynamically adjusts the system’s behavior.

When a transaction returns a Code 41, an optimized system immediately halts all standard, scheduled retries for that specific payment method, changing the state of that credential to a hard decline and quarantining it.

Platforms like SmartRetry are built around this exact operational philosophy. By focusing on payment optimization and intelligent retries of declined transactions, these systems help merchants recover revenue and improve transaction approval rates. Instead of blindly hammering a dead card, an intelligent architecture reads the Code 41, stops counterproductive authorization attempts, and shifts the recovery strategy toward updating the underlying credential.

This might involve scheduling an asynchronous check against the Account Updater service three to five days after the initial Code 41, allowing the banking infrastructure enough time to propagate the new PAN details. By building a deliberate, timed delay specifically tailored to the life cycle of a lost card replacement, merchants can dramatically increase their chances of a silent, frictionless recovery.

The Role of Network Tokenization

While Account Updater services are highly effective, the payments industry is moving toward an even more robust solution with tokenization. Under the EMVCo standard, a merchant does not store the raw 16-digit PAN but instead stores a secure network token issued directly by the card network.

Tokens decouple the merchant’s billing engine from the physical plastic in the customer’s wallet. When a customer loses their card and the bank issues a new one, the underlying PAN changes, but the network token assigned to that specific merchant remains valid. The issuing bank simply updates the mapping on their end to link the new PAN to the existing token.

For merchants utilizing network tokens, the incidence of Code 41 declines drops precipitously. A customer might lose their wallet, report it to the bank, and receive a new card days later. Meanwhile, the merchant’s subscription billing engine triggers a payment using the network token, and the transaction is approved seamlessly. The customer never experiences an interruption in service, and the merchant avoids dealing with a hard decline entirely.

Rethinking the Dunning Process for Lost Cards

Despite the best efforts of Account Updater services and tokenization, there will always be scenarios where the merchant cannot programmatically retrieve the new card details. The issuing bank might not participate in the updater network, or the customer might use the loss of their wallet as an opportunity to switch banking providers entirely. When automation fails, the merchant must rely on customer communication, commonly known in the industry as dunning.

The dunning workflow for a Code 41 should look fundamentally different from the workflow for a soft decline. If a payment fails due to insufficient funds, the customer usually knows they are short on cash, and a gentle reminder to add funds before the system retries is completely appropriate.

With a lost card, the customer is fully aware they lost their wallet, but they may not realize which specific online services were tied to that account while dealing with the stress of updating payment details across dozens of platforms.

The messaging strategy here must be empathetic and highly specific. Sending a generic payment failure email only causes confusion and anxiety. Instead, a highly optimized dunning email states clearly: “We noticed your bank declined the transaction because your card was reported lost or replaced. When your new card arrives, please take a moment to update your details here.”

This clarity removes the guesswork for the customer by acknowledging their situation, explaining exactly why the checkout issue occurred, and providing a direct path to resolution. Furthermore, because a Code 41 is a definitive failure, the merchant can initiate this communication immediately rather than waiting through a series of futile retries before reaching out.

The Data Behind the Declines

Managing payment failures effectively requires robust telemetry, and payment operations teams should treat decline codes as critical operational data points rather than simple transaction errors. Tracking the baseline rate of Code 41 declines provides immense visibility into the health of a merchant’s recurring revenue base.

If a merchant historically sees a 0.5% rate of Code 41 declines and that number suddenly spikes to 3% over a single weekend, it rarely means that thousands of customers simultaneously lost their wallets. It is almost always an indicator of a macro-level event, such as a large issuing bank reacting to a regional data breach by force-reissuing millions of cards.

By monitoring these anomalies, teams can proactively adjust their recovery strategies. They might pause dunning emails temporarily, knowing that customers haven’t received their new physical cards in the mail yet, or they might trigger manual updater batch files to catch the incoming wave of new PANs before the next billing cycle hits.

Additionally, analyzing the resolution pathways of Code 41s provides valuable insight into the effectiveness of a merchant’s payment stack. Operations teams should measure exactly what percentage of lost cards are recovered silently via Account Updater services versus what percentage require manual customer intervention. Tracking these metrics allows teams to quantify the ROI of implementing network tokens or upgrading their payment gateway integration.

Building a Resilient Architecture

The reality of digital commerce is that the physical objects tethering consumers to their digital identities will occasionally be misplaced, stolen, or proactively destroyed by risk algorithms. Authorization Code 41 is the network’s way of communicating this physical reality back to the digital ecosystem.

For merchants focused on growth, treating a lost card as a lost customer is a failure of imagination. The customer’s intent to pay hasn’t changed, only the credential has. To reduce payment declines and successfully retry failed payments in an intelligent manner, businesses must respect the boundaries set by the issuing banks.

When a card is lost, brute force is not the answer. The optimal path requires an architecture that listens to the network, halts unproductive authorization attempts, leverages secure data pathways to seek updated credentials, and engages the customer with clarity and precision only when automation reaches its limits.

By treating Code 41 not as an impassable roadblock but as an operational trigger requiring a specific strategic response, payment teams can protect their approval rates, minimize unnecessary processing fees, and ensure that a misplaced piece of plastic doesn’t sever a valuable customer relationship. The most sophisticated payment operations aren’t the ones that never experience failures. Instead, they are the ones that know exactly how to interpret every network signal and turn definitive declines into predictable, seamless recoveries.

Still letting failed transactions slip through?

SmartRetry turns declines into approvals - automatically, intelligently, and without changing your payment provider.

Frequently asked questions about this topic

Share this article

Author

Roi Lagziel

Roi Lagziel is a payments engineer specializing in authorization optimization, retry strategies, and issuer-level behavior. His work focuses on building practical, data-driven systems that help payment teams reduce false declines and recover lost revenue.

Read all articles >More in Payment Failures & Decline Codes:

March 8, 2026

The Hidden Mechanics of Cross-Border Card Declines

This article explains why international card transactions underperform, from issuer risk models to data mismatches and recurring billing gaps, and shows operators where to act to recover revenue and reduce false declines.

March 8, 2026

Issuer Response Code 43: Why Merchants Must Stop Retries on Stolen Cards

This article explains why Code 43 is a terminal decline, how to remove dead credentials from retry logic, and how disciplined handling protects approval rates, margin, and customer recovery.

March 8, 2026

Decoding Authorization Code 59: How Suspected Fraud Declines Affect Payment Recovery

This article explains why issuers return Authorization Code 59, how false positives hurt conversion, and what payment teams can do to recover legitimate revenue without damaging approval rates.