The Secret Language of Issuers: Decoding Merchant Advice Codes

March 8, 2026

![]() 14 min

14 min

The Secret Language of Issuers: Decoding Merchant Advice Codes

A transaction is declined. The screen flashes a generic error. Money is left on the table. The customer simply walks away. It happens every second of every day across the digital economy. Payment failures are an unavoidable reality of doing business online. Yet, how a merchant responds to these failures often determines the line between a thriving digital business and a leaky revenue bucket. When a bank rejects a transaction, they are not just closing the door on that specific purchase. They are often leaving a clue. Deciphering that clue requires an understanding of Merchant Advice Codes.

For years, the payments industry operated essentially in the dark when it came to authorization rejections. Merchants received cryptic, two-digit codes that offered little in the way of actionable intelligence. Today, the landscape has evolved. The payment processing flow is more sophisticated, networks are more communicative, and issuers are providing granular metadata designed to guide merchant behavior. Understanding this secret language turns a dead-end decline into a strategic opportunity for payment optimization.

The Anatomy of a Modern Payment Decline

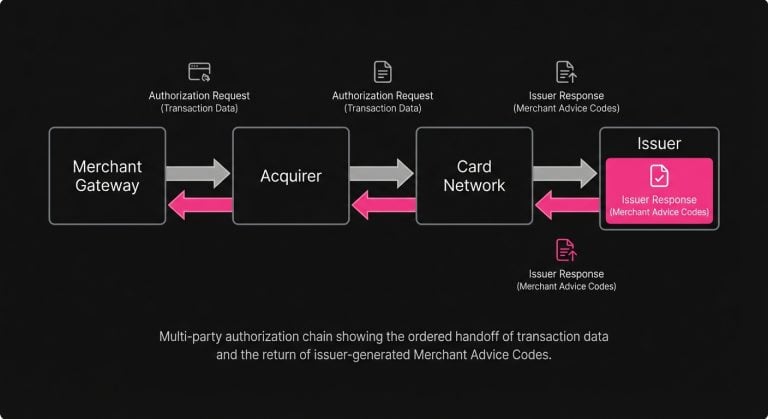

To understand why Merchant Advice Codes matter, it helps to briefly look at what actually happens when a transaction goes sideways. Every time a customer initiates a purchase, a complex web of communication fires across the globe. The merchant’s gateway talks to the acquirer, the acquirer routes the request through the card network, and the network knocks on the door of the issuing bank.

The issuing bank holds the ultimate authority. They evaluate the payment authorization request against hundreds of variables in a matter of milliseconds. They look at the cardholder’s balance, historical spending patterns, location data, velocity of purchases, and the merchant’s historical risk profile. Based on this rapid-fire calculation, the issuer sends back a response.

Historically, this issuer response was rooted in the ISO 8583 standard-a messaging protocol developed in the 1980s primarily for physical point-of-sale terminals. These legacy decline codes are notorious for their lack of clarity. If a card declined, a merchant might receive a Code 51 (Insufficient Funds), which is relatively clear. But far more often, they would receive a Code 05 (Do Not Honor), a frustratingly vague catch-all that essentially translates to, “No, and we aren’t going to tell you why.”

For a physical store owner in 1985, a “Do Not Honor” code simply meant asking the customer for a different card. For a global software-as-a-service company managing millions of recurring subscriptions, a generic decline code is an operational nightmare. It leaves engineering and finance teams guessing whether they should attempt the charge again the next day, wait a week, or immediately email the customer to ask for updated billing details.

The Problem With Flying Blind

When merchants lack context regarding why a transaction failed, they tend to adopt one of two flawed strategies: they either give up immediately, or they retry the card aggressively. Both approaches carry significant costs.

Giving up immediately means accepting unnecessary customer churn. Many payment issues are entirely temporary. A customer might be momentarily over their daily spending limit, the issuer’s risk system might be experiencing a brief timeout, or funds might be scheduled to clear into the account later that same afternoon. Treating every decline as a final verdict abandons perfectly valid revenue.

Conversely, aggressive retries are equally damaging. Treating a generic decline like a stubborn jar lid you just need to twist harder is a fast track to network penalties. The card networks monitor merchant retry logic closely. If an issuer has explicitly blocked a card because it was reported stolen, and a merchant system blindly attempts to charge that card four more times over the next week, the network notices.

This aggressive behavior degrades a merchant’s overall authorization rate. Issuers utilize complex machine learning models to assess risk, and they look closely at how acquirers and merchants behave. A merchant that repeatedly submits authorization requests for dead cards looks reckless, poorly managed, or potentially fraudulent. Over time, issuers may begin to decline even the borderline-valid transactions from that merchant out of an abundance of caution.

This tension-the merchant’s need to recover revenue versus the network’s need for order and efficiency-paved the way for a more communicative framework.

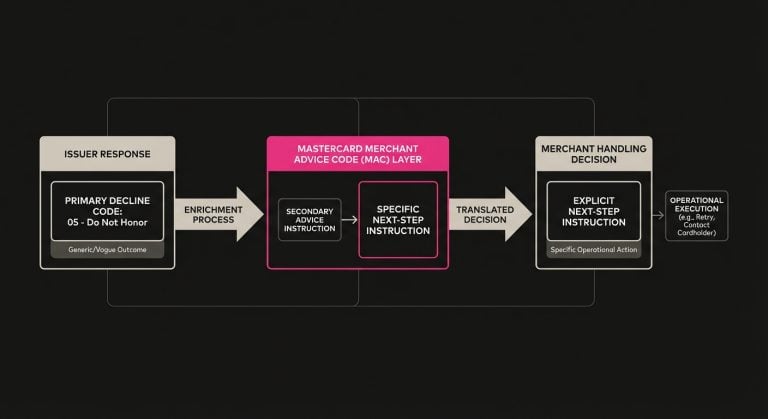

Enter the Merchant Advice Code

Recognizing the friction caused by legacy decline codes, Mastercard introduced the Merchant Advice Code (MAC) framework to provide a secondary layer of intelligence. While the primary decline code might still read as a generic failure, the MAC acts as a supplementary instruction manual, telling the merchant exactly how to handle the situation moving forward.

It is worth noting that while “Merchant Advice Code” is specifically Mastercard’s terminology, the concept of providing secondary, actionable response data has permeated the industry. Visa offers similar guidance through its own advanced response codes, category management rules, and Account Updater responses. For the sake of clarity, the payments industry often uses the concept of advice codes as a shorthand for this layer of instructional metadata, regardless of the specific network routing the transaction.

By appending these specific directives to the issuer response, the network removes the guesswork. The issuer is no longer just saying “no.” They are saying, “no, but here is exactly what you should do next.”

Deconstructing the “Do Not Honor” Dilemma

To see the value of a MAC, consider how it rescues the dreaded 05 Do Not Honor decline. On its own, an 05 Do Not Honor is an impenetrable wall. However, when paired with an advice code, it transforms into a clear operational directive.

If a merchant receives an 05 Do Not Honor coupled with an instruction that indicates the account has been closed, they know with absolute certainty that no amount of retrying will ever result in a successful charge. The automated billing system can immediately halt future attempts and trigger a dunning email to the customer, asking them to update their payment profile.

Alternatively, if that same 05 Do Not Honor decline is accompanied by an advice code indicating a temporary hold or suggesting a later retry, the merchant’s system can safely queue the transaction for another attempt 48 hours later, confident that they are operating within the network’s good graces.

The Core Advice Codes You Need to Know

While networks frequently update and refine their technical documentation, the advice codes generally fall into a few distinct operational categories. Understanding the intent behind these categories is crucial for any team tasked with minimizing checkout issues and optimizing revenue streams.

Code 01: New Account Information Available

This code is an operational lifesaver for businesses that rely on card-on-file transactions. When an issuer returns a Account Updater advice code, they are signaling that the card data the merchant attempted to use is outdated, but the customer still holds an active account with the bank.

Typically, this means the card has expired, was lost, or was upgraded to a new tier, and a replacement card has been issued. The instruction here is straightforward: do not retry this specific card number. Instead, the merchant should query the network’s Account Updater service to retrieve the new Primary Account Number (PAN) or expiration date, and then attempt the charge using the fresh credentials.

Code 02: Try Again Later

If there is a golden ticket in the realm of payment failures, it is the soft decline code. This response explicitly tells the merchant that the failure is temporary. The issuer cannot approve the transaction right now, but they anticipate that the situation may resolve itself shortly.

Why would an issuer send this? It often relates to temporary funding issues, such as a customer waiting for a direct deposit to clear, or it might be triggered by a velocity check if the cardholder has made an unusually high number of purchases in a single day. When a merchant receives an Insufficient Funds (Code 51), it validates their decision to retry failed payments. The network has given them permission to try again, provided they wait a reasonable amount of time (often defined by network rules as 24 to 72 hours) before initiating the subsequent authorization request.

Code 03: Do Not Try Again

This is the hard stop. A Code 43 advice code indicates that the decline is final and permanent. The account may be closed, the card may have been reported stolen, or there is suspected fraud associated with the credential.

Retrying a transaction after receiving a Code 43 is not just futile; it is actively harmful to the merchant’s standing with the networks. Systems should be architected to immediately flag these cards, remove them from any automated retry loops, and prompt the user for an entirely new method of payment. See Issuer Response Code 43: Why Merchants Must Stop Retries on Stolen Cards for details.

Code 04: Token Requirements

As the industry moves aggressively toward network tokenization, advice codes are adapting. A retry logic code often surfaces to indicate that the merchant should be utilizing a network token rather than the raw PAN for this specific transaction type or card profile. Network tokens replace sensitive card details with unique digital identifiers, heavily reducing fraud risk and frequently benefiting from higher authorization rate. An advice code pointing to tokenization is the network’s way of nudging a merchant’s payment architecture into a more secure, optimized state.

Code 21: Payment Cancellation

This code is highly specific to the recurring billing model and directly addresses subscription payment issues. When a customer contacts their issuing bank to revoke authorization for a specific recurring charge-often because they forgot how to cancel the service directly with the merchant-the issuer will return a soft decline advice code on the next billing attempt.

This code is an unambiguous instruction to cancel the subscription agreement. Attempting to charge the card again after receiving a decline is a direct violation of network rules and is almost guaranteed to result in a costly chargeback if the transaction somehow forces its way through.

The Operational Impact of Getting It Right

The distinction between a standard decline and an advice-code-driven response might seem like a minor technicality, but its impact on business operations is profound. Modern commerce operates at a scale where single-digit percentage improvements in approval rate translate to massive revenue figures.

When a merchant ignores the secondary data provided by issuers, they inadvertently engage in a practice known as “recycling.” Recycling is the brute-force method of payment recovery, where a system simply attempts to charge a declined card over and over again on a set schedule-perhaps every day at midnight for a week.

The card networks view thoughtless recycling as a strain on their infrastructure. To combat this, networks like Mastercard have instituted strict monitoring programs, such as the Transaction Processing Excellence (TPE) framework. These programs actively assess merchant retry logic. If a merchant’s system ignores a “Do Not Try Again” directive and repeatedly hammers the network with authorization requests for a dead card, the merchant will be penalized with direct fines for excessive retries.

Furthermore, every authorization attempt-successful or not-carries a microscopic network fee. While fractions of a cent seem insignificant in isolation, a poorly designed retry loop running millions of unnecessary attempts across a large customer base quickly inflates payment processing costs.

Conversely, reading and respecting the advice codes aligns the merchant’s financial interests with the network’s operational constraints. By only retrying transactions that have a realistic chance of success, the merchant drastically reduces unnecessary processing costs, entirely avoids TPE penalties, and signals to the issuing banks that they are a sophisticated, low-risk partner.

Building a Smarter Retry Strategy

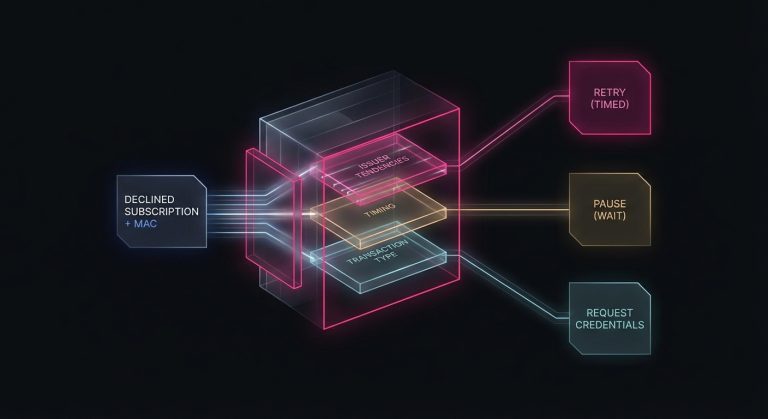

The transition from dumb retries to intelligent payment recovery requires a fundamental shift in how payment systems are architected. The logic governing whether to retry a charge can no longer be a static rule based solely on the legacy ISO code. It must become a dynamic decision engine that ingests multiple data points simultaneously.

To reduce payment declines effectively, a system must look at the primary decline code, the supplementary advice code, the time of day, the specific issuing bank’s historical behavior, and the nature of the transaction itself. For example, a “Try Again Later” advice code on a $10 monthly software subscription might warrant a retry 48 hours later. That same advice code on a $2,000 luxury furniture purchase might suggest the need to pause and send the customer a gentle SMS reminder to check with their bank regarding daily spending limits.

The operational heavy lifting required to parse these codes and dynamically adjust routing is significant. This is where modern infrastructure changes the equation. As a platform focused on payment optimization and intelligent retries of declined payment transactions, SmartRetry leverages granular data like Merchant Advice Codes alongside timing and issuer tendencies. By programmatically interpreting these signals rather than relying on static rules, merchants can safely navigate network constraints, helping them recover revenue and improve transaction approval rates without tripping fraud wires or incurring network penalties.

Ultimately, the goal of a smart retry strategy is to act invisibly. The best payment recovery is the one the customer never even realizes happened. When a system successfully reads an issuer’s cue to wait 24 hours and silently secures the funds on the second attempt, the customer avoids the friction of a suspended account or a nagging dunning email.

The Nuance of Subscription Operations

While e-commerce merchants selling physical goods benefit immensely from advice codes, the true power of this data is unlocked in the recurring billing space. Subscription-based businesses face a unique challenge: involuntary churn.

Involuntary churn occurs when a customer fully intends to continue paying for a service, but a technical failure severs the relationship. A card expires, a bank issues a replacement after a data breach, or a temporary freeze is placed on an account. The customer goes about their day, completely unaware that their subscription to their favorite software or streaming service is about to be canceled.

Traditional billing engines treat all failed recurring charges identically, usually by instantly revoking the user’s access and sending an aggressive “Update Your Payment Method” email. This is an incredibly poor user experience. It creates friction, forces the customer to log in and find their wallet, and worst of all, gives them a designated moment to re-evaluate whether they actually need the service at all. Many customers who receive a dunning email simply ignore it, effectively turning a temporary technical glitch into a permanently lost subscriber.

Merchant Advice Codes allow product and growth teams to map out sophisticated, empathetic recovery flows. If the code indicates new account information is available, the system can automatically query the network, update the card-on-file, and process the charge without ever bothering the user. If the code indicates a temporary hold, the service can grant the user a 3-day grace period while the system retries the charge in the background. The customer’s access is never interrupted, and the revenue is eventually secured.

By integrating advice codes into the core product experience, subscription businesses can drastically reduce involuntary churn, preserving their hard-earned customer lifetime value.

Moving from Reactive to Proactive Payments

The payments ecosystem is gradually moving away from the rigid, adversarial relationships of the past. For decades, it felt as though merchants were constantly fighting against issuing banks to get their transactions approved. Today, the introduction and expansion of granular response data highlight a more collaborative reality.

Issuers want legitimate transactions to go through just as much as merchants do. They make their money through interchange fees, and a cardholder who constantly experiences declined purchases will eventually migrate to a different bank. The network, the issuer, and the merchant all share the exact same goal: maximizing the volume of safe, legitimate commerce.

Merchant Advice Codes are the industry’s way of extending an olive branch. They represent an open line of communication, allowing banks to share their operational reality with the businesses initiating the charges.

To take advantage of this, organizations must elevate payments from a purely financial function to a core product strategy. Engineers, product managers, and growth leaders must view the checkout process not as a finalized endpoint, but as a continuous conversation with the financial network. When a decline happens, the system shouldn’t just record an error log; it should actively listen to the feedback being provided and adjust its behavior accordingly.

Understanding and implementing the logic behind Merchant Advice Codes is one of the highest-leverage activities a digital business can undertake. It transforms a frustrating, opaque process into a transparent, actionable workflow. By treating payment failures not as inevitable losses, but as puzzles with clearly provided instructions, merchants can reclaim lost revenue, protect their standing with the card networks, and deliver a frictionless experience that keeps customers coming back.

Still letting failed transactions slip through?

SmartRetry turns declines into approvals - automatically, intelligently, and without changing your payment provider.

Frequently asked questions about this topic

Share this article

Author

Roi Lagziel

Roi Lagziel is a payments engineer specializing in authorization optimization, retry strategies, and issuer-level behavior. His work focuses on building practical, data-driven systems that help payment teams reduce false declines and recover lost revenue.

Read all articles >More in Payment Failures & Decline Codes:

March 8, 2026

The Hidden Mechanics of Cross-Border Card Declines

This article explains why international card transactions underperform, from issuer risk models to data mismatches and recurring billing gaps, and shows operators where to act to recover revenue and reduce false declines.

March 8, 2026

Issuer Response Code 43: Why Merchants Must Stop Retries on Stolen Cards

This article explains why Code 43 is a terminal decline, how to remove dead credentials from retry logic, and how disciplined handling protects approval rates, margin, and customer recovery.

March 8, 2026

Authorization Code 41: How Payment Teams Should Handle Lost Card Declines

This article explains why Code 41 is a definitive lost-card decline, how to stop harmful retries, and where account updater, tokenization, and targeted dunning improve recovery and authorization performance.